Why the $1.8 Trillion Global Space Economy Market Size Report Overstates the Space Market

Why It Matters

Inflated market numbers can mislead investors, distort policy priorities, and erode credibility in a rapidly maturing space sector.

Key Takeaways

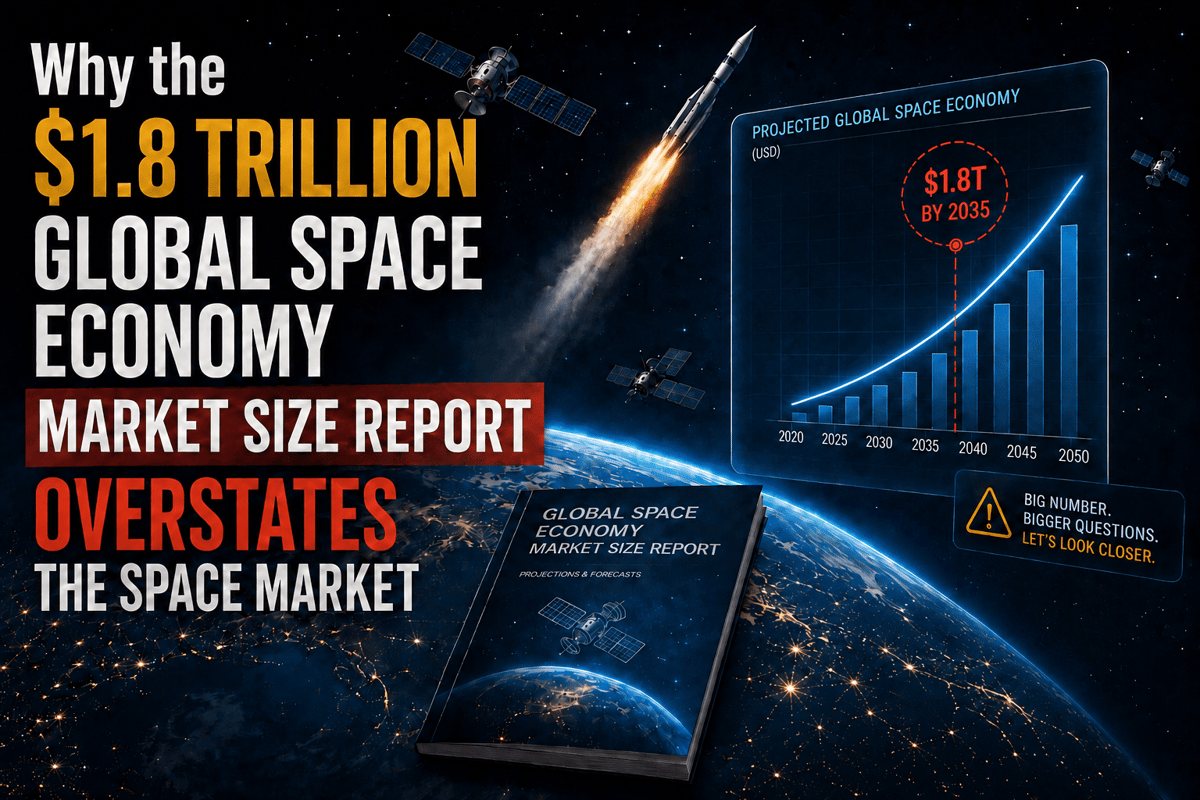

- •$1.8 trillion 2035 forecast mixes direct and reach revenues.

- •Direct space supplier revenue in 2024 was about $613 billion.

- •Reach applications contributed roughly $300 billion of 2023 total.

- •Inflated market size can distort investment and policy decisions.

- •Separate core, adjacent, and impact metrics for accurate reporting.

Pulse Analysis

The controversy surrounding the WEF‑McKinsey space‑economy estimate stems from how market boundaries are drawn. Traditional market sizing counts only the revenue earned by firms that sell rockets, satellites, ground stations, and related services. By adding "reach" revenues—such as ride‑hailing fees or agricultural sales that depend on satellite data—the report creates a composite figure that overstates the space sector’s direct economic footprint. This methodological choice blurs the line between supplier revenue and downstream value, making the headline number less useful for investors seeking addressable market size.

For capital markets and policymakers, the distinction matters. Venture capitalists evaluate satellite‑data analytics, launch services, or in‑space manufacturing based on the pool of direct customer spend, not the total revenue of every industry that benefits from those capabilities. The telecom analogy illustrates the risk: mobile‑network operators report service revenue, while the billions of dollars generated by e‑commerce or streaming platforms remain outside the telecom market. Similarly, semiconductor analysts separate chip sales from the value of the devices they power. Applying the same discipline to space would prevent double‑counting, improve comparability across regions, and provide clearer signals for funding and regulation.

A pragmatic solution is to adopt a three‑tier framework: (1) core space‑economy revenue covering launch, manufacturing, operations, and direct services; (2) adjacent space‑enabled revenue that quantifies downstream industry sales supported by space inputs; and (3) broader economic impact measuring productivity gains, risk mitigation, and public‑good benefits. Organizations such as the OECD and the U.S. Bureau of Economic Analysis already use supply‑use tables to separate output from value‑added, offering a template for standardizing space‑economy statistics. Clear labeling and transparent assumptions will allow investors to gauge true market opportunities while enabling governments to justify infrastructure spending based on genuine dependency metrics, ultimately fostering a more credible and sustainable space industry.

Why the $1.8 Trillion Global Space Economy Market Size Report Overstates the Space Market

Comments

Want to join the conversation?

Loading comments...