Memory Crunch Deepens Chasm Between Stock Winners and Losers

Why It Matters

The split underscores how supply‑chain constraints can reshape sector dynamics, rewarding pure‑play chipmakers while penalizing hardware vendors dependent on affordable memory. Investors and executives must adjust strategies to navigate heightened cost volatility.

Key Takeaways

- •AI demand fuels unprecedented memory chip shortage worldwide

- •Micron and Samsung stocks hit record highs on price spikes

- •HP, Nintendo earnings pressured by rising memory costs

- •Memory scarcity widens performance gap between tech winners and losers

- •Analysts expect continued volatility as AI projects expand

Pulse Analysis

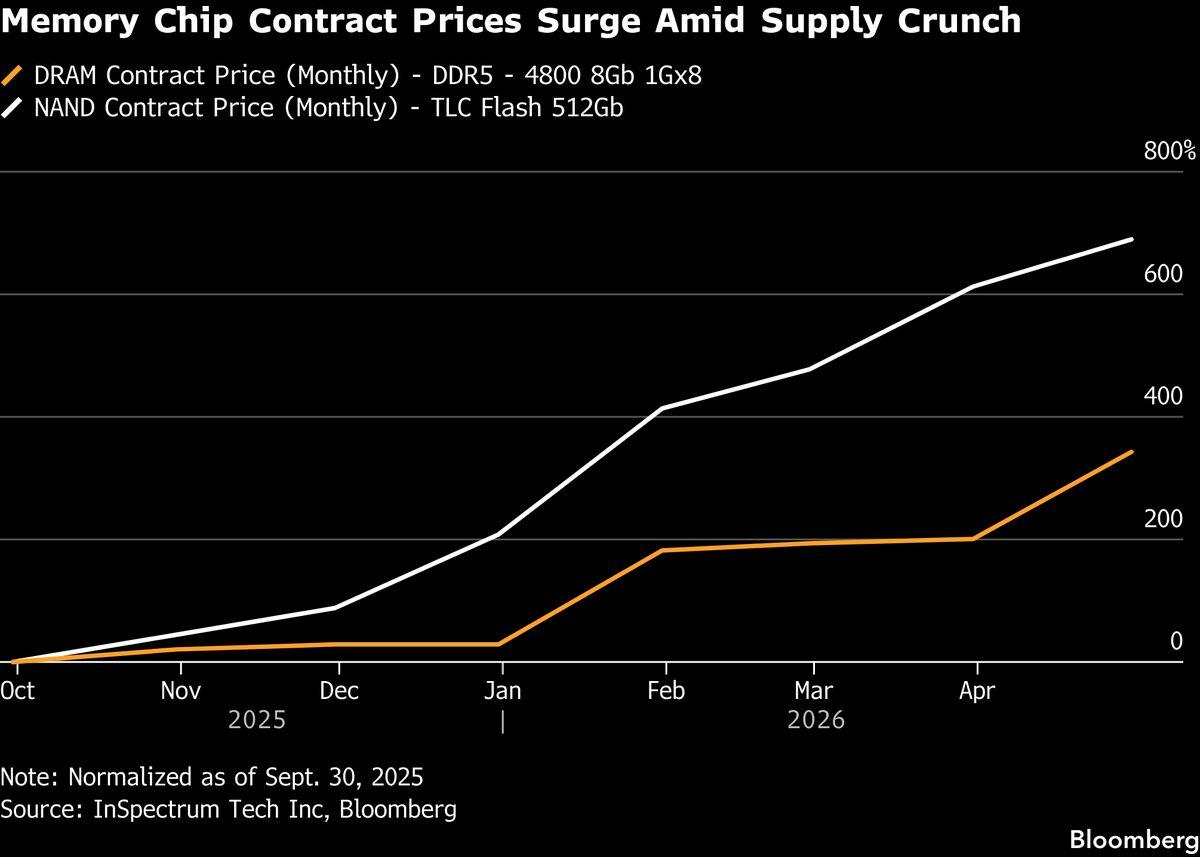

The surge in artificial‑intelligence workloads has turned memory chips into a bottleneck for the tech ecosystem. Training large language models and running inference at scale require terabytes of high‑bandwidth DRAM and NAND, pushing demand far beyond the capacity of existing fabs. Meanwhile, wafer capacity expansions are hampered by equipment lead times, geopolitical tensions, and the capital intensity of advanced process nodes. The resulting supply‑demand imbalance has lifted spot prices for DRAM and NAND to multi‑year highs, tightening margins for downstream manufacturers.

Equity markets have responded sharply, creating a pronounced divide between memory producers and consumer‑electronics firms. Micron Technology and Samsung Electronics posted earnings that beat expectations, buoyed by price premiums that more than offset modest volume growth, sending their shares to all‑time highs. In contrast, companies such as HP and Nintendo reported squeezed profit margins as the cost of embedded DRAM rose sharply, forcing them to either absorb the expense or pass it on to price‑sensitive customers. The divergence has amplified sector rotation, rewarding pure‑play chipmakers while penalizing hardware vendors reliant on inexpensive memory.

Looking ahead, the memory crunch is unlikely to ease until new fab capacity comes online, a process that can take 18‑24 months and requires billions of dollars in investment. Short‑term strategies such as inventory buffering and strategic sourcing may mitigate price volatility, but they also raise cash‑flow pressures for OEMs. Investors should monitor capacity‑expansion announcements from Taiwan Semiconductor Manufacturing Co. and SK Hynix, as well as any policy shifts that could accelerate domestic chip production in the United States. The balance of supply and demand will remain a key driver of earnings and stock performance across the tech sector.

Memory Crunch Deepens Chasm Between Stock Winners and Losers

Comments

Want to join the conversation?

Loading comments...