The U.S. Farm Machinery & Equipment Market: Sales, Inventories, and Tariff Headwinds

•February 27, 2026

0

Why It Matters

The contraction threatens revenue and profitability for the industry’s three largest OEMs and limits farmers’ access to affordable equipment, influencing overall agricultural productivity.

Key Takeaways

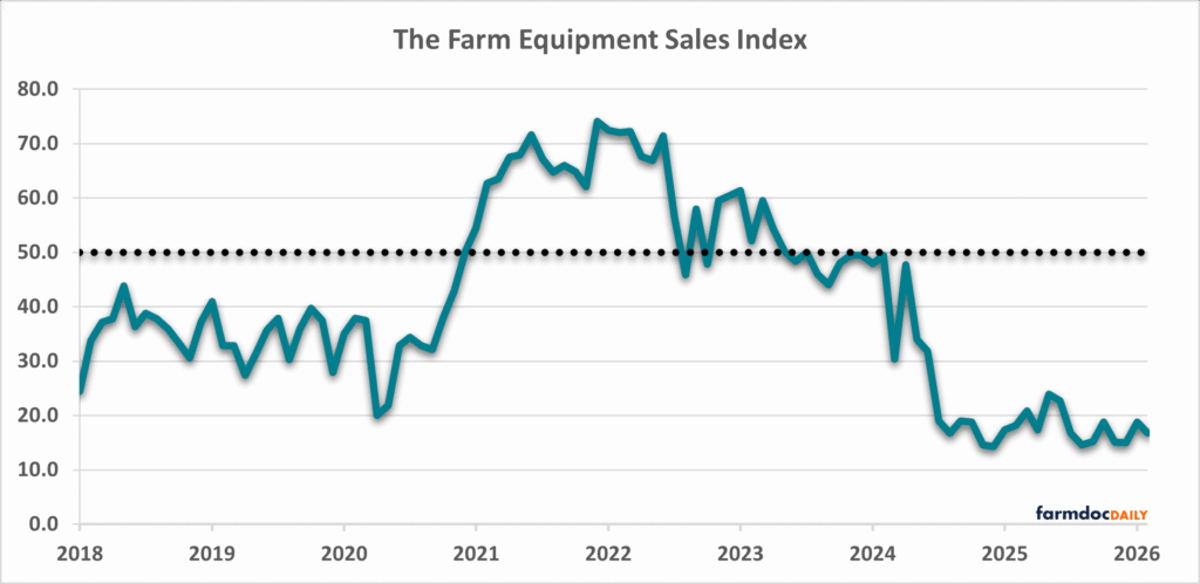

- •Tractor sales down 9.9% in 2025

- •Combine sales down 35.6% in 2025

- •Inventories fell 20.8% since 2022 peak

- •Tariff costs hit Deere $600 M, CNH EBIT halved

- •Supreme Court may refund duties, but new tariffs loom

Pulse Analysis

The 2025 sales slump reflects a broader shift in farm economics. Lower grain prices, squeezed farm incomes, and higher borrowing costs have curbed farmer spending, driving a 30‑month stretch of sub‑neutral readings on the Creighton Rural Mainstreet Index, which dropped to 16.7 in February. Tractor volumes contracted for the fifth consecutive year, while combine sales, once a growth story, now register double‑digit declines, signaling that even high‑value equipment is vulnerable to credit constraints.

Manufacturers have responded by trimming production to align with the weakened demand. Total farm machinery inventories fell from a $7.23 billion peak in late 2022 to $5.72 billion by the end of 2025, a 20.8% reduction. Yet, used‑tractor inventories and asking prices continue to slide, indicating persistent oversupply in the secondary market, whereas used‑combine inventories show modest rebounds. Despite these pressures, the USDA’s machinery price index remains above pre‑COVID‑19 levels, underscoring that input cost inflation and supply‑chain bottlenecks still influence pricing dynamics.

The tariff episode adds a volatile policy layer. In 2025, emergency tariffs imposed under the IEEPA forced Deere to absorb roughly $600 million in duties, with CNH’s ag‑segment EBIT dropping from $1.47 billion to $772 million. A February 2026 Supreme Court ruling that struck down those tariffs offers potential relief, but the administration’s pivot to a new 10‑15% tariff under Section 122 re‑introduces uncertainty. Stakeholders will watch closely for legislative or judicial outcomes, as any sustained tariff relief could restore margins and stimulate a gradual market recovery, provided grain prices and credit conditions also improve.

The U.S. Farm Machinery & Equipment Market: Sales, Inventories, and Tariff Headwinds

0

Comments

Want to join the conversation?

Loading comments...