Why It Matters

The CPI reading steers monetary‑policy expectations, while the grain market shifts signal supply‑side pressures that could reshape global food prices and trade flows.

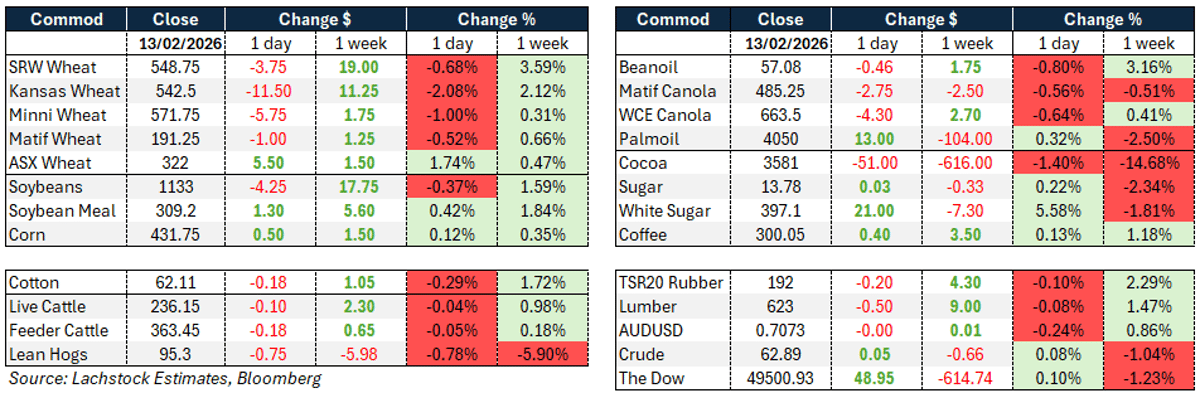

Key Takeaways

- •US CPI 2.4% y/y, easing inflation pressures

- •Wheat futures slide as spreads invert, supply ample

- •China rain damages stored corn, raises import risk

- •Australian rain forecast 20‑30mm, market liquidity thin

- •Canola bids hold, export interest resurges

Pulse Analysis

The latest US consumer‑price data showed a modest 0.2% month‑over‑month rise, pulling annual inflation to 2.4% and keeping core CPI in line with forecasts. Analysts interpret the softening headline as evidence that the disinflation process remains on track, reinforcing market bets on additional Federal Reserve easing later in the year. With rate‑cut pricing now around 67 basis points by early 2027, the dollar slipped modestly, nudging the AUD to 0.7073 and influencing commodity‑linked currencies.

Across the grain spectrum, wheat futures fell sharply as an unprecedented surge in spread trading inverted the curve, a structural event not driven by a clear supply shock. Record open interest and a sudden contraction in carry forced systematic participants to unwind positions, leaving the market vulnerable to any unexpected supply changes. Meanwhile, the IKAR forecast lift for Russian wheat to 91 mt and limited Indian export allocations have reinforced the perception of ample Black Sea supply, pressuring prices despite lingering weather uncertainties in the U.S. Plains and Europe.

The broader agricultural outlook is colored by weather extremes. Excessive rainfall in China has reportedly caused mold in stored corn, sparking concerns over quality and the potential for heightened import demand as domestic prices rise. In Australia, growers are eyeing a modest 20‑30 mm rain event, a critical moisture boost as liquidity remains thin in the northern markets. Canola enjoys a supportive bid environment, buoyed by export interest and a resilient veg‑oil market, while the Canadian dollar’s recent weakness adds a modest tailwind for commodity exporters. Together, these dynamics underscore a volatile but opportunity‑rich period for traders and food‑industry stakeholders.

Daily Market Wire 16 February 2026

0

Comments

Want to join the conversation?

Loading comments...