Why ARMs Are Rising Even as Rates Drift Lower

•March 9, 2026

0

Why It Matters

The surge signals mounting housing‑affordability stress and could reshape mortgage product mix, influencing lenders, regulators, and home‑buyer strategies.

Key Takeaways

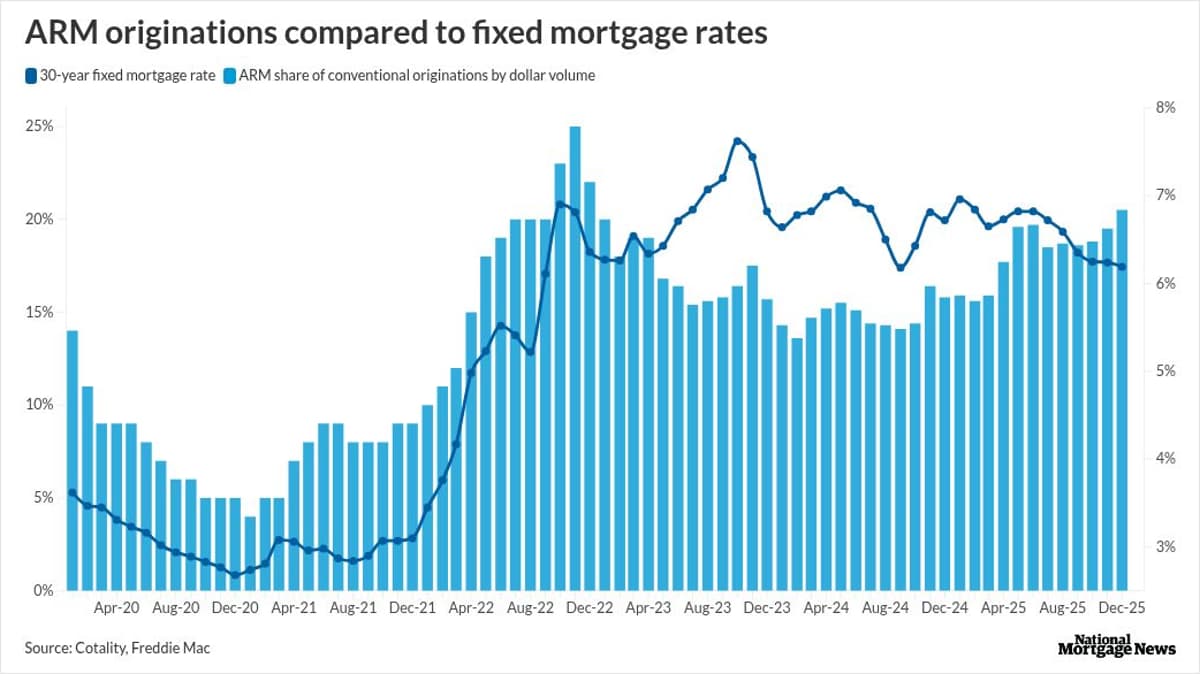

- •ARM share rose to 20.5% of conventional volume

- •5/1 ARM rate 80 bps below 30‑yr fixed

- •California ARMs exceed 31% of originations

- •Luxury loans $1M+ make up ~47% of ARM volume

- •Borrower regret reaches 70% for ARM choices

Pulse Analysis

The recent uptick in adjustable‑rate mortgages reflects a fundamental shift in how borrowers navigate an increasingly unaffordable housing market. As 30‑year fixed rates slipped below 6.5% but remained elevated relative to historic lows, many buyers in expensive metros turned to ARMs for their lower introductory rates. The 80‑basis‑point spread between the 5/1 ARM and the fixed benchmark translates into tangible monthly savings, making the product a pragmatic bridge for those unable to qualify for traditional financing. This dynamic is especially pronounced in California, the District of Columbia, and Massachusetts, where ARMs now account for roughly a third of all mortgage originations.

While the short‑term cash‑flow relief is appealing, it carries significant risk. Data from Point shows that nearly 70% of ARM borrowers later regret their choice, often because they underestimated payment increases after the fixed period expires. Moreover, a sizable share of ARM originations involve high‑end properties—nearly half of the volume ties to loans exceeding $1 million—indicating that even affluent borrowers are leveraging rate arbitrage to manage costs. The legacy of the 2022‑23 rate surge, when many adopted a "marry the house, date the rate" mindset, resurfaces as borrowers confront potential payment shocks amid a volatile macro environment.

Looking ahead, the trajectory of ARM demand hinges on the relative competitiveness of fixed‑rate mortgages. Should 30‑year rates decline further and regain price advantage, lenders may see a reversion to traditional loan mixes. Conversely, persistent inflationary pressures or geopolitical shocks could keep fixed rates elevated, cementing ARMs as a staple financing tool for price‑sensitive buyers. Policymakers and industry stakeholders must monitor borrower education and protection measures, as the growing reliance on variable‑rate products underscores broader affordability challenges within the U.S. housing sector.

Why ARMs are rising even as rates drift lower

0

Comments

Want to join the conversation?

Loading comments...