Analysts Warn of Largest Oil Supply Disruption in History

•March 3, 2026

0

Why It Matters

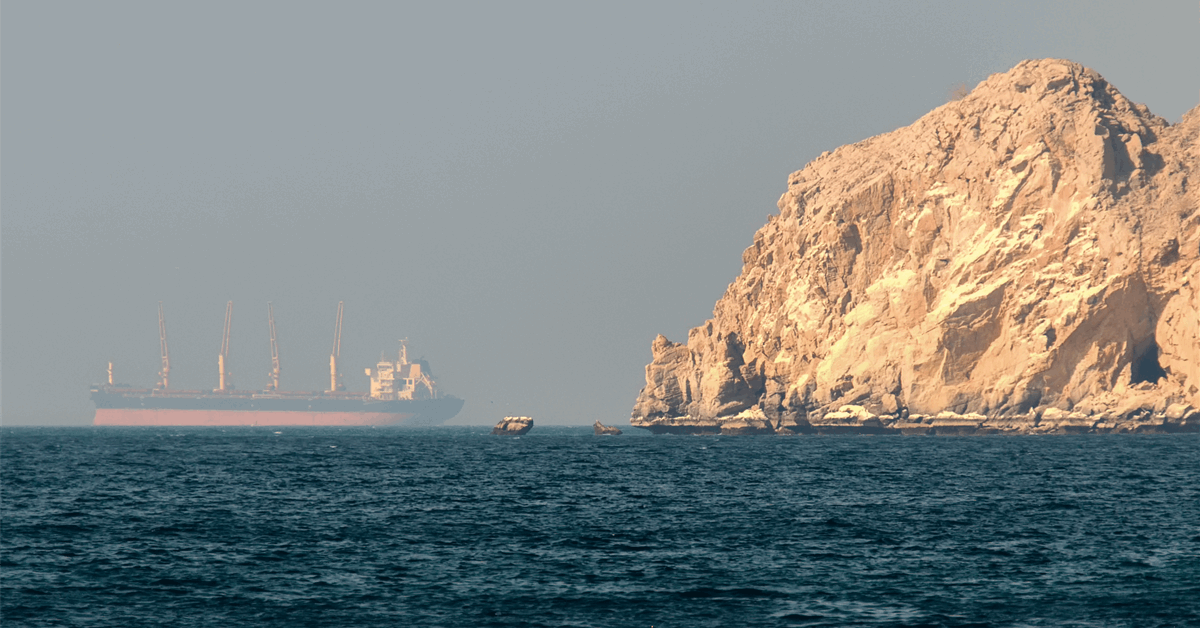

The Strait of Hormuz carries roughly 20% of global oil flow; any prolonged shutdown would spike prices, strain financial markets, and reshape the global energy balance.

Key Takeaways

- •Tanker transits fell from 60 to five daily.

- •Up to 15 million barrels per day at risk.

- •Low‑case Brent forecast $75‑$90; high‑case $110‑$130.

- •Prolonged Hormuz closure could turn surplus into deficit.

- •Market impact hinges on conflict duration and infrastructure damage.

Pulse Analysis

The Strait of Hormuz remains a chokepoint for world energy, funneling about 20 percent of daily crude and a similar share of LNG. A sudden drop to five tankers on March 1—down from a typical sixty—signals a rapid escalation in geopolitical risk. When the narrow waterway is compromised, shippers must reroute around Africa’s Cape of Good Hope, adding weeks and billions in costs, while regional producers scramble to use alternative pipelines that may lack capacity.

S&P Global and Fitch’s BMI teams have modeled three risk pathways. In the low‑case, a brief flare‑up limits price spikes to $75‑$90 per barrel, but a mid‑case with partial Hormuz disruption pushes Brent into the $90‑$110 range. The high‑case, featuring sustained attacks and extensive infrastructure damage, could see prices breach $130, erasing any surplus and forcing rationing. Such moves would reverberate through commodity markets, sovereign wealth funds, and corporate balance sheets, amplifying volatility and reshaping hedging strategies.

Policymakers and investors must monitor both the duration of hostilities and the resilience of Gulf export infrastructure. A swift diplomatic de‑escalation could restore transit within weeks, allowing the market to revert to its pre‑conflict oversupplied outlook for 2026. Conversely, a protracted conflict would accelerate a shift from surplus to deficit, prompting central banks to reassess inflation forecasts and energy‑focused funds to recalibrate exposure. Understanding these dynamics is essential for navigating the next wave of oil‑price uncertainty.

Analysts Warn of Largest Oil Supply Disruption in History

0

Comments

Want to join the conversation?

Loading comments...