HECM Lenders See Subdued Numbers to Start the Year

•March 3, 2026

0

Why It Matters

The decline signals shifting borrower preferences toward private, flexible reverse‑mortgage solutions, potentially reshaping lender competition and FHA’s market share. Understanding this trend is critical for investors and policymakers monitoring senior housing finance.

Key Takeaways

- •HECM endorsements fell 20.7% Jan‑Feb 2024

- •Proprietary reverse‑mortgage products gaining market share

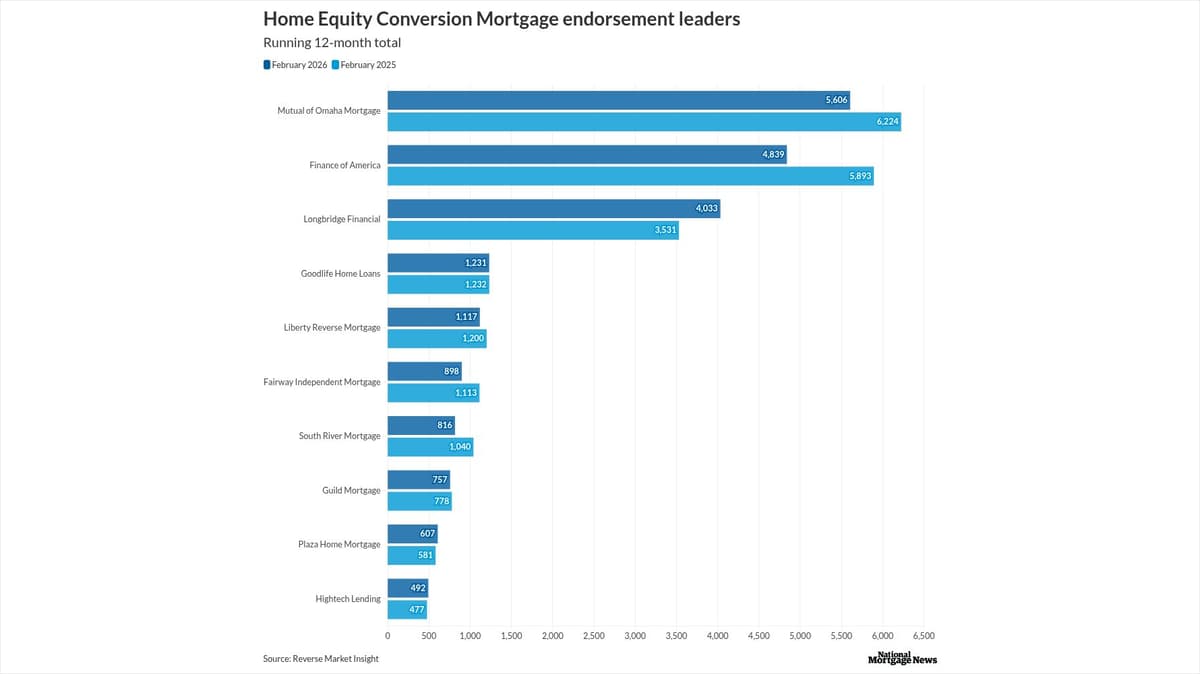

- •Mutual of Omaha led February HECM endorsements

- •Home equity wealth hit $14.7 trillion, up 1.9%

- •Data on proprietary loans remains unavailable publicly

Pulse Analysis

The reverse‑mortgage sector entered 2026 with a noticeable contraction in FHA‑backed Home Equity Conversion Mortgage (HECM) activity. According to Reverse Market Insight, endorsements fell 20.7% between January and February and are 26.6% lower than the same month a year earlier. Analysts attribute the dip to a combination of seasonal shutdowns, lingering political uncertainty, and growing competition from non‑government products. Yet the underlying pool of senior homeowners remains robust, with a record $14.7 trillion in housing wealth, suggesting demand for equity‑based financing persists despite short‑term weakness.

During the past twelve months, leading originators have launched proprietary reverse‑draw loans that blend features of home‑equity lines of credit with higher loan limits and no mortgage‑insurance premiums. These private offerings promise lower upfront costs and greater flexibility, appealing to borrowers who seek cash without the constraints of FHA guidelines. While exact origination figures are not publicly disclosed, anecdotal evidence points to a steady erosion of HECM market share as lenders like Finance of America pivot toward their own suites. The rise of shared‑appreciation contracts further diversifies the senior‑lending landscape, providing alternatives that defer payments until contract termination.

The shift toward proprietary products carries strategic implications for both lenders and policymakers. Traditional HECM providers must reassess pricing, service models, and marketing to retain relevance, while regulators may need to evaluate consumer protection standards for private reverse‑mortgage arrangements. Investors watching the senior‑housing finance market should monitor lender rankings—Mutual of Omaha currently leads February endorsements—and the pace at which proprietary volumes grow. If the trend continues, FHA‑backed reverse mortgages could lose a sizable portion of their foothold, reshaping the financing options available to America’s aging homeowners.

HECM lenders see subdued numbers to start the year

0

Comments

Want to join the conversation?

Loading comments...