War Risks, Rate Cuts Affect Thai Banks’ Margins

Why It Matters

The earnings squeeze highlights how geopolitical uncertainty and monetary easing are reshaping Thai banks’ revenue mix, pressuring investors and prompting a shift toward fee‑based services for stability.

Key Takeaways

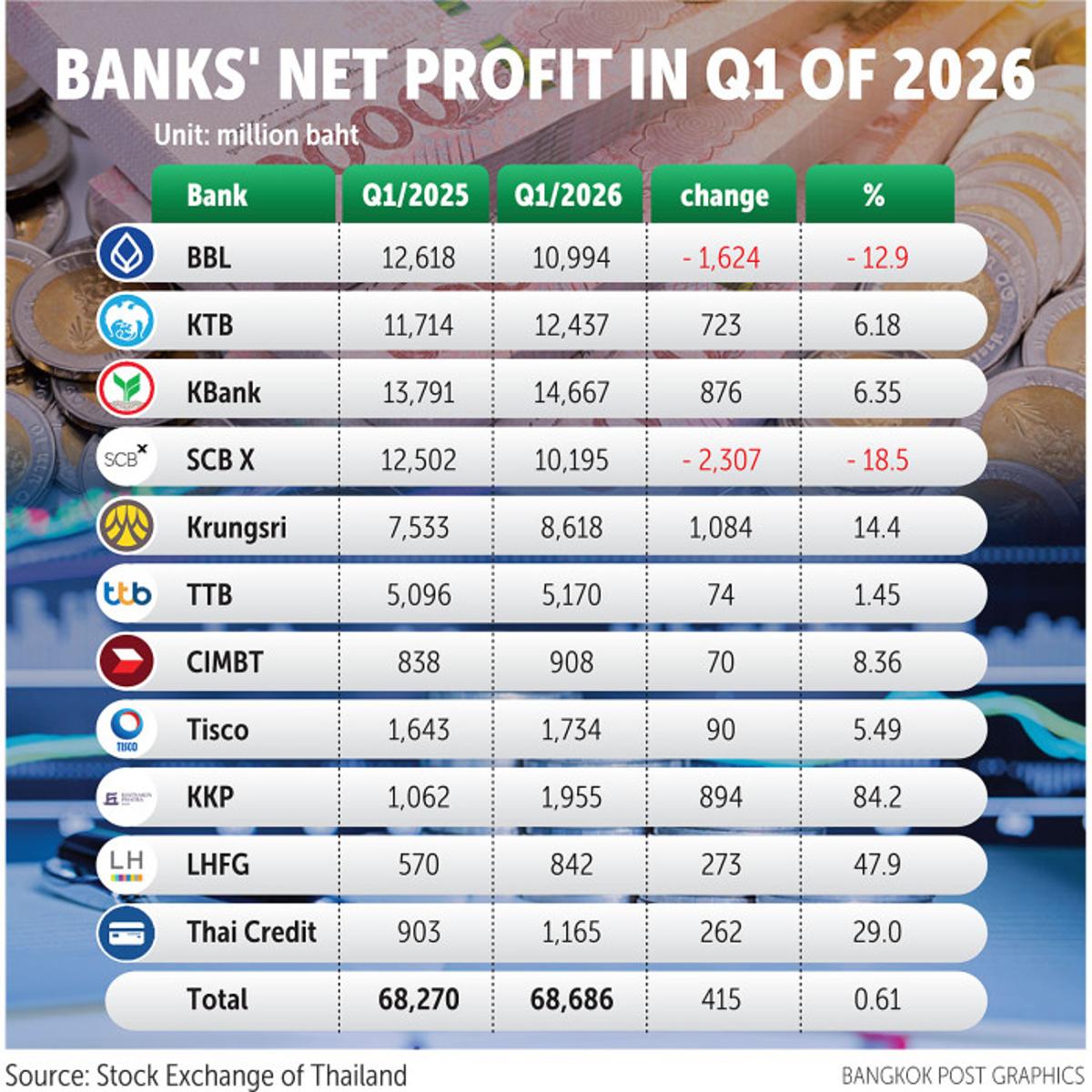

- •KBank profit up 6.3% to 14.6bn baht (~$410m), core down 3%

- •Bangkok Bank profit down 12.9% as NIM fell 12.3% after rate cuts

- •Krungthai Bank profit rose 6.2% despite 15.8% NIM drop, fees up 13.9%

- •SCB X profit fell 18.5% with NIM down 13.7% amid Middle East tensions

- •Krungsri profit up 14.4% thanks to higher loan yields and auto‑loan consolidation

Pulse Analysis

The first quarter of 2024 revealed a fragile profit landscape for Thailand’s banking sector. While headline net profits showed modest growth, the underlying net interest income—traditionally the backbone of bank earnings—contracted sharply. The Bank of Thailand’s aggressive policy‑rate cuts, aimed at supporting a slowing economy, reduced loan‑rate spreads, dragging net interest margins down 12%‑16% across the major lenders. At the same time, escalating tensions in the Middle East have heightened geopolitical risk, dampening consumer confidence and export demand, which further pressures loan growth and credit quality.

Individual banks responded in divergent ways. KBank managed to post a 6.3% profit increase to 14.6 billion baht, but its core earnings fell 3% once one‑off compensation was stripped out, underscoring the fragility of profit drivers. Bangkok Bank’s 12.9% profit decline reflected a 12.3% NIM compression, while Krungthai Bank turned the margin squeeze into an opportunity, offsetting a 15.8% NIM drop with a 13.9% surge in fee‑based income, especially wealth‑management services. SCB X suffered the steepest hit, with an 18.5% profit slide, whereas Krungsri leveraged higher loan yields and the integration of its auto‑loan arm to post a 14.4% profit rise.

For investors and corporate clients, the shift toward non‑interest income signals a strategic rebalancing that could stabilize earnings amid uncertain macro conditions. Analysts will watch the central bank’s next moves closely; any further rate easing could deepen NIM pressure, while a pivot to tighter policy might restore interest spreads but risk slowing loan growth. Meanwhile, banks that successfully expand fee‑based platforms and manage geopolitical exposure are likely to emerge with more resilient balance sheets, positioning them for long‑term shareholder value in a volatile regional environment.

War risks, rate cuts affect Thai banks’ margins

Comments

Want to join the conversation?

Loading comments...