Prepayments Hit 4-Year High After Mortgage Rates Eased

Companies Mentioned

Why It Matters

Higher prepayments accelerate the amortization of existing mortgage‑backed securities, reshaping cash‑flow expectations for investors, while the rise in late‑stage delinquencies signals emerging credit risk that could affect lenders and policymakers.

Key Takeaways

- •Prepayment speed rose to 1.06% in March, a four‑year high

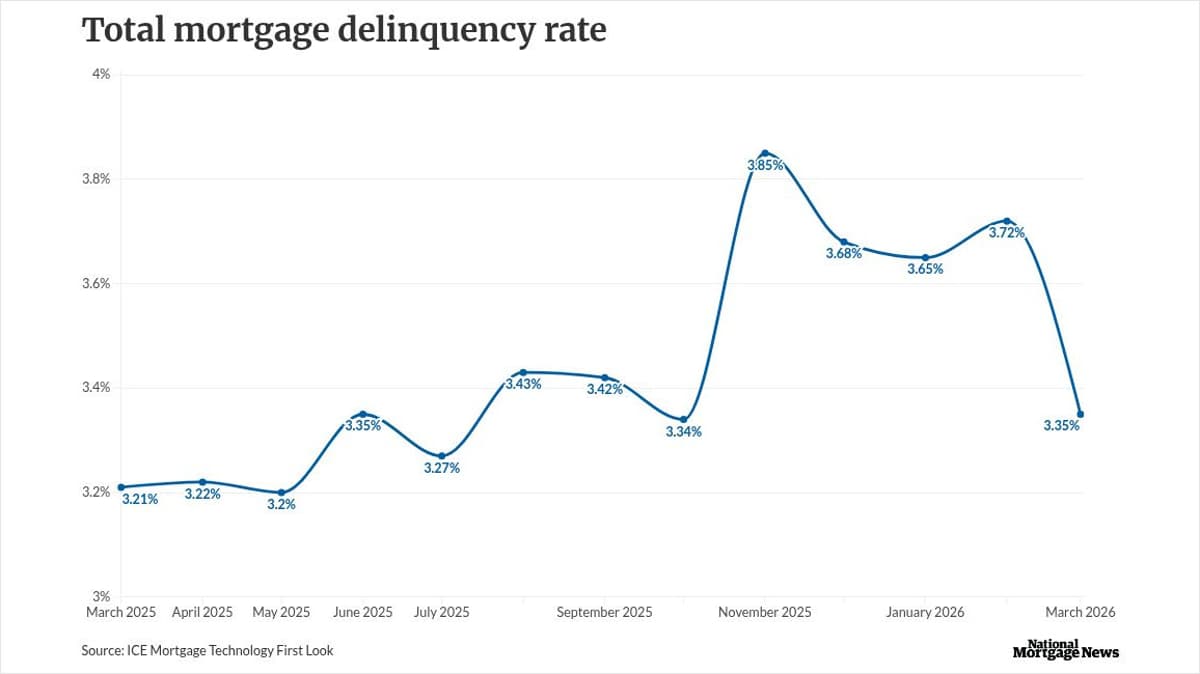

- •Delinquency rate fell to 3.35% overall, down 37 bps month‑over‑month

- •Late‑stage delinquencies and foreclosures increased, hitting six‑year peak

- •Mortgage refinance activity boosted by declining rates despite geopolitical shock

- •Southern states led non‑current mortgage shares, with Mississippi at 8.01%

Pulse Analysis

The latest ICE Mortgage Technology First Look report shows prepayment speeds climbing to 1.06% in March, the highest level since 2020. The jump follows a winter of falling mortgage rates that rekindled refinance activity, even as the Iran‑Israel conflict briefly nudged rates upward. Lower fixed‑rate averages compared with a year ago made it attractive for borrowers to replace higher‑cost loans, pushing the year‑over‑year prepayment rate up 78.4%. This surge improves cash‑flow timing for mortgage‑backed securities but also accelerates the amortization of existing pools.

At the same time, overall delinquency metrics improved, with the national non‑current rate slipping to 3.35% in March, a 37‑basis‑point decline from February. Early‑stage delinquencies fell and cure rates rose 27%, reflecting the seasonal health of the housing market. However, the report flags a growing tail risk: borrowers 90 days past due and foreclosure filings rose, pushing the foreclosure inventory to a six‑year high of 273,000 homes. The divergence between early‑stage relief and late‑stage distress suggests lenders must monitor credit‑risk pipelines closely.

Geography adds another layer of nuance. Southern states such as Mississippi, Louisiana and Alabama posted the highest non‑current ratios, exceeding 7%, while markets like Hawaii, Colorado and Montana remained under 2.3%, indicating resilient local economies. For investors in agency MBS and CMBS, these regional disparities affect expected loss assumptions and pricing. Policymakers may also watch the late‑stage delinquency uptick as a leading indicator of broader economic stress, especially if mortgage rates climb again. Overall, the mixed picture underscores the need for dynamic risk management in a volatile rate environment.

Prepayments hit 4-year high after mortgage rates eased

Comments

Want to join the conversation?

Loading comments...