Taxes, Insurance Eat 21% of Mortgage Payments

•March 5, 2026

0

Why It Matters

Escrow‑based tax and insurance costs erode affordability, reshaping buying power and influencing market dynamics across the United States.

Key Takeaways

- •Tax and insurance average 21% of mortgage payments.

- •Some markets exceed one‑third of monthly payment.

- •First‑time buyers often unaware of escrow costs.

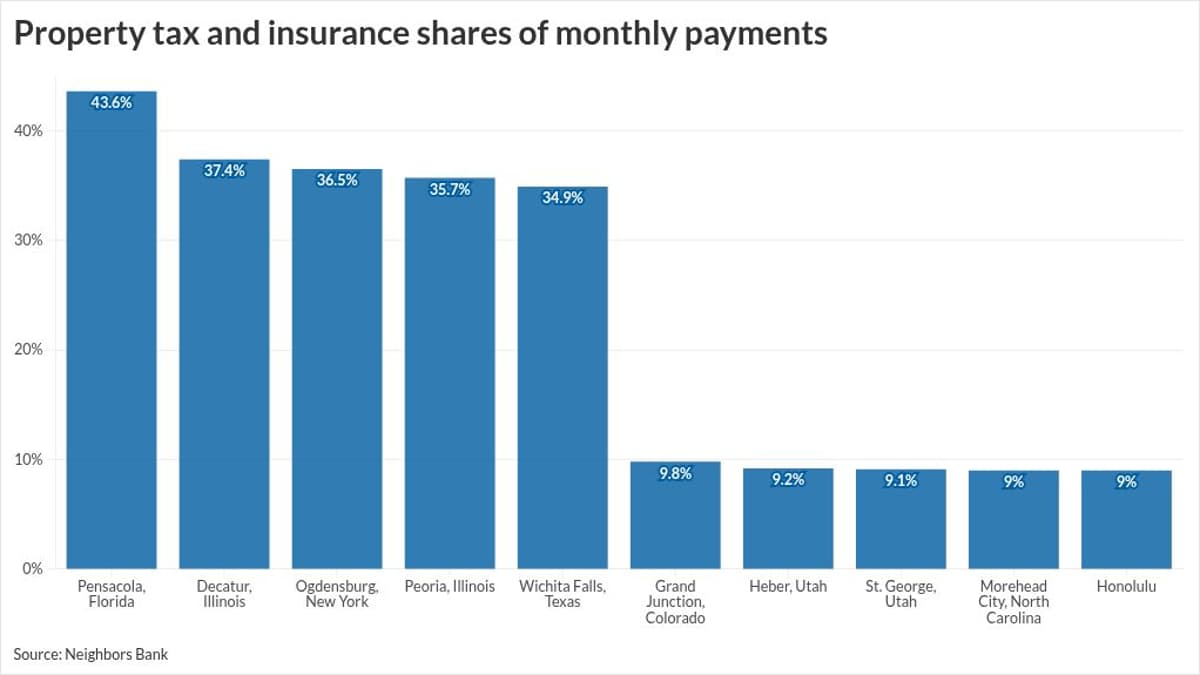

- •Florida and Illinois have highest tax/insurance burdens.

- •Honolulu shows low tax/insurance share despite high home prices.

Pulse Analysis

The rising share of taxes and insurance in monthly mortgage obligations signals a shift in the affordability equation that extends beyond headline‑grabbing home prices and interest rates. As local governments and insurers adjust to inflationary pressures, borrowers face variable escrow disbursements that can add hundreds of dollars to a fixed‑rate loan. This volatility disproportionately affects first‑time purchasers and borrowers in government‑backed programs, who often lack the financial literacy to anticipate fluctuating non‑mortgage costs. Lenders that fail to surface these expenses risk higher delinquency rates and reduced customer satisfaction.

Geography plays a decisive role in the tax‑insurance burden. In Florida, climate‑related insurance premiums surge, while Illinois’ property‑tax structure pushes the combined cost well above the national average. These high‑burden markets are prompting legislative action, from proposals to cap assessment growth to discussions about eliminating certain taxes altogether. Conversely, markets like Honolulu benefit from lower tax rates and newer, less risky housing stock, illustrating how local policy and risk exposure can dramatically alter the cost landscape. Investors and developers must factor these regional differentials into pricing models and risk assessments.

For prospective homeowners, proactive budgeting is essential. Understanding escrow mechanics, regularly reviewing tax assessments, and shopping for competitive insurance policies can mitigate surprise payment spikes. Mortgage lenders can add value by offering transparent cost breakdowns and educational tools that outline long‑term payment trajectories. As the housing market continues to grapple with inflationary pressures, integrating tax and insurance forecasts into affordability models will become a best practice for both borrowers and industry professionals.

Taxes, insurance eat 21% of mortgage payments

0

Comments

Want to join the conversation?

Loading comments...