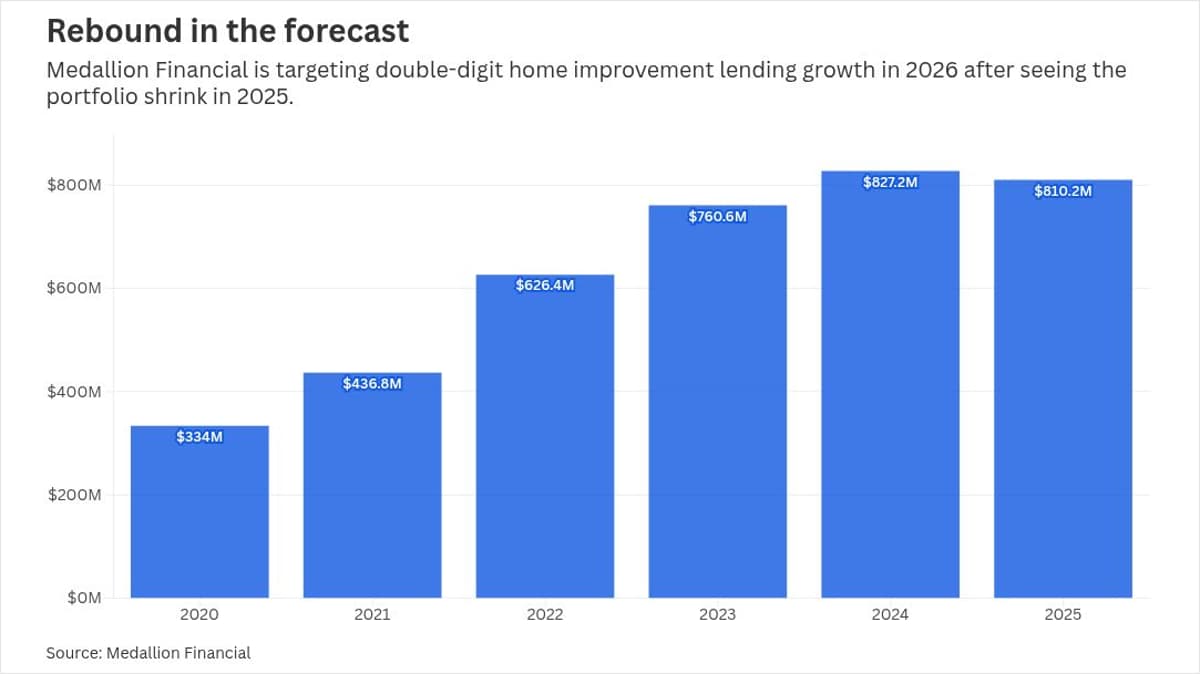

Medallion Stresses Home Improvement to Drive 2026 Growth

•February 19, 2026

0

Companies Mentioned

Why It Matters

Strong growth in home‑improvement lending diversifies Medallion’s revenue away from its dwindling taxi‑medallion legacy, positioning it for higher margins and resilience in a competitive consumer‑credit market.

Key Takeaways

- •Home‑improvement loans targeted for mid‑teens growth in 2026

- •Joel Cannon hired to lead seasoned home‑improvement lending team

- •Taxi‑medallion loans now under 1% of total portfolio

- •Recreational‑vehicle loans comprise over 60% of $2.6B assets

- •Quarterly net income rose 20% year‑over‑year in Q4

Pulse Analysis

The consumer‑credit landscape is increasingly dominated by niche loan products such as home‑improvement financing, which has benefited from rising renovation spending and low‑interest rates. As traditional collateral‑based lending, exemplified by taxi‑medallion loans, erodes, institutions like Medallion Financial are re‑engineering their balance sheets to capture higher‑margin, repeat‑borrower segments. This shift mirrors broader industry dynamics where fintech partnerships and data‑driven underwriting are accelerating loan origination volumes.

Medallion’s recruitment of Joel Cannon, a veteran from Regions Financial, signals a deliberate push to deepen expertise and accelerate pipeline velocity in the home‑improvement space. Cannon’s team brings proven sales processes and a network of borrowers, giving Medallion a competitive edge against peers such as First National Bank of Omaha, which also projects double‑digit loan growth. By consolidating its consumer‑lending focus around both home‑improvement and recreational‑vehicle products, Medallion can cross‑sell, improve risk diversification, and leverage its fintech collaborations that more than tripled originations from 2024 to 2025.

Financially, Medallion posted a 20% increase in fourth‑quarter net income, underscoring the profitability of its new loan mix. With taxi‑medallion exposure now below 1% and RV loans accounting for over 60% of a $2.6 billion portfolio, the firm enjoys a more balanced risk profile. While acquisitions remain off the table, the board remains open to a premium‑driven sale, reflecting confidence in the company’s growth trajectory. Analysts will watch whether the mid‑teens home‑improvement target materializes, as it could set a benchmark for other mid‑size lenders seeking to reinvent legacy assets.

Medallion stresses home improvement to drive 2026 growth

0

Comments

Want to join the conversation?

Loading comments...