Bitcoin Volatility Is Still Compressing, Dimming Year-End Rally Outlook

•December 10, 2025

0

Companies Mentioned

Why It Matters

Lower volatility diminishes speculative upside, signaling a tougher environment for Bitcoin’s year‑end rally and influencing trader risk‑management strategies.

Key Takeaways

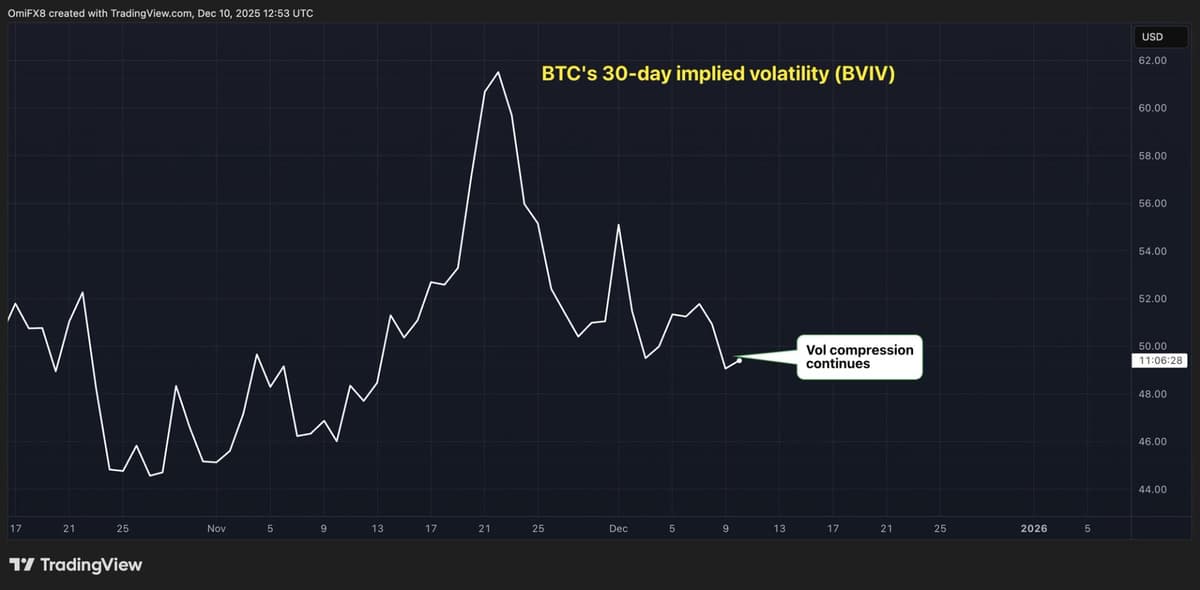

- •BTC 30‑day implied volatility fell to 49%.

- •S&P 500 VIX dropped to 17% in same period.

- •Volatility compression reduces upside rally probability.

- •Historical price‑volatility correlation turning negative since Nov 2024.

- •FOMC meeting may be last catalyst before year‑end.

Pulse Analysis

The recent drop in Bitcoin’s implied volatility mirrors a broader market trend where equity volatility, measured by the VIX, has also softened. This convergence suggests that crypto markets are increasingly responding to the same macro‑economic signals that temper risk appetite in traditional assets. For traders, a lower BVIV means tighter options pricing, reducing premium income opportunities while also signaling that large price swings are less expected in the near term.

Historically, Bitcoin’s price movements have been positively correlated with volatility spikes, a dynamic that attracted speculative traders seeking outsized gains. Since late 2024, however, that correlation has begun to invert, with price appreciation occurring amid declining volatility. This shift reflects the maturation of the crypto ecosystem, where institutional participation and more sophisticated hedging tools are dampening extreme price swings. The options market now plays a pivotal role in price discovery, and the compression of implied volatility compresses the range of potential outcomes, making breakout bets riskier.

Looking ahead, the Federal Reserve’s upcoming FOMC decision is likely the last major macro catalyst before the calendar year closes. Once monetary policy signals settle, the prevailing trend points toward further volatility decay, limiting the probability of a late‑year rally. Market participants may pivot to strategies that prioritize capital preservation, such as selling covered calls or reallocating to lower‑volatility assets. Understanding this volatility landscape is essential for investors aiming to navigate Bitcoin’s evolving risk‑reward profile in a market increasingly aligned with traditional financial dynamics.

Bitcoin Volatility Is Still Compressing, Dimming Year-End Rally Outlook

0

Comments

Want to join the conversation?

Loading comments...