Courting Crisis: The Case Against Cutting Bank Capital Requirements

Key Takeaways

- •Proposed rules cut CET1 capital by $88 billion for top U.S. banks.

- •System-wide CET1 ratio would fall from 13.4% to about 12.9%.

- •G‑SIB surcharge reduction alone removes $33 billion of capital buffer.

- •Lower capital may spur dividend buybacks and risk‑weight arbitrage.

- •Past data shows higher capital banks lend more, challenging “gold‑plating” claim.

Pulse Analysis

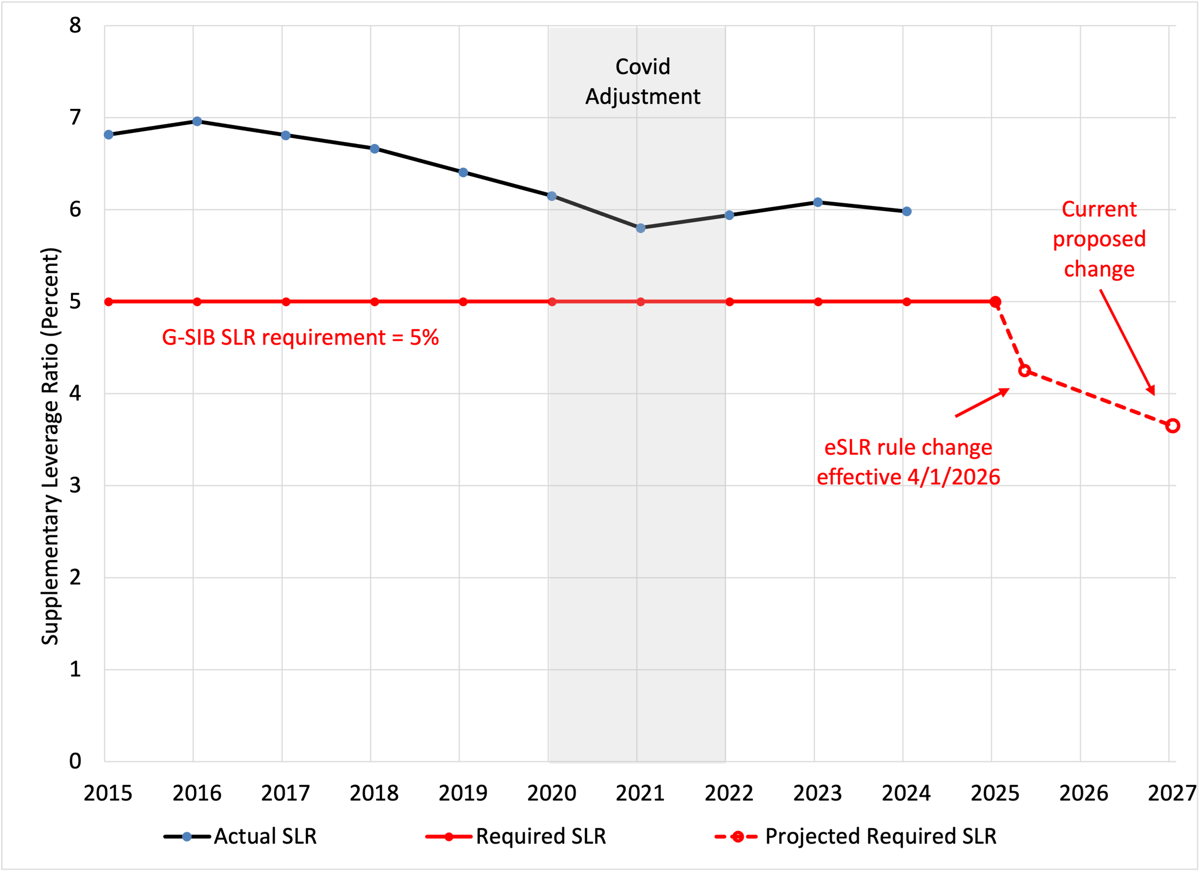

The March 2026 notice of proposed rulemaking marks a decisive shift away from the Basel III safeguards that have underpinned U.S. banking stability since the 2008 crisis. By allowing the largest banks to rely on a single risk‑weight calculation, trimming the G‑SIB systemic surcharge, and lowering risk‑weight factors for a broad set of assets, regulators aim to reduce the CET1 requirement by $88 billion. This would shrink the aggregate capital ratio to roughly 12.9%, a level many academics argue is well below the optimal range for absorbing shocks.

Beyond the headline numbers, the capital cuts could reshape banks’ balance‑sheet strategies. History shows that when capital buffers shrink, institutions often redirect the freed capital to shareholder returns—evidenced by the $33 billion of stock repurchases in Q1 2026—and to higher‑yield, lower‑risk‑weight assets. Such arbitrage can depress the leverage ratio, eroding a secondary line of defense. Moreover, empirical research consistently links stronger capital positions with more resilient lending, especially during stress periods, challenging the narrative that higher capital hampers credit growth.

The proposals also raise broader competitive and systemic concerns. U.S. banks have outperformed European peers despite stricter capital rules, disproving the “gold‑plating” argument that higher standards erode competitiveness. Weakening the framework risks a regulatory race to the bottom, potentially encouraging other jurisdictions to relax their own standards. Maintaining robust capital requirements is essential not only for domestic stability but also for preserving the United States’ role as a global anchor in banking regulation.

Courting Crisis: The Case Against Cutting Bank Capital Requirements

Comments

Want to join the conversation?