Ginnie Mae Pauses Delinquency Rules Amid FHA Waterfall Shift

Companies Mentioned

Why It Matters

The adjustment reshapes how investors evaluate credit risk in Ginnie‑backed mortgage‑backed securities, potentially influencing pricing and capital allocation. It also underscores regulatory responsiveness to FHA policy shifts that directly affect the MBS market.

Key Takeaways

- •Ginnie Mae excludes TPP loans from delinquency ratios starting April 2.

- •Pause lasts at least 60 days before standard reporting resumes.

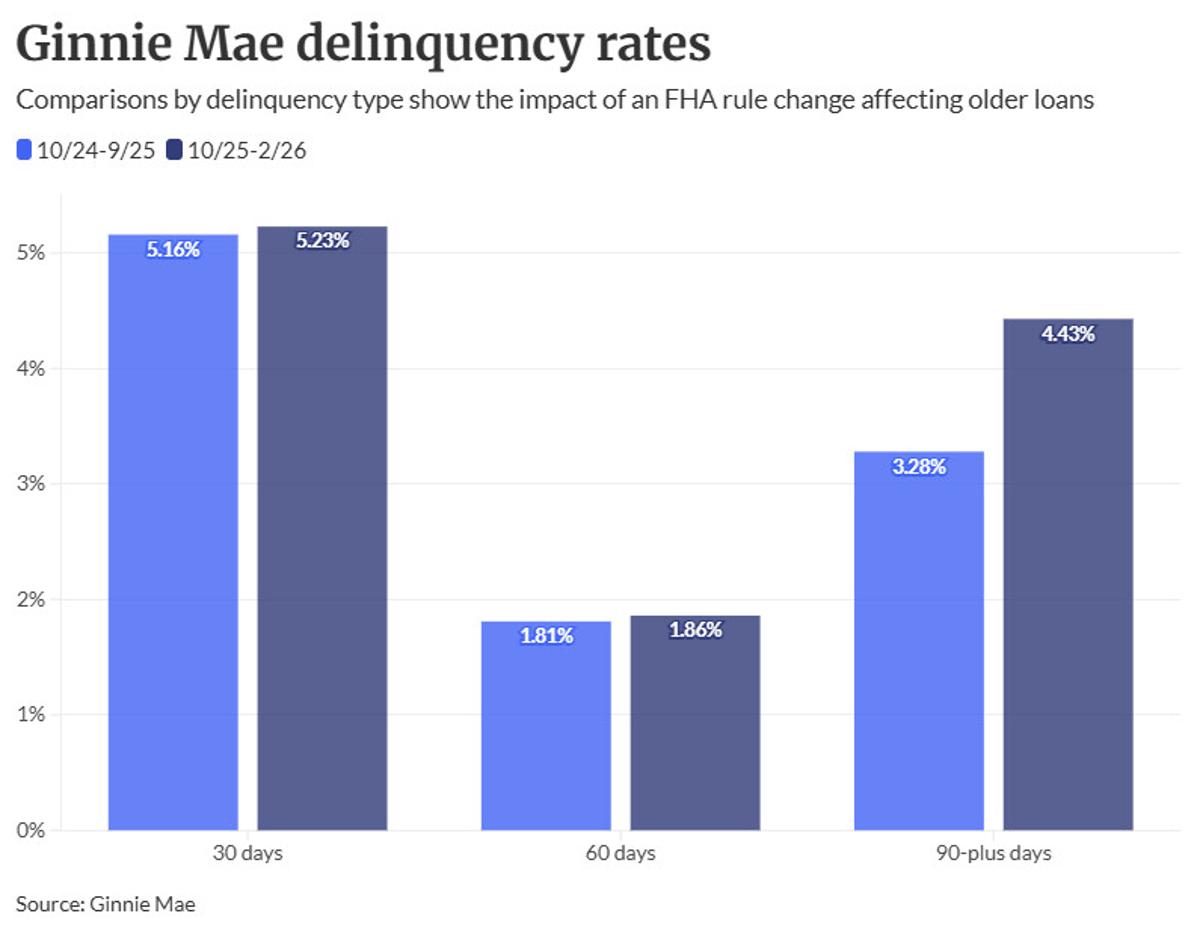

- •FHA waterfall change caused >1% rise in three‑month delinquencies.

- •30‑ and 60‑day delinquency rates unchanged, up <10 basis points.

- •Potential future changes to delinquency thresholds under review.

Pulse Analysis

The Federal Housing Administration’s recent overhaul of its delinquency "waterfall"—the hierarchy of loss‑mitigation tools—has pushed a sizable cohort of older loans onto trial payment plans (TPPs). Under the new rules, borrowers who previously could repeatedly request partial‑claim relief must now enter a TPP after exhausting pandemic‑era options, and they face stricter limits on subsequent relief requests. Ginnie Mae, the government agency that guarantees the majority of FHA‑backed mortgage‑backed securities, observed a sharp uptick in three‑month delinquencies and chose to temporarily exclude TPP‑bound loans from its compliance ratios to avoid distorting portfolio‑level risk metrics.

For investors and servicers, the pause signals a short‑term recalibration of credit‑risk assessments for Ginnie‑backed MBS. By removing TPP loans—often in a transitional distress phase—from delinquency calculations, Ginnie aims to present a clearer picture of underlying performance, which can affect yields, spreads, and capital requirements for holders of these securities. The 60‑day notice period gives market participants time to adjust models and reporting processes, while the potential revision of delinquency thresholds hints at a longer‑term shift in how the agency will monitor and enforce credit quality standards.

Looking ahead, the episode highlights the sensitivity of the secondary‑mortgage market to policy tweaks at the FHA level. As the FHA continues to refine its loss‑mitigation framework, Ginnie Mae may need to adapt its reporting rules more frequently, creating a dynamic compliance environment. Stakeholders should monitor forthcoming guidance for any permanent changes to delinquency thresholds, which could reshape risk‑based pricing and influence the broader housing finance ecosystem.

Ginnie Mae pauses delinquency rules amid FHA waterfall shift

Comments

Want to join the conversation?

Loading comments...