ADAS Focus Shifts From Sensors to Software

Why It Matters

The shift redefines how value is created in automotive safety, forcing traditional hardware players to add software capabilities and reshaping supply chains across the industry.

Key Takeaways

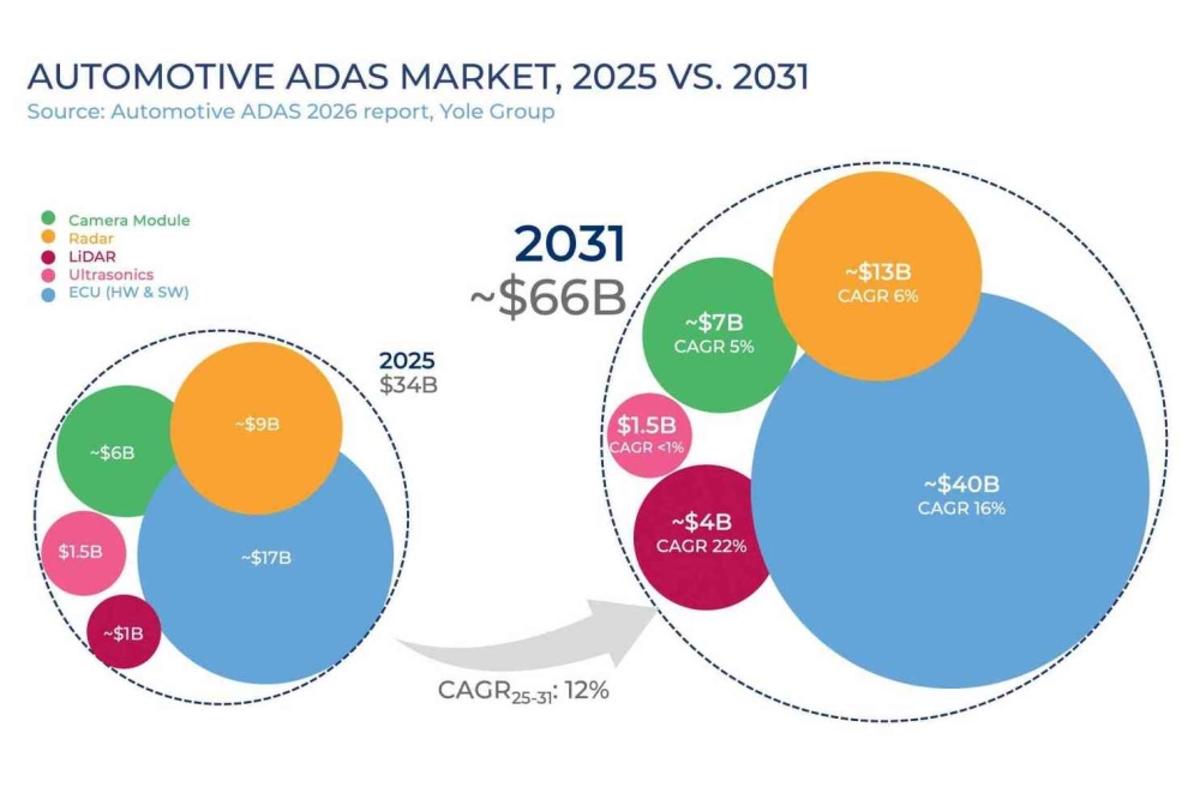

- •ADAS market to surpass $66 billion by 2031.

- •Growth now led by computing platforms and software, not sensors.

- •Centralized architectures replace distributed ECUs for scalability.

- •China becomes a distinct, fast‑adopting ADAS market.

- •Tier‑1s and semiconductors move up value chain with software.

Pulse Analysis

The latest Yole Group analysis highlights a fundamental transition in advanced driver assistance systems (ADAS) from a hardware‑first mindset to a software‑first architecture. While cameras, radar, and LiDAR remain essential sensors, the real competitive edge now lies in how these inputs are fused, processed, and acted upon by centralized computing platforms. This evolution mirrors broader automotive trends toward domain‑based architectures, where a single high‑performance processor handles multiple functions, delivering higher throughput, lower latency, and easier scalability for future autonomous features.

Supply‑chain implications are profound. Traditional Tier‑1 suppliers, long accustomed to delivering discrete electronic control units (ECUs) and sensor modules, are expanding their portfolios to include system integration, software development, and validation services. Semiconductor manufacturers are also moving up the value chain, forging tighter collaborations with OEMs to provide end‑to‑end platforms that bundle chips, firmware, and cloud connectivity. This convergence blurs the line between hardware and software vendors, accelerating the need for cross‑disciplinary talent and reshaping procurement strategies across the automotive ecosystem.

China’s rapid adoption adds another layer of urgency. The country’s vertically integrated ecosystem—combining domestic sensor makers, chip fabs, and software firms—has shortened innovation cycles for L2+ and emerging L3 capabilities. As Chinese OEMs roll out feature‑rich ADAS suites at scale, global players must contend with a market where software and compute dominate the value proposition. Looking ahead, the $66 billion market forecast underscores that firms able to deliver integrated, software‑centric ADAS platforms will capture the lion’s share of growth, while those clinging to pure sensor sales risk obsolescence.

ADAS focus shifts from sensors to software

Comments

Want to join the conversation?

Loading comments...