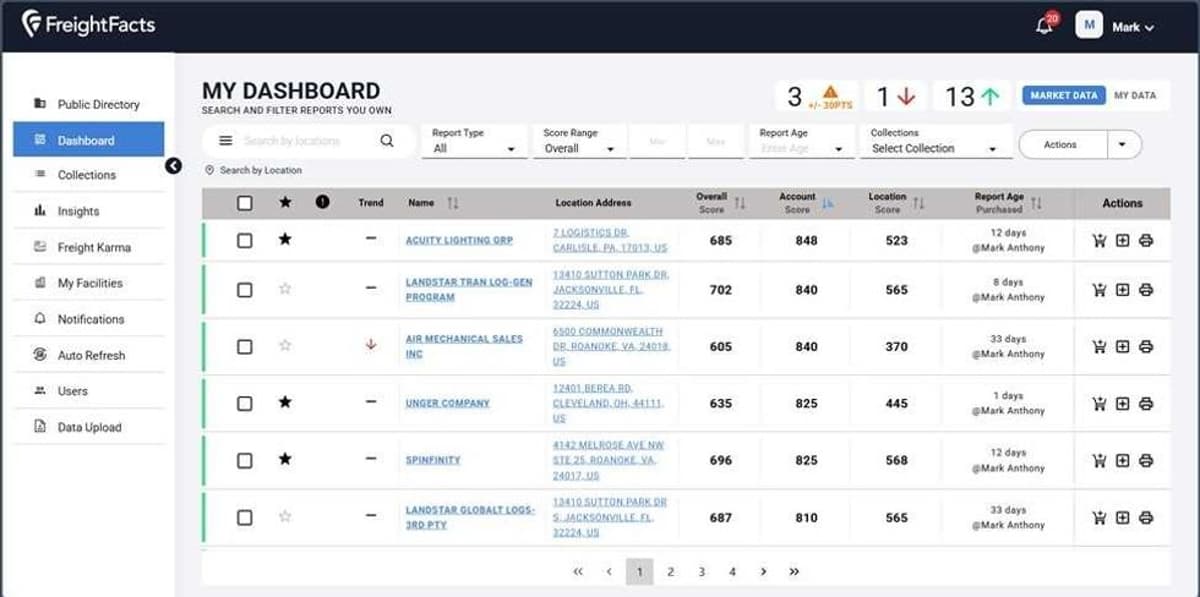

Startup Lets LTL Carriers Measure Shipper Performance

Companies Mentioned

Why It Matters

The convergence of regulatory driver reductions, persistent capacity glut, and heightened demand for tech‑enabled visibility reshapes profitability and competitive dynamics for LTL carriers and their shipper partners.

Key Takeaways

- •ODFL keeps 30% excess capacity, ready for market rebound

- •Driver oversupply persists; new regulations begin trimming independent operators

- •Shippers demand better tech, driving 3PL digital upgrades

- •Tiered sourcing hierarchies help mitigate tariff volatility

Pulse Analysis

The freight recession that began in 2023 shows few signs of abating, and LTL carriers are feeling the strain. Old Dominion Freight Line, the sector’s second‑largest player, has deliberately preserved roughly a third of its network as idle capacity while completing several new terminals. This strategic over‑building allows ODFL to quickly capture market share when spot rates climb, but it also ties up capital during a period of depressed demand. Analysts see this approach as a hedge against the inevitable cycle reversal, yet it underscores the delicate balance between readiness and cash‑flow pressure.

At the same time, the driver landscape is shifting. An estimated 580,000 owner‑operators once flooded the market, keeping capacity abundant and rates low. Recent DOT enforcement—tightening non‑domiciled driver licenses and mandating English proficiency—has begun to prune this oversupply, especially among single‑truck fleets. Industry observers predict a gradual capacity correction over the next two years, which could tighten the market and improve pricing for carriers that have survived the price war.

Shippers, however, are not waiting for the market to self‑correct. With tariffs fluctuating and supply‑chain disruptions commonplace, they are adopting tiered sourcing hierarchies to diversify risk and demand real‑time visibility. This pressure is accelerating investment in AI‑driven automation, ERP/WMS integrations, and cloud‑based platforms offered by 3PLs. Providers that can deliver seamless digital experiences will command premium rates, while those lagging in technology risk losing business back to in‑house logistics teams. The next wave of growth in LTL will likely be driven by carriers that combine operational flexibility with robust, customer‑focused tech solutions.

Startup lets LTL carriers measure shipper performance

Comments

Want to join the conversation?

Loading comments...