Waymo’s Shocking Data & Uber’s Infrastructure Pivot

•February 21, 2026

0

Why It Matters

Waymo’s low staffing ratio validates the scalability of autonomous tech, and Uber’s infrastructure spend signals a strategic shift that could reshape the competitive landscape of ride‑hailing and EV charging markets.

Key Takeaways

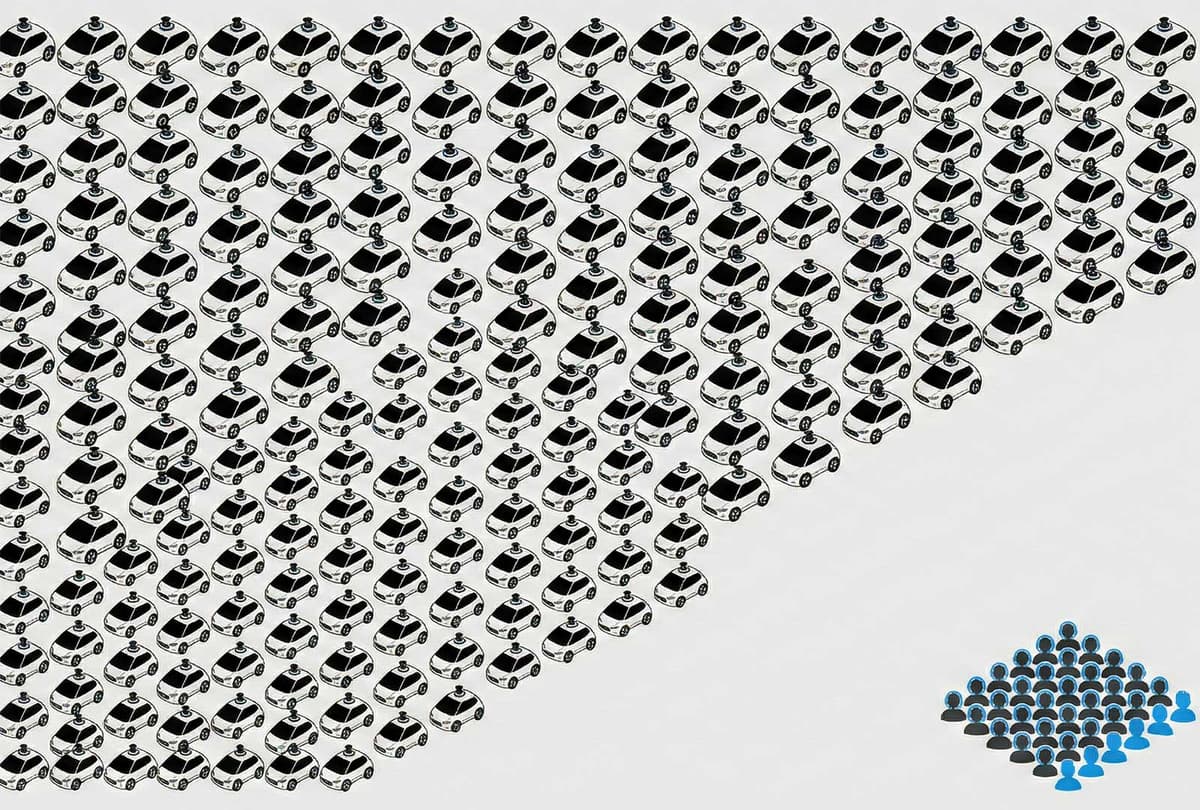

- •Waymo runs 3,000 cars with 70 remote agents

- •Half of Waymo's agents located in the Philippines

- •Uber spends $100M building EV charging stations

- •Uber's “take‑or‑pay” contracts may limit competitor access

- •Tesla receives FCC clearance for ultra‑wideband wireless charging

Pulse Analysis

Waymo’s revelation that a modest team of 70 remote assistance operators can oversee a 3,000‑vehicle robotaxi fleet underscores the maturity of its perception and control stack. By minimizing human intervention, Waymo not only reduces operating costs but also strengthens its case for broader regulatory approval. Industry observers see this ratio as a benchmark for emerging players, suggesting that the path to profitability may hinge more on software robustness than on labor‑intensive safety nets.

Uber’s $100 million plunge into proprietary EV charging infrastructure marks a notable departure from its publicly stated asset‑light philosophy. The investment, focused on fast‑charging hubs in key West Coast markets, could grant Uber preferential access to power and lock out rivals through “take‑or‑pay” contracts. Analysts argue that owning the energy supply chain may provide a competitive moat, yet it also raises capital‑intensity concerns and could alter the economics of its ride‑hailing platform.

Regulatory dynamics add another layer of complexity. New York’s reversal on a robotaxi proposal and Iowa’s driver‑in bills reflect a fragmented policy environment that autonomous operators must navigate. Simultaneously, Tesla’s FCC approval for ultra‑wideband wireless charging of the Cybercab showcases how ancillary technologies can accelerate adoption by easing the charging burden. Together, these developments illustrate a pivotal moment where operational efficiency, strategic asset allocation, and evolving regulations converge to shape the future of autonomous mobility.

Waymo’s Shocking Data & Uber’s Infrastructure Pivot

0

Comments

Want to join the conversation?

Loading comments...