US Grain Storage Capacity Growth Has Stopped

Key Takeaways

- •Storage capacity growth halted since 2020 despite rising production

- •2025 on‑farm utilization reached 80%, near historic highs

- •Surplus capacity shrank to 5% of total, down from 15%

- •Off‑farm storage growth lagged, shifting burden to farmers

- •Investment uncertainty driven by construction costs and low returns

Pulse Analysis

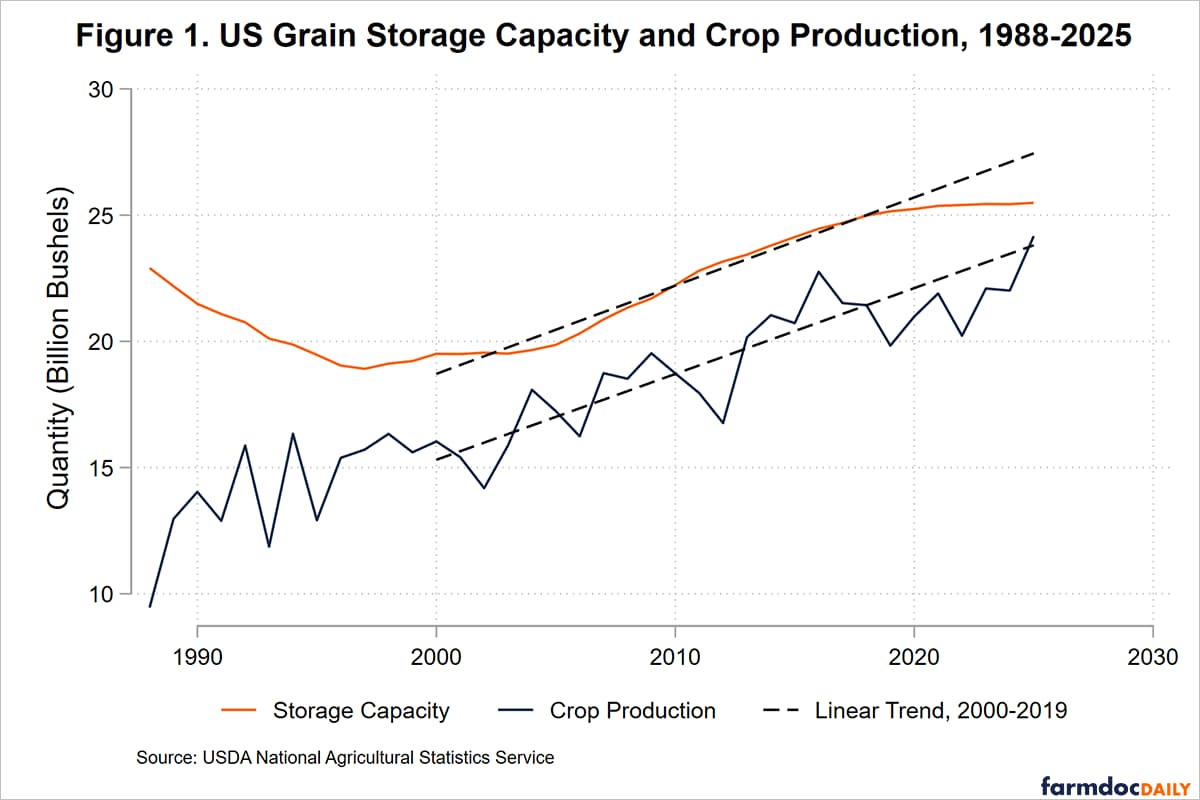

Grain storage is the linchpin of the United States’ agricultural logistics, allowing producers to capture optimal market prices and smoothing seasonal supply fluctuations. From 2000 to 2019, capacity kept pace with production, expanding by an average of 349 million bushels annually. That alignment vanished after 2020, leaving the nation with roughly 25 billion bushels of storage while crop output continued to climb, especially in corn. The resulting squeeze has pushed overall surplus capacity to a five‑year low, setting the stage for systemic stress.

The most visible symptom of this strain is the surge in on‑farm storage utilization. By the end of the 2025 harvest, farmers were using 80 % of their on‑farm bins, compared with 65 % off‑farm, reversing a decades‑long trend where intermediaries handled the bulk of post‑harvest storage. Regional analysis shows the Western Corn Belt and Northern Great Plains relying heavily on on‑farm facilities, increasing exposure to local bottlenecks and transport constraints such as low Mississippi River water levels. Higher utilization amplifies basis differentials, potentially inflating farm‑gate prices while compressing margins for downstream processors.

Looking ahead, the storage gap hinges on capital allocation decisions. Rising construction costs, higher interest rates, and uncertain revenue streams make new silos a risky proposition, especially when returns are modest under normal market conditions but spike only during shocks. Stakeholders may need to explore public‑private partnerships, tax incentives, or innovative financing models to revive capacity growth. Meanwhile, short‑term mitigations—such as temporary bagging, ground piles, or improved inventory rotation—can alleviate pressure, but a sustainable solution will require coordinated investment to keep the U.S. grain supply chain resilient and competitive.

US Grain Storage Capacity Growth Has Stopped

Comments

Want to join the conversation?