German Industrial Production Rebounds in April on Higher Energy, Construction Output

Why It Matters

The data signals a tentative turnaround in Germany’s manufacturing engine, crucial for Europe’s export‑oriented growth, but the uneven sector performance warns of lingering demand weakness. Investors and policymakers will watch whether construction‑led momentum can translate into sustained industrial expansion.

Key Takeaways

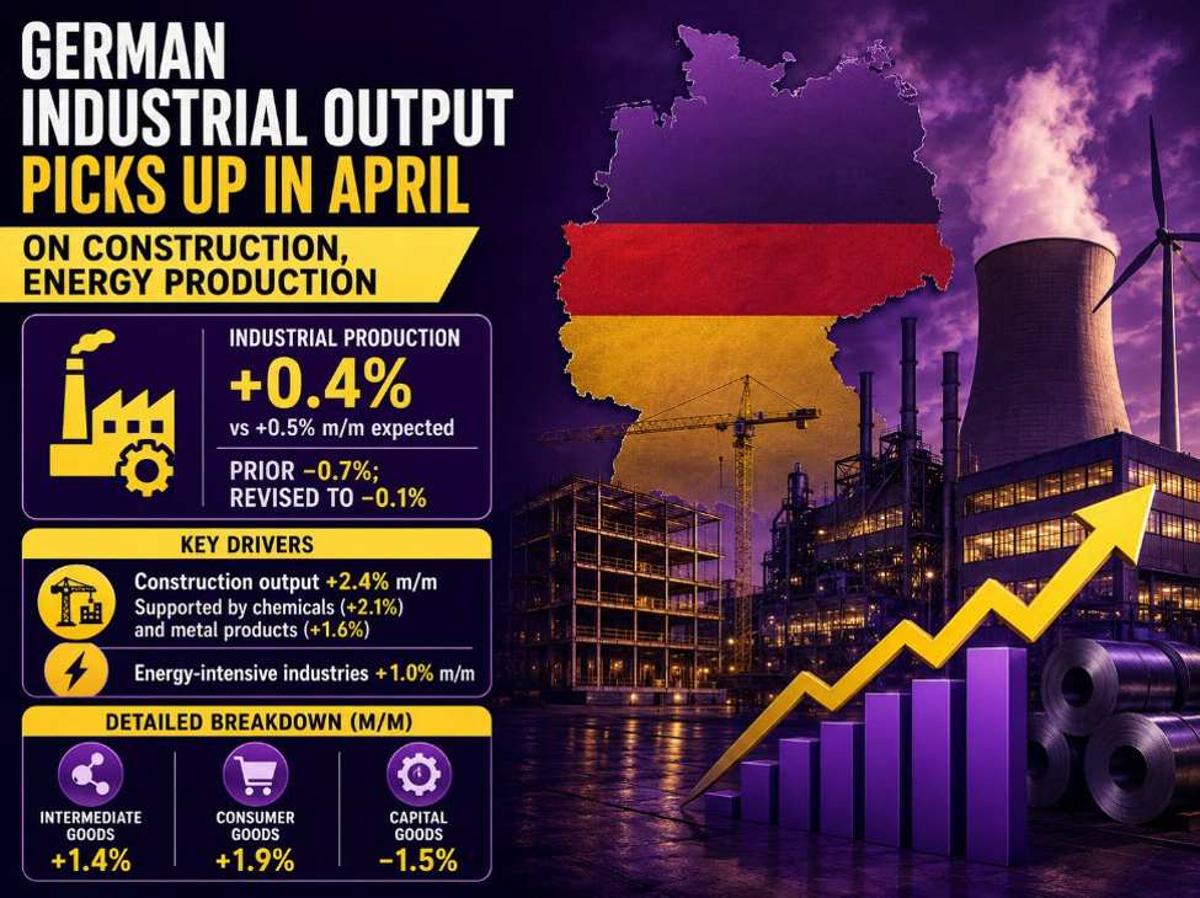

- •German industrial output rose 0.4% in April, beating forecasts.

- •Construction output surged 2.4%, driven by chemicals and metal manufacturing.

- •Energy‑intensive sectors added 1.0% growth, offsetting capital goods decline.

- •Intermediate and consumer goods production increased over 1% each month.

- •Core manufacturing excluding energy and construction remained flat.

Pulse Analysis

Germany’s industrial production posted a modest 0.4 % month‑on‑month rise in April, outpacing the 0.5 % consensus forecast and correcting a previously reported 0.7 % decline to a near‑flat –0.1 % figure for March. The modest rebound reflects a broader stabilization after a turbulent first quarter, where energy price volatility and supply‑chain disruptions weighed heavily on output. While the headline number suggests improvement, the underlying core manufacturing index—excluding energy and construction—showed no change, underscoring that the uptick is concentrated in specific sub‑sectors rather than a wholesale recovery.

The construction sector was the primary engine, posting a 2.4 % jump, with chemicals (+2.1 %) and metal‑product manufacturing (+1.6 %) leading the surge. This rebound aligns with renewed investment in infrastructure projects and a gradual easing of material shortages that plagued the previous months. Energy‑intensive industries added another 1.0 % gain, reflecting lower natural‑gas costs and improved plant utilization. However, capital goods output slipped 1.5 %, hinting that firms remain cautious about expanding equipment inventories amid lingering demand uncertainty.

Analysts view the April data as a tentative positive signal for Germany’s export‑driven economy, but they caution that the recovery remains uneven. The stagnation in core manufacturing suggests that demand from key trading partners, especially the United States and China, has yet to translate into sustained production gains. Policy makers may respond by maintaining fiscal incentives for construction and energy efficiency upgrades, while the European Central Bank watches inflation trends tied to industrial activity. Investors should monitor upcoming PMI surveys and the Bundesbank’s outlook for a clearer picture of whether the current momentum can be sustained.

German industrial production rebounds in April on higher energy, construction output

Comments

Want to join the conversation?

Loading comments...