Hut 8’s Tuesday Tumble Misguided and a Buying Opportunity: Benchmark

Why It Matters

The analyst’s bullish stance underscores Hut 8’s long‑term growth potential in AI‑driven compute and crypto mining, implying that the market may be undervaluing its expanding power assets and strategic positioning, which could drive future price appreciation.

Summary

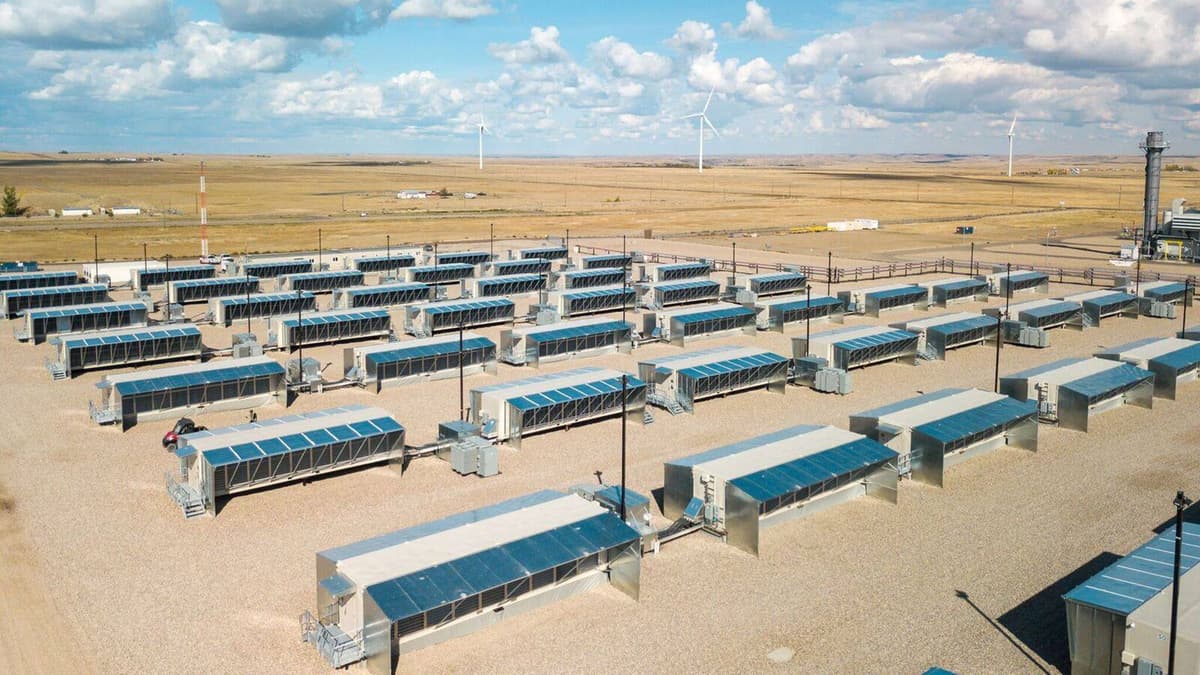

Hut 8’s shares fell nearly 13% after the Q3 earnings call failed to announce a hyperscaler tenant for its River Bend data centre, but Benchmark analyst Mark Palmer called the sell‑off short‑sighted and kept a buy rating with a $78 price target. The company posted record revenue and solid profitability, and its 300 MW facility in Louisiana is on track for late‑2026, with a pipeline that could scale to 1 GW and additional power capacity under exclusivity and diligence. Palmer highlighted Hut 8’s diversified assets—including a 64% stake in American Bitcoin and over 10,000 BTC—and its ability to shift between AI, high‑performance computing and bitcoin mining, suggesting further upside beyond the current valuation. The stock rebounded 4% to $50 amid a broader market decline.

Hut 8’s Tuesday Tumble Misguided and a Buying Opportunity: Benchmark

Comments

Want to join the conversation?

Loading comments...