Residential Building Worker Wages Remain Soft in Early 2026 Amid Slower Housing Activity

Why It Matters

The deceleration in wage growth signals a cooling residential construction market, which could pressure profit margins for builders and affect labor supply dynamics. For workers, stagnant real pay raises concerns about purchasing power amid persistent inflation.

Key Takeaways

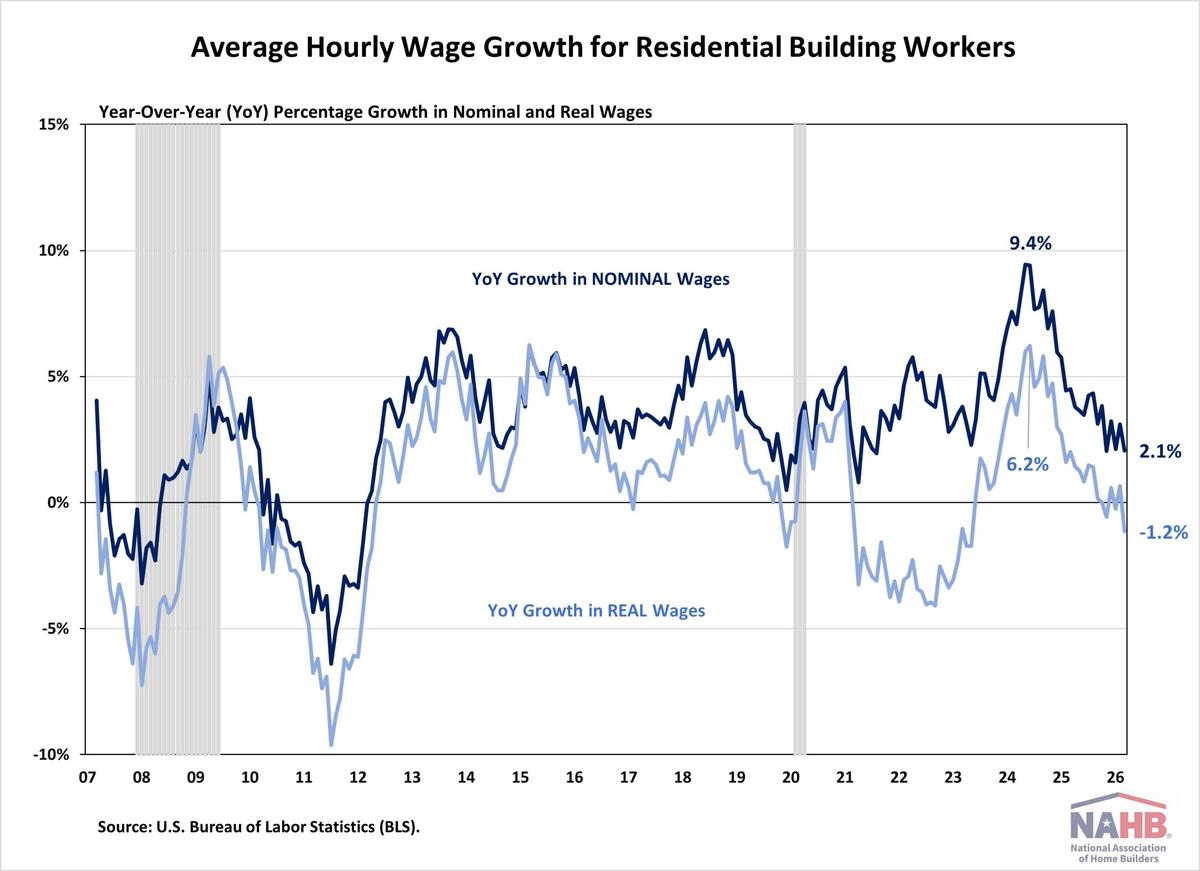

- •Nominal wages rose 2.1% YoY in March 2026.

- •Real wages fell 1.2% YoY, lagging inflation.

- •Open construction jobs keep declining, indicating weaker demand.

- •Residential wages still 8.4% higher than manufacturing.

- •Wage growth slowed after 2024 peak, reflecting softer housing market.

Pulse Analysis

The residential construction labor market entered a new phase in early 2026, moving away from the rapid post‑pandemic expansion that drove double‑digit wage gains in 2023‑2024. As home‑building permits slipped and remodel activity softened, employers faced less urgency to compete for talent, allowing nominal earnings to plateau at a modest 2.1% increase. This trend aligns with broader macroeconomic signals, including tighter credit conditions and a slowdown in mortgage rates, which together dampen new‑home starts and remodel budgets.

For workers, the headline numbers mask a more nuanced reality. While nominal pay remains above many other sectors—8.4% higher than manufacturing and 22.4% above transportation—real wages have slipped 1.2% after accounting for inflation. The erosion of purchasing power is especially concerning given that housing costs, a major expense for construction workers, continue to rise in many regions. The wage differential also highlights occupational bargaining power; however, the declining pool of unfilled construction jobs suggests that the sector may soon face a surplus of labor, potentially reversing the premium.

Looking ahead, the trajectory of residential wages will hinge on housing demand, policy interventions, and broader economic health. If mortgage rates stabilize and consumer confidence rebounds, a modest uptick in construction activity could reignite wage growth. Conversely, prolonged high interest rates or supply‑chain constraints could keep labor demand muted, pressuring real earnings further. Stakeholders—from builders to policymakers—should monitor job‑opening trends and regional price dynamics to gauge whether the current softness is a temporary adjustment or the start of a longer‑term recalibration in the residential construction labor market.

Residential Building Worker Wages Remain Soft in Early 2026 Amid Slower Housing Activity

Comments

Want to join the conversation?

Loading comments...