Mining for Key Energy-Transition Minerals Is Not a Major Source of Global Greenhouse Gas Emissions, ICMM Research Finds

•March 10, 2026

0

Why It Matters

Understanding mining’s true emissions share helps policymakers and investors assess climate risks without over‑estimating the sector’s impact, guiding more balanced energy‑transition strategies.

Key Takeaways

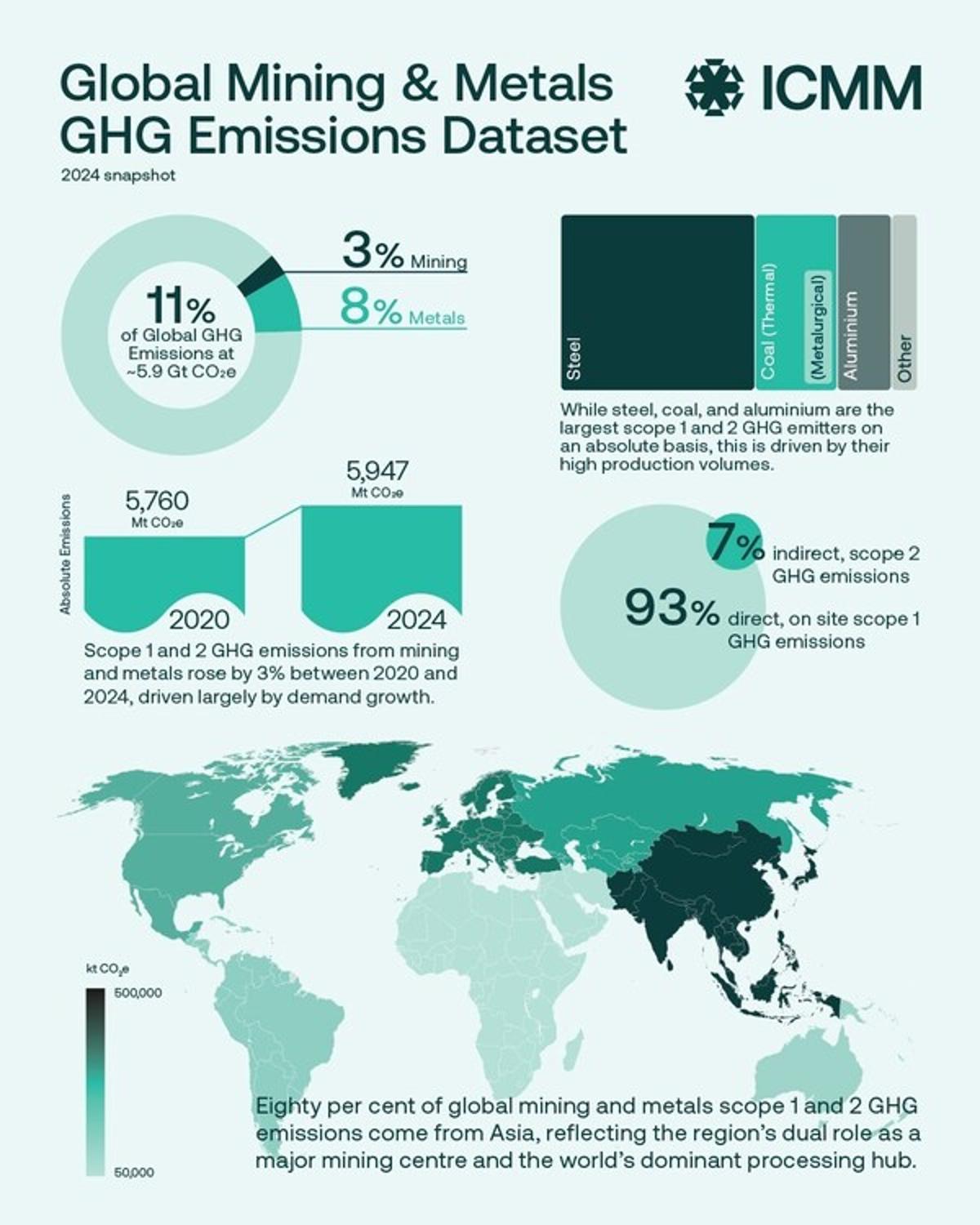

- •Dataset covers 1,700 facilities, 87% production of 14 commodities.

- •Scope 1 and 2 emissions modeled for 2024 sector-wide.

- •Mining sector not major contributor to global GHG emissions.

- •Data excludes certain refining stages and gases like SF6.

- •Designed for high-level insights, not corporate benchmarking.

Pulse Analysis

The surge in demand for copper, lithium, nickel and other energy‑transition minerals has sparked intense scrutiny of mining’s carbon intensity. By aggregating facility‑level data from 1,700 sites and modelling the remaining 13% of global output, ICMM delivers the first comprehensive, sector‑wide picture of scope 1 and scope 2 emissions. This baseline lets analysts place mining alongside power generation, steel and cement, revealing that, despite its energy‑intensive processes, the sector’s share of global GHG emissions remains modest.

ICMM partnered with Wood Mackenzie to apply a consistent GHG‑Protocol‑aligned methodology, ensuring comparability across commodities and regions. The dataset captures 87% of production for 14 commodities, while the residual gap is filled with regional averages. Notably, the dataset omits certain downstream refining stages and gases such as hydrofluorocarbons and SF₆, limiting its granularity. Unlike corporate inventories, which reflect individual company targets and controls, this model‑based estimate is unsuitable for asset‑level benchmarking but valuable for macro‑level policy analysis and investment screening.

For policymakers, investors and sustainability officers, the dataset offers a transparent reference point to calibrate climate‑risk models and design sector‑specific decarbonisation pathways. It also underscores the need for continued data improvement, encouraging broader collaboration to fill current gaps. As the energy transition accelerates, reliable emissions data will be pivotal in balancing mineral supply security with climate objectives, shaping the next phase of sustainable mining practices.

Mining for key energy-transition minerals is not a major source of global greenhouse gas emissions, ICMM research finds

0

Comments

Want to join the conversation?

Loading comments...