Cooling’s New Reality: It’s Not Air Vs. Liquid Anymore. It’s Architecture.

•February 26, 2026

0

Companies Mentioned

Why It Matters

Cooling has become a primary constraint on AI‑scale data centers, influencing economics, geography, and time‑to‑market. Companies that master the integrated cooling stack will gain decisive competitive advantage.

Key Takeaways

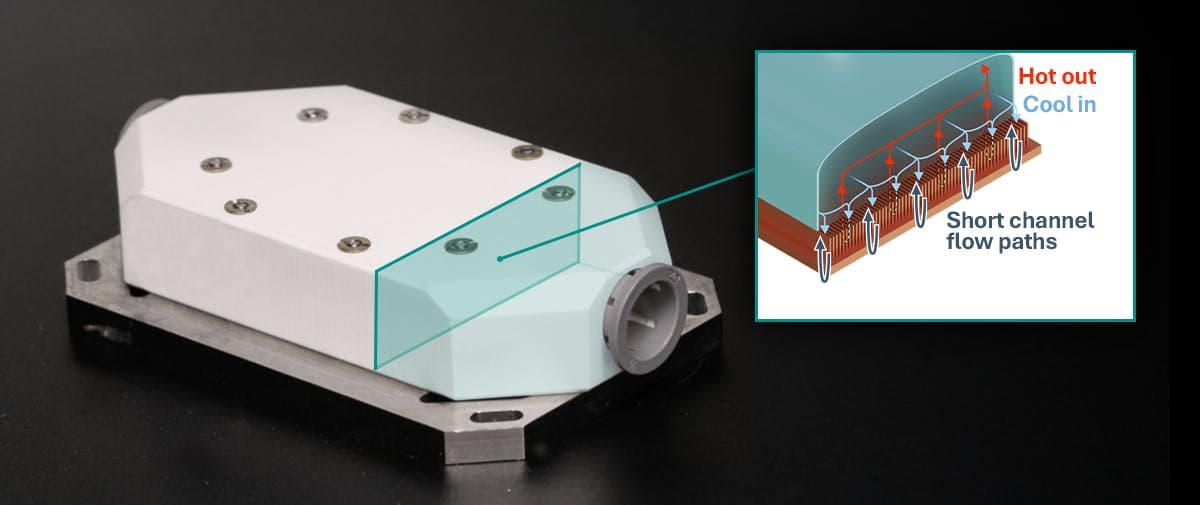

- •HRL Low‑Chill cuts pumping power tenfold

- •Johnson Controls acquires Alloy for liquid‑cooling IP

- •Carrier chiller recovers full capacity in under three minutes

- •Boyd doubles manufacturing footprint to meet AI demand

- •Immersion fluids target higher density than air or direct‑to‑chip

Pulse Analysis

The emerging cooling stack is reshaping data‑center architecture at every layer. At the chip level, HRL’s Low‑Chill leverages 3D‑printed manifolds to slash thermal resistance and enable hot‑loop operation, directly reducing the energy overhead of pumps. This shift not only supports next‑generation GPUs but also opens the door for dry‑air heat exchangers in water‑scarce regions, expanding viable site locations.

Beyond the rack, OEMs are treating thermal management as a strategic product line rather than a peripheral add‑on. Johnson Controls’ purchase of Alloy adds proprietary direct‑liquid cooling components that promise up to 35% efficiency gains, while Carrier and Modine reinforce the need for robust chillers capable of rapid recovery and extreme temperature tolerance. Their hybrid and resilient designs ensure uptime even when ambient conditions or power availability fluctuate, a critical factor for hyperscale operators seeking global consistency.

Supply‑chain scalability and fluid chemistry are the final pieces of the puzzle. Boyd’s facility expansion in Juárez illustrates the race to mass‑produce high‑capacity CDUs, cold plates, and manifolds at hyperscale speed. Simultaneously, chemistry firms like Arkema and PFX Group are elevating refrigerants and heat‑transfer fluids from commodities to performance differentiators, offering low‑GWP options that meet sustainability mandates. Together, these trends confirm that cooling is no longer a bolt‑on; it is a core determinant of AI‑driven data‑center viability.

Cooling’s New Reality: It’s Not Air vs. Liquid Anymore. It’s Architecture.

0

Comments

Want to join the conversation?

Loading comments...