U.S. and Brazil Soybean Competitiveness: Farm-Level Costs and Returns

•February 23, 2026

0

Why It Matters

The cost‑structure gap threatens U.S. market share and farm profitability, prompting a need for productivity gains and cost‑management strategies. It also reshapes global soybean trade dynamics as Brazil consolidates its export lead.

Key Takeaways

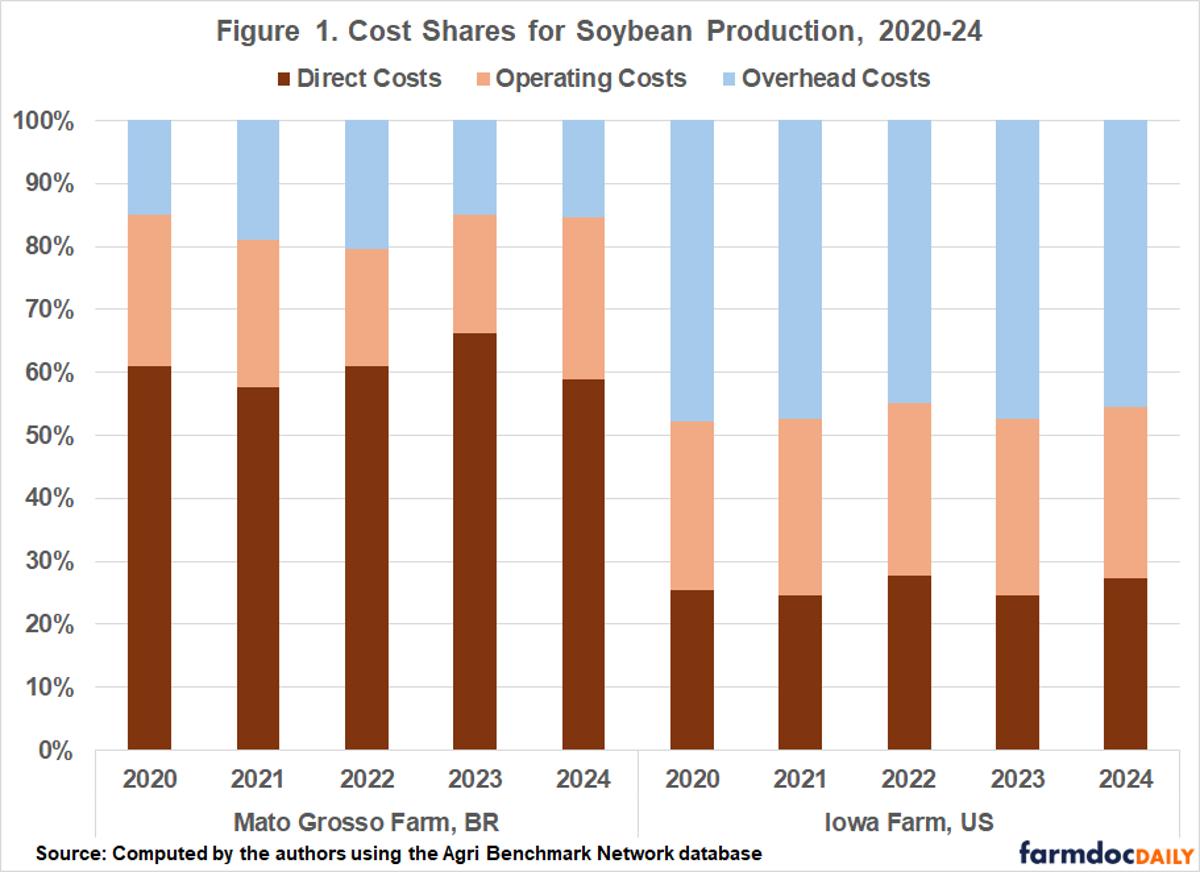

- •Brazil’s input costs exceed 60% of total soybean expenses.

- •U.S. overhead costs dominate, driven by rising land values.

- •Brazilian soybean profits stayed positive despite cost spikes.

- •U.S. farms faced profit volatility and occasional losses 2020‑24.

- •Future U.S. competitiveness hinges on productivity and cost control.

Pulse Analysis

Brazil’s ascent in the global soybean market is rooted in a cost structure that, while heavily weighted toward direct inputs, benefits from a depreciating real and robust demand from China. Imported fertilizers, which represent a large share of Brazilian expenses, surged after the Russia‑Ukraine conflict, pushing per‑ton costs from $172 to $337. Yet strong international prices and favorable exchange‑rate dynamics kept Brazilian farm profits positive, underscoring the country’s ability to absorb input shocks and maintain export momentum.

In the United States, the opposite dynamic prevails. Overhead costs—particularly land values—now consume nearly half of total soybean production expenses, driven by limited cropland supply, investor demand, and high corn‑soybean profitability. Operating costs rose 14% between 2020 and 2024 as labor, diesel, and machinery prices climbed amid pandemic‑induced supply‑chain strains and inflation. These pressures eroded margins, producing volatile profitability and losses in 2020 and 2024 despite occasional price spikes that briefly lifted revenues.

The divergent trajectories signal a strategic crossroads for U.S. producers. To preserve competitiveness, American farms must accelerate productivity through precision agriculture, adopt lower‑cost input alternatives, and manage land‑value exposure via leasing or diversified cropping. Policy support for domestic fertilizer production and trade‑friendly agreements could also mitigate cost volatility. As Brazil expands into frontier regions and upgrades logistics, the U.S. will need a coordinated mix of technology, risk‑management tools, and cost‑control measures to retain its share of the global soybean market.

U.S. and Brazil Soybean Competitiveness: Farm-Level Costs and Returns

0

Comments

Want to join the conversation?

Loading comments...