Southeast Asia Sees New Wave of Deepwater Gas Projects

Why It Matters

The gas will be crucial for regional energy security as legacy supplies wane, but the narrow profit margins make successful execution a litmus test for Southeast Asia’s ability to attract investment in high‑cost deepwater assets.

Key Takeaways

- •28 trillion cubic feet targeted across six deepwater developments.

- •Capital spending exceeds US$20 billion, measured in 2026 dollars.

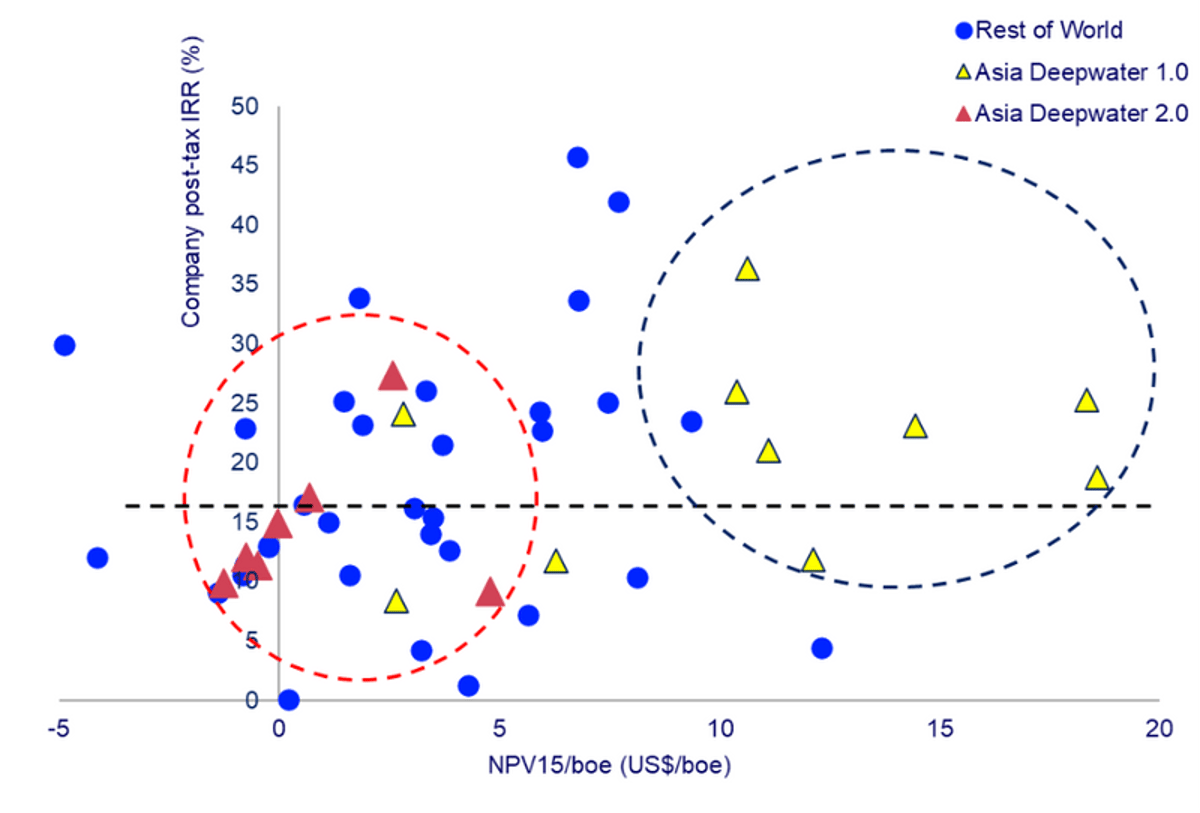

- •Most projects forecast IRR under 15 %, below global deepwater averages.

- •A 20 % cost rise or price drop cuts NPV by ~150 %.

- •Delays of three years can erase half of a project's value.

Pulse Analysis

The second wave of deep‑water gas development marks a strategic pivot for Southeast Asia as its shallow‑water and onshore fields mature. With Indonesia’s offshore gas output down more than 12 % since 2018 and Brunei needing an additional 500 million cubic feet per day after 2030, the region faces a looming supply gap. Deepwater projects promise to fill that void, delivering domestic gas for power generation and feeding LNG export terminals that have become vital revenue streams amid ongoing geopolitical tensions in Europe and the Middle East.

However, the economics are precarious. Wood Mackenzie’s model shows most projects hovering around a 15 % internal rate of return, well below the 20‑25 % benchmark typical of other basins. Sensitivity analysis reveals that a 20 % rise in capex or a comparable dip in gas prices can slash net present value by roughly 150 %, while a three‑year delay can wipe out half the project's value. These thin margins demand robust fiscal frameworks—such as risk‑sharing contracts or production‑linked royalties—to cushion operators against cost inflation and supply‑chain disruptions that have been amplified by the Middle East conflict.

If successfully executed, the deep‑water surge could cement Southeast Asia’s energy self‑sufficiency and reinforce its position in the global LNG market. Accelerated delivery models, exemplified by Eni’s five‑year discovery‑to‑first‑gas target, aim to mitigate execution risk. Investors will watch closely as the next five years determine whether the region can marshal the capital, technology, and policy support needed to turn these high‑cost assets into reliable supply pillars, reshaping the energy landscape of the Indo‑Pacific.

Southeast Asia Sees New Wave of Deepwater Gas Projects

Comments

Want to join the conversation?

Loading comments...