Why It Matters

AI‑powered demand is reshaping semiconductor revenue streams, boosting high‑margin segments while creating supply bottlenecks that could curb growth in downstream consumer markets.

Key Takeaways

- •AI fuels 25.6% semiconductor market growth 2025

- •Memory firms report 29% revenue rise, driven by AI

- •Memory shortages threaten PC and smartphone shipments 2026

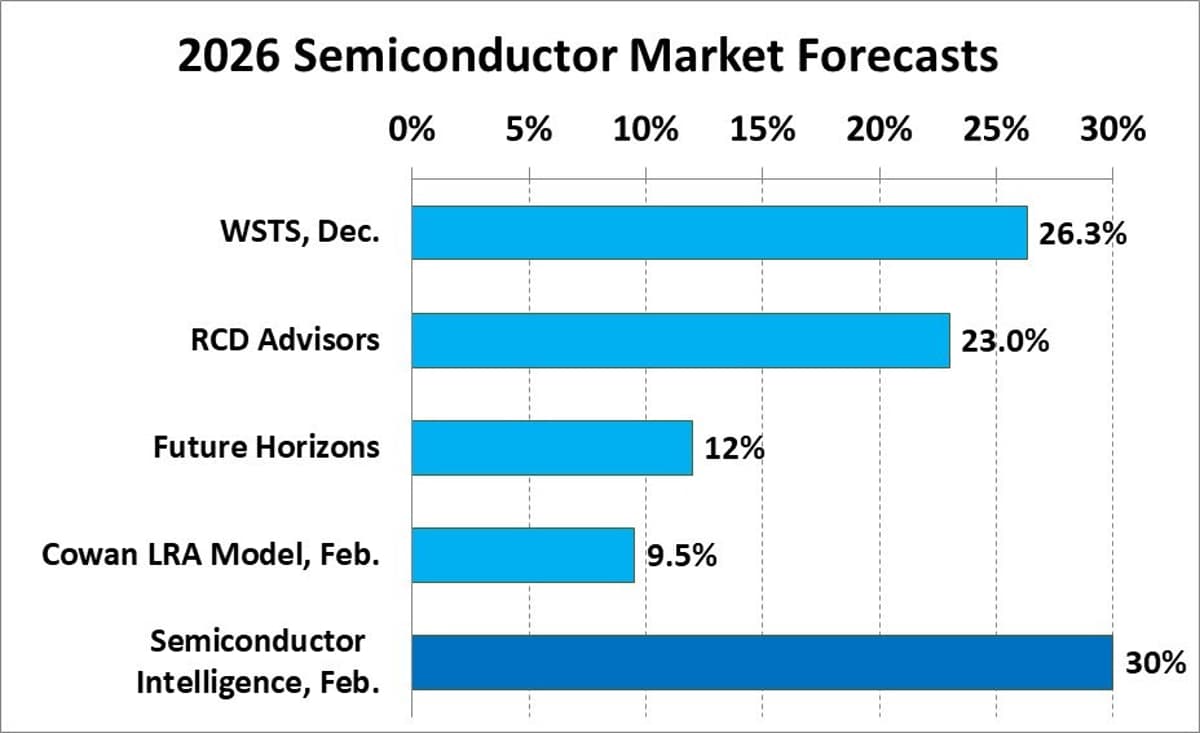

- •Forecasts split, high estimates exceed 20% growth 2026

Pulse Analysis

AI’s rapid adoption has become the primary catalyst for the semiconductor boom, pushing the industry’s 2025 revenue to an unprecedented $792 billion. Nvidia’s 65% revenue jump and the 29% collective growth of memory giants such as Samsung, SK Hynix, Micron, Kioxia and Sandisk illustrate how deep‑learning workloads are inflating demand for high‑bandwidth memory and advanced process nodes. This surge is not merely a short‑term spike; it reflects a structural shift where AI workloads dominate design roadmaps, prompting foundries to prioritize AI‑optimized chips and investors to reallocate capital toward AI‑centric portfolios.

The flip side of this AI‑driven expansion is a tightening of memory supplies that threatens the broader consumer ecosystem. Intel, Qualcomm and MediaTek have already flagged double‑digit revenue declines for Q1 2026, citing memory shortages that limit PC and smartphone production. IDC’s warning of potential shipment drops underscores a ripple effect: as memory prices climb, device manufacturers may delay launches or reduce bill‑of‑materials, eroding margins in traditionally stable markets. Companies less tied to AI, such as Texas Instruments and Infineon, are experiencing modest growth, highlighting a divergence between AI‑heavy and legacy segments within the semiconductor landscape.

Looking ahead, forecasts diverge sharply, with high‑end models projecting 23‑30% growth for 2026, while more conservative estimates linger around 9‑12%. The consensus among analysts who track AI trends suggests that, despite memory constraints, the sector will sustain over 20% expansion, buoyed by robust industrial and automotive demand and continued AI investment. Stakeholders should monitor supply‑chain adjustments, memory pricing dynamics, and the pace of AI adoption to gauge whether the sector can maintain its momentum or face a corrective slowdown as alternative markets adjust to the new AI‑centric reality.

AI Drives Strong Semiconductor Market in 2025-2026

0

Comments

Want to join the conversation?

Loading comments...