Cars to AI: How New Tech Drives Demand for Specialized Materials

•December 11, 2025

0

Why It Matters

AI’s reliance on scarce minerals could bottleneck a key growth engine and shift global power toward resource‑rich countries, affecting both industry and geopolitics.

Key Takeaways

- •AI models require rare earth minerals for hardware.

- •Cars spurred suburban expansion and material demand.

- •Specialized materials shift geopolitical power toward mineral-rich nations.

- •Mining industry growth follows tech adoption cycles.

- •Supply chain constraints risk AI deployment scalability.

Pulse Analysis

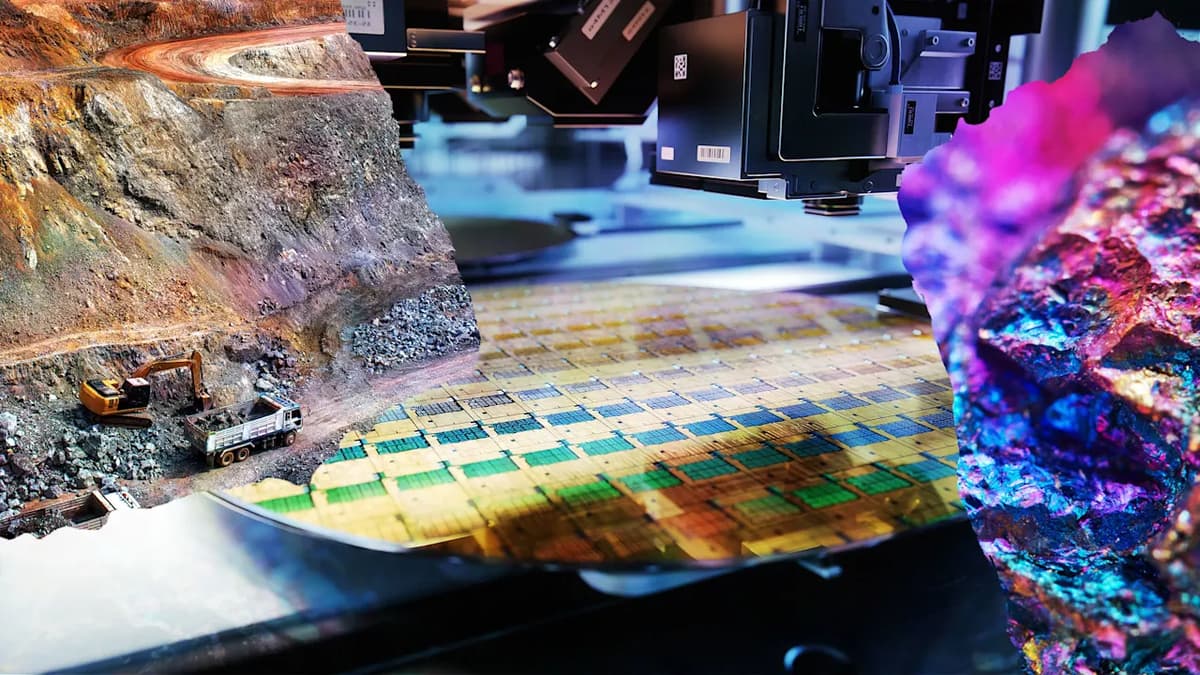

The rise of generative artificial intelligence is more than a software story; it is a materials story. Modern AI workloads depend on GPUs and specialized accelerators built from rare earth elements, cobalt, lithium, and other critical minerals. As data centers proliferate, the pressure on these supply chains intensifies, prompting manufacturers to secure long‑term contracts and explore alternative chemistries. Understanding the material underpinnings helps investors gauge where bottlenecks may emerge and which firms are positioned to mitigate risk.

History offers a clear template. When Henry Ford introduced the moving assembly line, automobile prices fell, enabling middle‑class families to own cars and prompting suburban sprawl. That lifestyle shift demanded new infrastructure—roads, highways, and housing—driven by steel, rubber, and later, petrochemical plastics. The smartphone era repeated the cycle, creating demand for glass, rare earth magnets, and advanced semiconductors. Each wave illustrates how a breakthrough technology reshapes consumption patterns, which in turn fuels a surge in specialized material production.

The geopolitical fallout is profound. Nations that control critical mineral deposits, such as the Democratic Republic of Congo for cobalt or China for rare earths, gain strategic leverage over technology supply chains. This dynamic spurs policy responses: diversification of mining sources, investment in recycling, and strategic stockpiling. Companies that integrate vertically or partner with responsible miners can reduce exposure, while regulators may impose standards to ensure supply chain resilience. For stakeholders, the intersection of AI, materials science, and geopolitics defines the next frontier of competitive advantage.

Cars to AI: How new tech drives demand for specialized materials

0

Comments

Want to join the conversation?

Loading comments...