Lower Mortgage Rates Boost Refinancing While Purchase Activity Slows

•March 9, 2026

0

Why It Matters

Lower rates are reviving refinancing demand, boosting lender volume, while the purchase slowdown highlights persistent supply constraints that could pressure home prices.

Key Takeaways

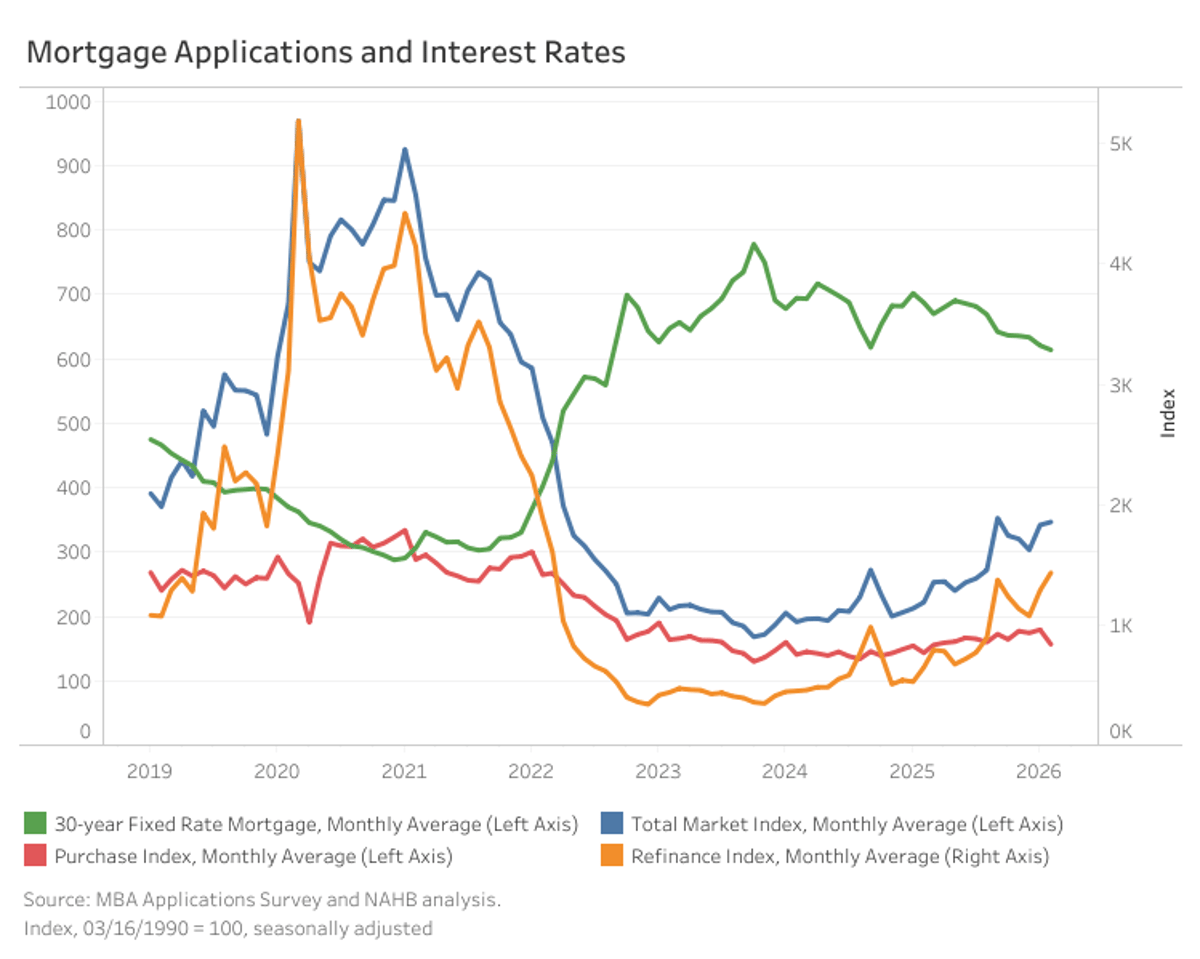

- •Mortgage applications up 1.5% month‑over‑month.

- •30‑yr fixed rate fell to 6.14%, three‑year low.

- •Refinancing rose 11.3%; purchases fell 12.3%.

- •ARM share grew to 8.3% of applications.

- •Average loan size reached $414,800, up 3.2%.

Pulse Analysis

The plunge of the 30‑year fixed mortgage rate to 6.14%—its lowest level in three years—mirrors a broader dip in the 10‑year Treasury yield, a relationship that has long driven home‑loan pricing. This rate compression has reignited refinancing activity, with applications climbing 11.3% month‑over‑month and overall market volume up 1.5% from January. Borrowers are seizing the opportunity to lock in lower payments, boosting the average refinance loan size to $391,800. Lenders, in turn, are seeing tighter spreads but benefit from higher volume, reinforcing the cyclical link between bond markets and mortgage demand.

Concurrently, adjustable‑rate mortgages (ARMs) are gaining traction, now representing 8.3% of all applications—a rise of 1.2 percentage points from the previous month. The 18% month‑over‑month surge in ARM filings reflects consumer appetite for lower initial rates amid lingering rate uncertainty. While ARMs can offer short‑term savings, they expose borrowers to future rate resets, a risk that may become pronounced if Treasury yields rebound. Lenders are responding by expanding ARM product offerings and emphasizing rate‑cap disclosures, signaling a strategic shift to capture price‑sensitive segments without compromising underwriting standards.

The surge in refinancing contrasts sharply with a 12.3% decline in purchase applications, underscoring the strain of limited inventory and seasonal weather disruptions on home‑buying activity. Larger average purchase loans—now $446,300—suggest that buyers who remain in the market are targeting higher‑priced homes, potentially inflating price appreciation in constrained segments. As rates stabilize, the market may see a gradual rebalancing: refinancers exiting the pipeline and new buyers re‑entering as inventory improves. Stakeholders should monitor mortgage‑backed securities spreads and housing supply metrics to gauge the durability of this dual‑trend environment.

Lower Mortgage Rates Boost Refinancing While Purchase Activity Slows

0

Comments

Want to join the conversation?

Loading comments...