Can Both Spouses Claim the QSBS Exclusion? What Section 1202 Does and Doesn't Say About Married Couples

Key Takeaways

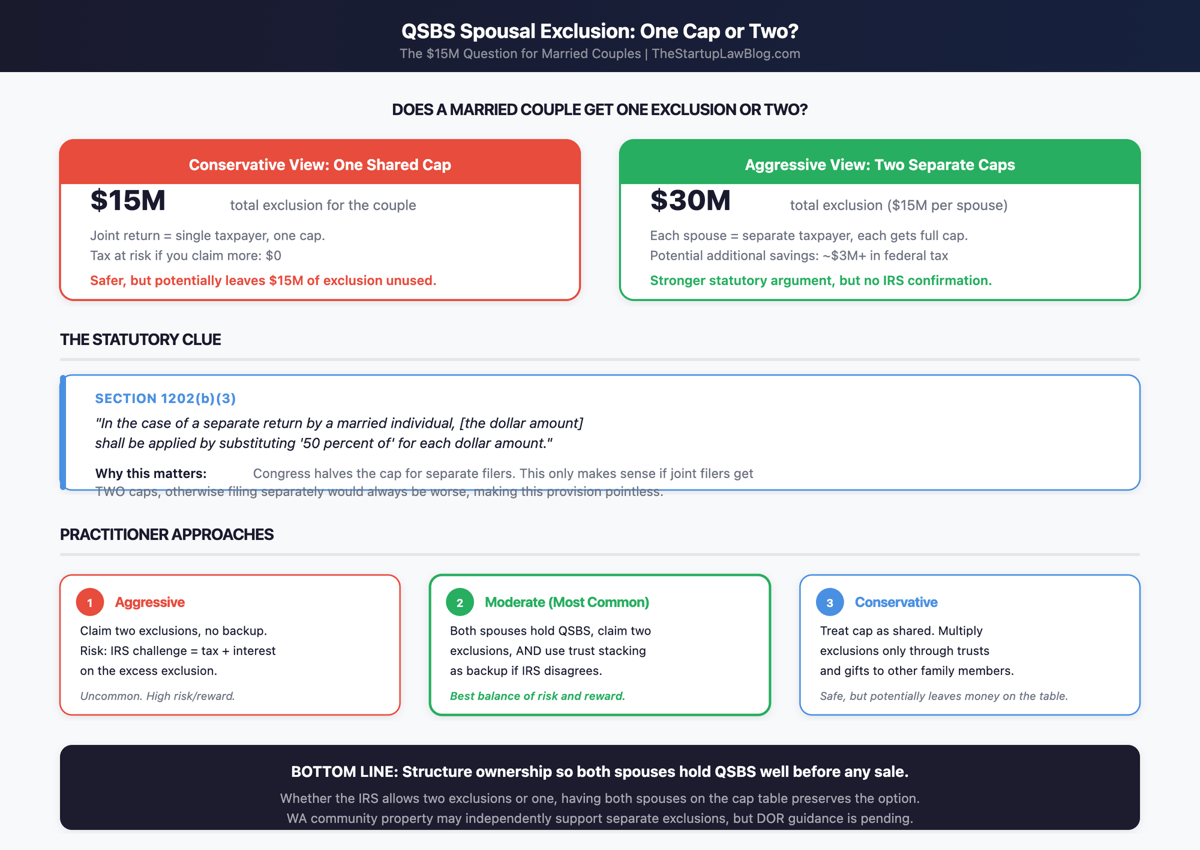

- •Statute caps QSBS gain at $15 million per taxpayer.

- •Married filing separately halves the cap to $7.5 million.

- •Joint return treatment remains unresolved, sparking two‑exclusion debate.

- •Community‑property states add ownership complexity for spouses.

- •Trust‑stacking offers a more defensible way to multiply exclusions.

Pulse Analysis

Qualified Small Business Stock (QSBS) under Section 1202 was created to spur investment in early‑stage companies by offering a substantial capital‑gains exclusion. The One Big Beautiful Bill Act of 2025 raised the per‑taxpayer cap to $15 million (adjusted for inflation after 2027) and introduced tiered holding‑period percentages, making the potential tax savings even larger. Because the exclusion applies at the federal level, any ambiguity in its application can translate into multi‑million‑dollar differences for founders and investors during a liquidity event.

The core of the controversy lies in the statute’s definition of “taxpayer.” While the code explicitly halves the exclusion for married‑filing‑separately returns, it offers no guidance for joint returns, leaving courts and the IRS to interpret whether a married couple is treated as a single taxable unit or as two independent taxpayers. Proponents of a dual‑exclusion view point to the halving provision as evidence that Congress intended to prevent double‑dipping only when spouses file separately. Opponents argue that, absent explicit language, the default is one exclusion per return, a stance reinforced by the IRS’s historical use of married‑filing‑separately penalties. Community‑property jurisdictions further complicate matters by assigning half‑ownership of assets to each spouse regardless of title, raising questions about how the exclusion cap should be allocated.

In practice, tax advisors balance aggressive spousal gifting with more defensible trust‑stacking structures. A gift to a spouse before a sale can, in theory, double the exclusion but hinges on the unresolved joint‑return interpretation and may trigger step‑transaction challenges. By contrast, transferring QSBS into irrevocable non‑grantor trusts creates distinct taxpayers with clear per‑entity caps, offering stronger legal footing. Most practitioners adopt a hybrid approach: they position spouses to claim separate exclusions while simultaneously establishing trust stacks as a fallback. This layered strategy mitigates exposure to IRS challenges while preserving the upside of potentially saving tens of millions in taxes.

Can Both Spouses Claim the QSBS Exclusion? What Section 1202 Does and Doesn't Say About Married Couples

Comments

Want to join the conversation?