Why It Matters

Lower feed costs can improve swine producers’ margins, influencing profitability and pricing decisions across the pork supply chain. The outlook also signals how commodity volatility may affect budgeting and risk‑management strategies.

Key Takeaways

- •Corn futures 2026 median $4.41 per bushel.

- •Feed-cost indices projected below 2025 levels.

- •Each $0.10 corn rise adds $0.43 cwt feed cost.

- •Swine finishing cost range $28‑$36 per cwt.

- •Soybean‑meal prices stay under long‑term average.

Pulse Analysis

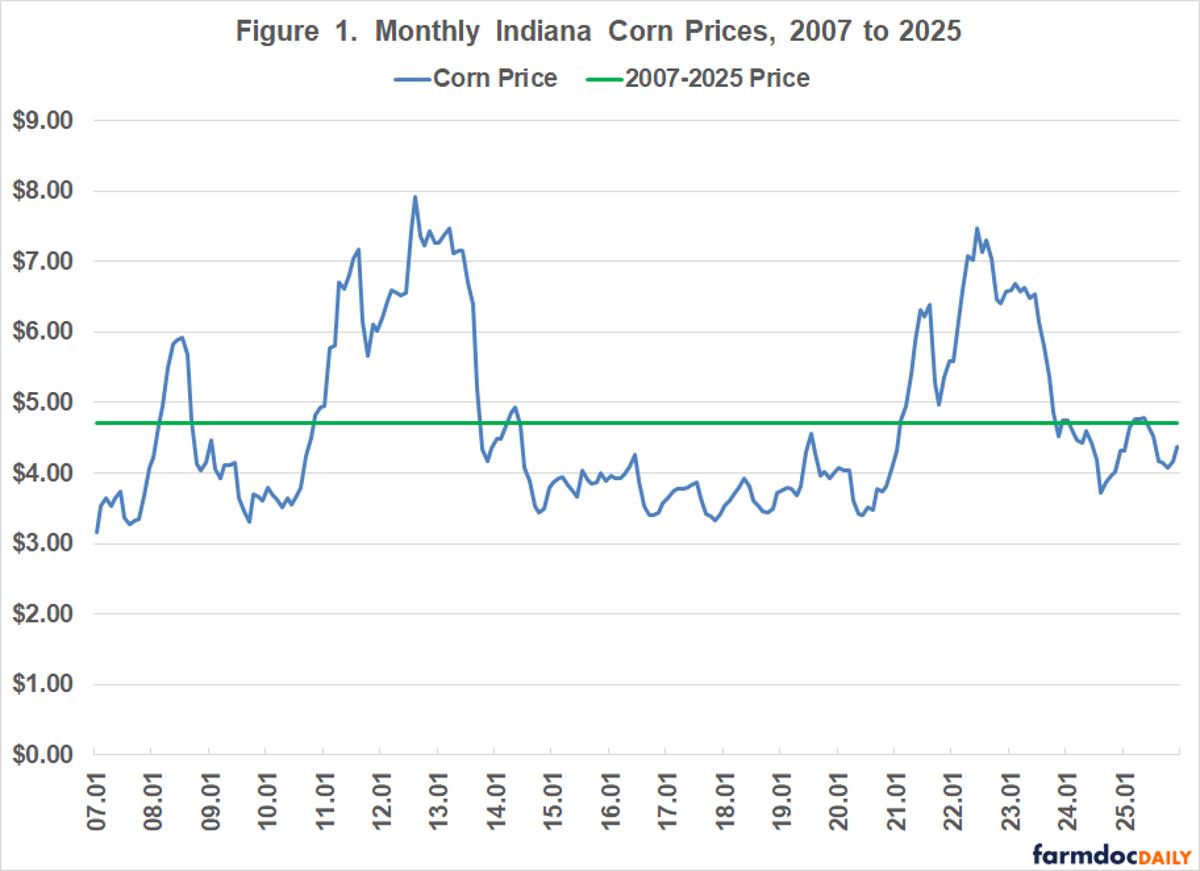

The corn market in the Midwest has entered a prolonged low‑price phase, with Indiana’s 2025 average at $4.45 per bushel and July 2026 futures distributed between $4.11 and $4.73. This environment reflects ample global supplies, favorable weather patterns, and muted demand from ethanol producers. Soybean‑meal, another key protein source, is also trading below its 2007‑2025 average, hovering around $312 per ton. Together, these commodity trends set the stage for a more affordable feed bill for pork operations.

Feed‑cost indices, the industry’s barometer for ingredient expense, illustrate the direct impact of these price dynamics. The farrow‑to‑finish index is projected at 98.8 for 2026, while the swine‑finishing index sits near 99.3, both modestly under the 2025 baseline of 100. Sensitivity analysis underscores that a modest $0.10 shift in corn price translates to a $0.43 per cwt change in total feed cost, and a $10 move in soybean‑meal alters costs by $0.37 per cwt. Depending on the exact corn‑soybean‑meal mix, producers could see feed costs ranging from $28 to $36 per cwt.

For pork producers, these cost signals are critical for budgeting, contract negotiations, and risk‑hedging strategies. Lower feed expenses improve gross margins and can enable competitive pricing in downstream markets. However, the outlook remains contingent on weather anomalies, global demand fluctuations, and policy shifts affecting biofuel mandates. Producers are advised to monitor futures curves closely and consider forward contracts or options to lock in favorable prices, ensuring resilience against potential commodity rebounds.

Prospects for Swine Feed Costs in 2026

0

Comments

Want to join the conversation?

Loading comments...