Companies Mentioned

Why It Matters

Fewer in‑center dialysis sites, particularly in rural areas, risk worsening care gaps and highlight the financial pressures reshaping the renal‑care market.

Key Takeaways

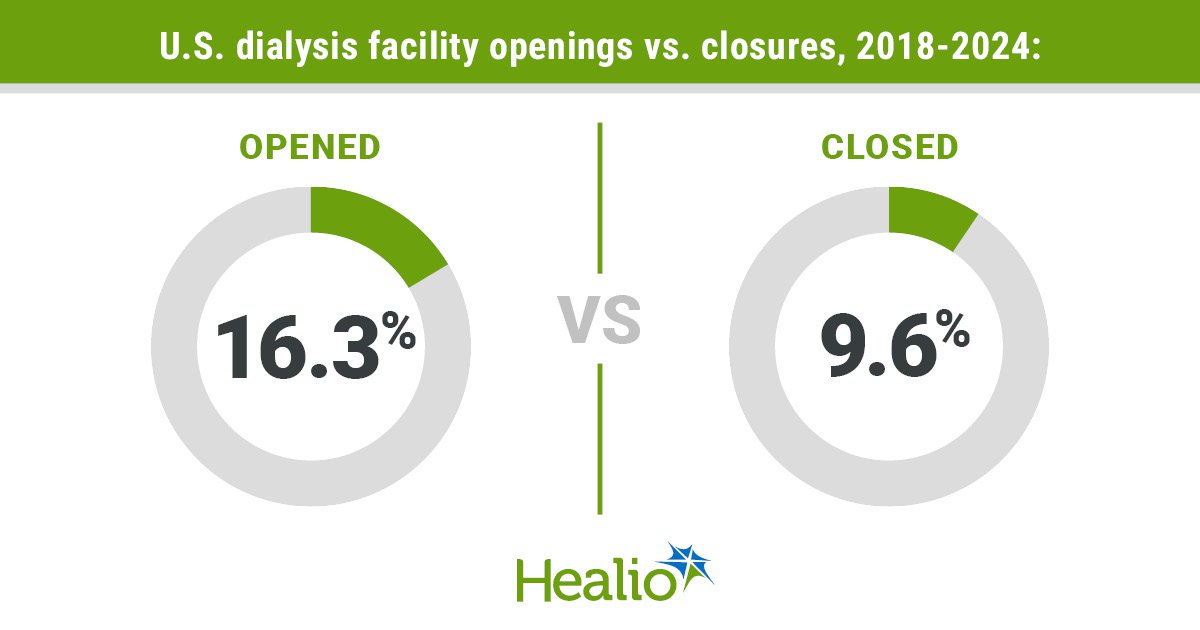

- •Opening-to-closure ratio fell from 8.9 (2018) to 0.8 (2024)

- •74 facilities closed vs. 56 opened in 2024, net loss of 18

- •Closed sites were smaller (median 58 patients) and more often rural Midwest

- •Declining patient volumes post‑COVID and profit pressures drive consolidation

- •Large duopoly (DaVita, Fresenius) earned ~$6 billion while closures rise

Pulse Analysis

The sharp reversal in dialysis clinic dynamics reflects deeper shifts in the U.S. renal‑care ecosystem. After a decade of expansion, the industry now faces a contraction driven by lower patient volumes post‑COVID, tighter reimbursement under the ESRD Treatment Choices model, and mounting fixed‑cost pressures. Smaller, rural facilities—once the backbone of community‑based care—are especially vulnerable because they lack the patient density needed to amortize multi‑million‑dollar capital investments. As a result, closures have clustered in the Midwest, where many clinics serve fewer than 60 patients on average.

Market concentration amplifies the impact. DaVita and Fresenius together command roughly 80% of the in‑center dialysis market and generated close to $6 billion in profit during the period of rising closures. Their scale enables aggressive pricing and the ability to absorb losses that would cripple independent operators. This duopolistic environment discourages new entrants and limits innovation, even as policymakers push for home‑dialysis and transplantation alternatives. Without targeted incentives or subsidies for safety‑net clinics, the current profit‑centric model is likely to perpetuate the decline of rural access points.

For patients, the fallout could be significant. Rural residents already travel longer distances for care, and the loss of nearby facilities may increase travel time, reduce treatment flexibility, and strain emergency response capabilities. Stakeholders—including CMS, state health agencies, and advocacy groups—must consider policies that protect low‑volume clinics, such as adjusted reimbursement rates or grant programs for hybrid home‑dialysis support. Addressing both the economic drivers and the geographic inequities will be essential to ensure continuity of care as the dialysis landscape continues to evolve.

Dialysis facility closures outpaced openings in 2024

Comments

Want to join the conversation?

Loading comments...