Waymo’s Shocking Data & Uber’s Infrastructure Pivot

•February 21, 2026

0

Why It Matters

The developments signal a tightening competitive moat for leaders like Waymo, force asset‑light players such as Uber to reconsider capital strategies, and highlight regulatory friction that could shape the rollout pace of autonomous mobility.

Key Takeaways

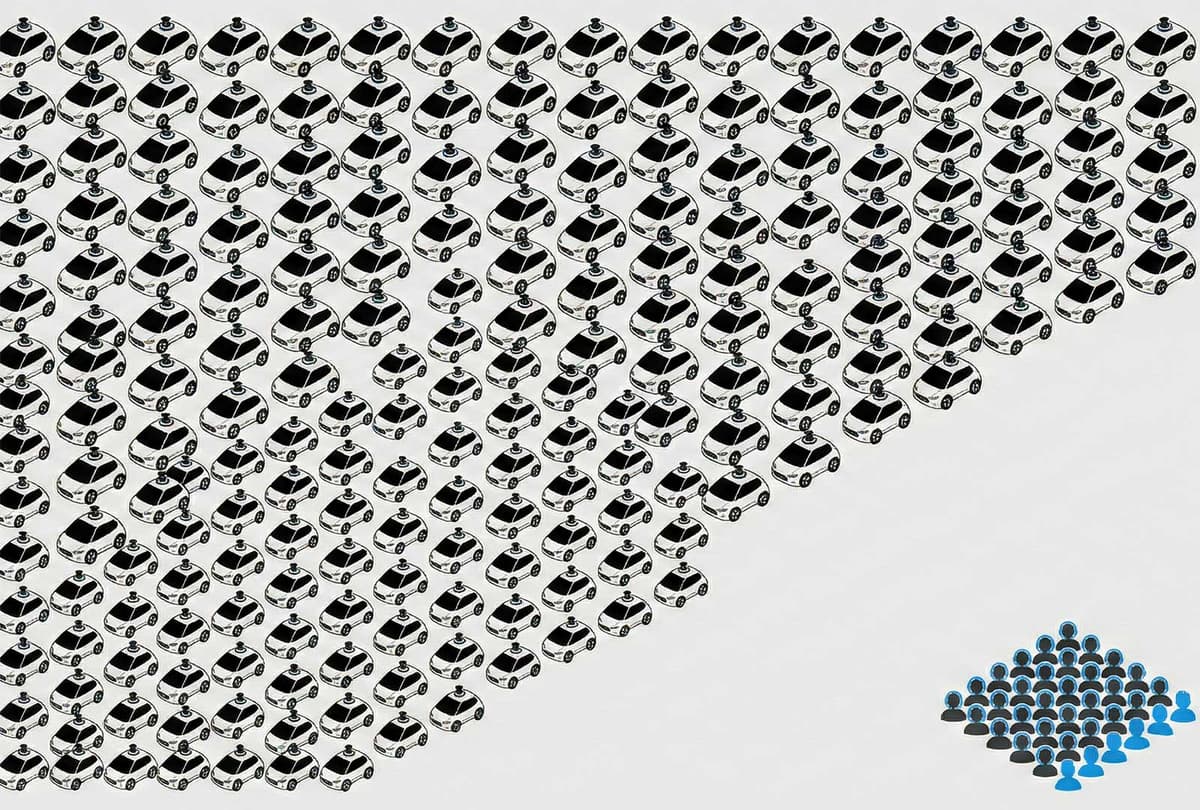

- •Waymo runs 3,000 cars with 70 remote agents

- •Half of Waymo agents outsourced to Philippines

- •Uber invests $100M in fast‑charging stations

- •NY governor stalls robotaxi expansion

- •Aurora opens 1,000‑mile autonomous trucking lane

Pulse Analysis

Waymo’s striking remote‑assistance ratio underscores how software and data processing efficiencies can dramatically reduce operational overhead. By centralizing supervision for thousands of vehicles, the company demonstrates a scalable model that rivals struggle to match. However, the reliance on outsourced staff in the Philippines introduces geopolitical risk, potentially exposing Waymo to regulatory scrutiny or labor disputes as the industry expands globally.

Uber’s $100 million commitment to autonomous‑vehicle charging infrastructure marks a notable pivot from its traditional asset‑light approach. Building proprietary fast‑charging stations in key markets not only secures energy access for its future robotaxi fleet but also creates a physical foothold that could deter competitors. This capital‑intensive move reflects broader industry pressure to own more of the value chain, especially as rivals like Waymo and Tesla tighten their technological advantages.

Regulatory dynamics remain a critical hurdle: New York’s decision to shelve a robotaxi proposal and Iowa’s driver‑in‑the‑car bills illustrate divergent state attitudes toward autonomy. Simultaneously, hardware progress continues, with Tesla’s FCC clearance for ultra‑wideband wireless charging and Aurora’s launch of a 1,000‑mile autonomous trucking corridor. These advances suggest momentum, yet the patchwork of local policies could fragment deployment timelines, making strategic partnerships and compliance expertise essential for sustained growth.

Waymo’s Shocking Data & Uber’s Infrastructure Pivot

0

Comments

Want to join the conversation?

Loading comments...