Two Harbors Rejects UWM's Hostile $12.50 Offer

Why It Matters

The decision preserves the all‑stock CrossCountry transaction as the default, protecting shareholder upside and exposing governance friction in the mortgage‑servicing sector. It also underscores market doubts about UWM’s capacity to fund a cash takeover without additional financing.

Key Takeaways

- •Two Harbors rejects UWM's $12.50 cash bid as non‑superior

- •Board cites UWM leverage concerns and unchanged financing commitment

- •ISS advises shareholders to vote against CrossCountry merger

- •UWM stock slipped 7 cents after rejection announcement

- •Controlling shareholder ends 10b5‑1 plan, citing increased liquidity

Pulse Analysis

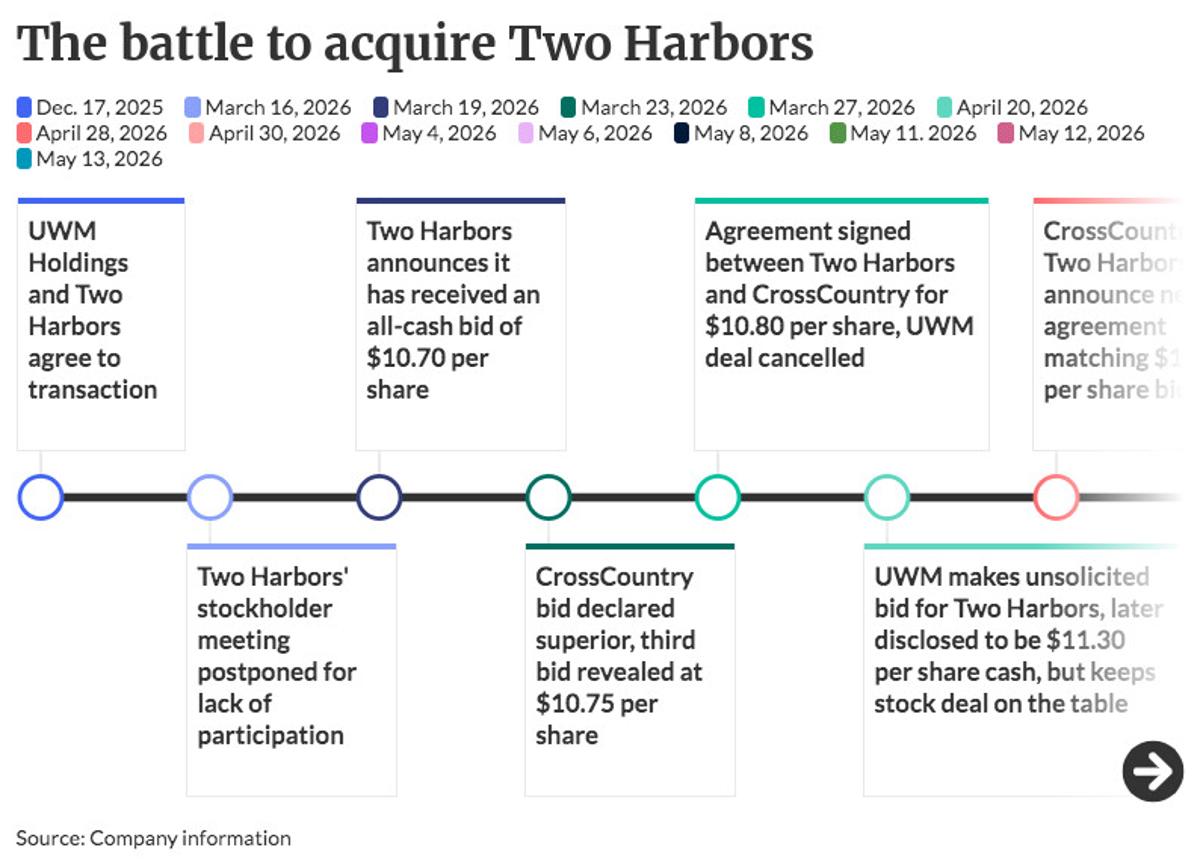

The showdown between Two Harbors, UWM Holdings, and CrossCountry Mortgage reflects a broader consolidation trend in the mortgage‑servicing industry. Two Harbors, a leading MSR (mortgage‑servicing‑rights) holder, has become the focal point of competing bids as lenders seek scale to manage low‑coupon servicing portfolios. While CrossCountry’s all‑stock offer values Two Harbors at $7.58 per share, UWM attempted a cash premium of $12.50, hoping to leverage its extensive servicing platform. The board’s rejection signals that shareholders are not convinced a cash deal outweighs the strategic benefits and financial risks associated with UWM’s leveraged balance sheet.

UWM’s financing posture is at the heart of the board’s concerns. The company did not increase its commitment from Mizuho, leaving the cash offer under‑secured amid Fitch’s warnings about UWM’s leverage ratios. Moreover, the lack of a meaningful premium beyond CrossCountry’s price raises questions about shareholder value creation. Institutional Shareholder Services (ISS) has taken a firm stance, urging investors to reject the CrossCountry merger unless a higher bid emerges, further pressuring the deal’s timeline. This proxy recommendation highlights the growing influence of proxy advisory firms in shaping merger outcomes, especially when financial metrics and governance issues intersect.

Beyond the immediate transaction, the episode sheds light on the evolving dynamics of mortgage‑servicing rights (MSR) markets. UWM’s claim of being the largest seller of low‑coupon MSRs, with $40 billion sold in Q1, underscores the massive capital flows tied to servicing assets. The termination of a Rule 10b5‑1 trading plan by UWM’s controlling shareholder, SFS Holdings, reflects heightened sensitivity to insider‑trading perceptions as the company navigates liquidity and float considerations. As the industry consolidates, the ability to fund acquisitions, manage leverage, and align shareholder interests will dictate which players emerge as dominant servicers in a low‑rate environment.

Two Harbors rejects UWM's hostile $12.50 offer

Comments

Want to join the conversation?

Loading comments...