Alex Johnson

Creator

1 followers

Creator of Fintech Takes; writes sharp analysis on consumer finance, lending/credit, and digital banking strategy.

Recent Posts

Social•Feb 9, 2026

First‑party Fraud Needs Memory, Not More Blocks

First-party fraud passes every check. The data lines up; the customer's real. The problem is intent, and intent is difficult to quantify. First-party fraud is hard to detect because it's hard to define. A PSP sees risk. A merchant sees a refund. A network sees noise. So how do you share signals without forcing everyone to agree? In a recent episode of Not Fintech Investment Advice on the @FintechTakes podcast, @sytaylor and I talk about what makes first-party fraud more of a qualitative problem, and why blocking more transactions isn't always the fix. It’s all about building memory, which is what @trudenty's working on. Watch the clip, then tune in to hear more about the fintech startups Simon and I are absolutely not giving investment advice on: https://t.co/91WaPOsunX (Also featuring Tidalwave, @kaaj_ai, & FinReach Solutions)

By Alex Johnson

Social•Feb 2, 2026

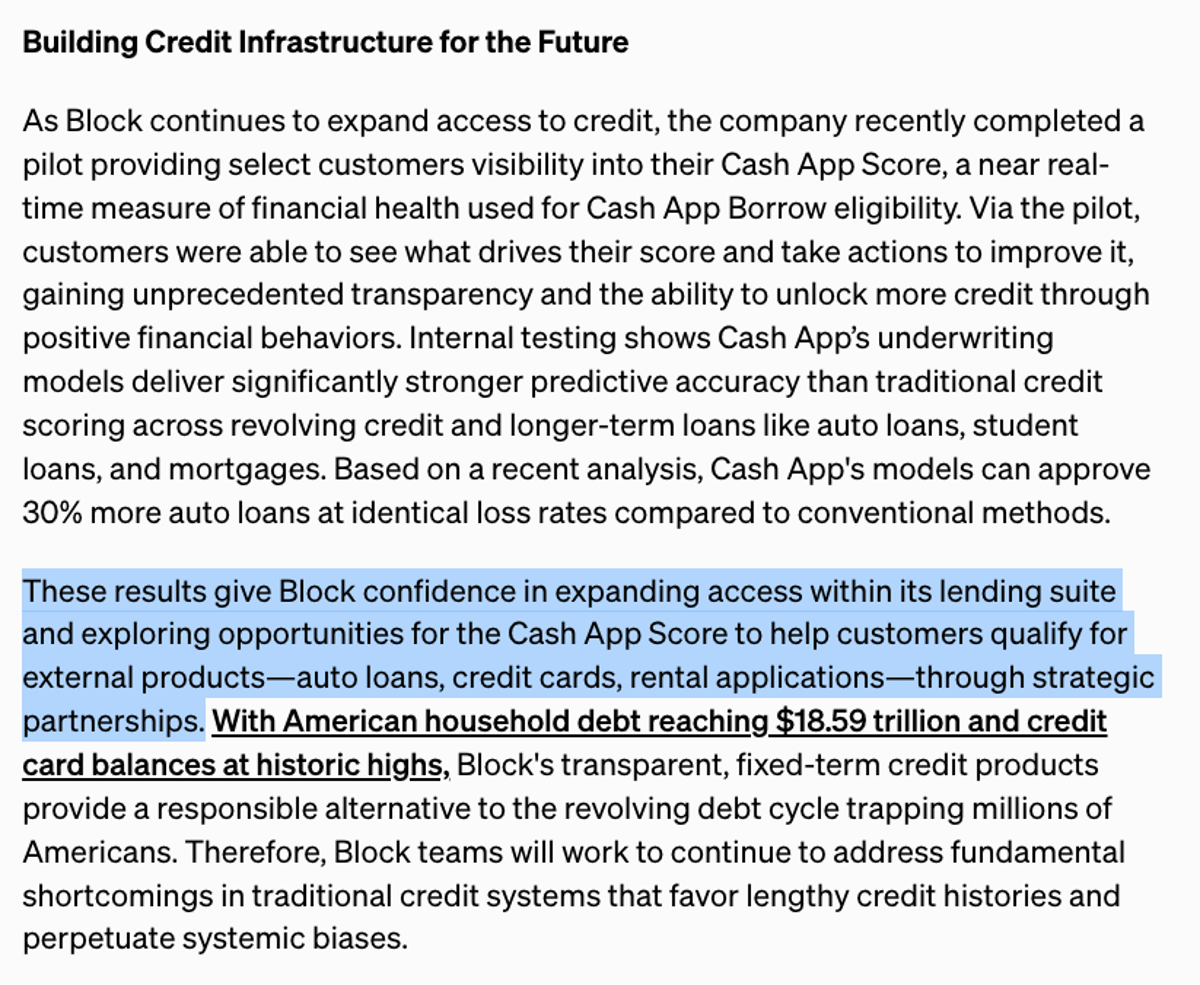

Block Eyes Cash App Score for External Lending Partnerships

Block has said that it's going to explore leveraging its Cash App Score (i.e., its internal underwriting model) to help customers qualify for products and services from external providers (auto lenders, credit card issuers, landlords, etc.) I have so many questions...

By Alex Johnson

Social•Feb 2, 2026

Early Decisions Shape Scalable Culture Beyond the Founder

Culture is what persists after the founder leaves the room. In this clip, @mlevchin explains how early decisions calcify into a company's DNA. Those decisions get embedded early. They compound and (eventually) self-enforce. Once a company scales, culture is no longer a...

By Alex Johnson

Social•Jan 30, 2026

Coinbase Seeks Bank Perks, Dodges Regulatory Duties

It's funny because the old response from Armstrong would have been, "regulators would never let us become a bank." Obviously, that's not true right now, which suggests that Coinbase wants privileges of being a bank without the obligations of being one.

By Alex Johnson

Social•Jan 27, 2026

Customers Stay with Banks; Stablecoins Won’t Shift Deposits

I very much agree with this sentiment. There’s nothing stopping Chase and BofA customers from moving to get higher rates today. They choose not to. Yield-bearing stablecoins won’t fundamentally change that dynamic. (This also means that Coinbase will likely be less successful...

By Alex Johnson

Social•Jan 26, 2026

Kontigo's Neobank Facade Leaves No Clear Accountability

Kontigo looks and acts like a neobank, but there’s no bank standing behind it. At least with BaaS middleware, the end user had a legal and contractual relationship with a bank. So, there's a clear line of responsibility (whether the issue was...

By Alex Johnson

Social•Jan 23, 2026

Fintech Infrastructure Battle Benefits Nerds, Hurts EWS/FIS

This is the best case scenario for nerds like me who are interested in obscure fintech infrastructure and data-sharing consortiums. And it's the worst case scenario for EWS and/or FIS. Getting dragged into this fight is the last thing they want.

By Alex Johnson

Social•Jan 22, 2026

The Term “Seed Round” Is Officially Retired

We are now officially retiring the term "seed round". Thank you for your attention to this matter. https://t.co/NzL2sy9dUJ

By Alex Johnson

Social•Jan 22, 2026

Treat Generative AI as Intelligence, Not Deterministic Software

We often talk about LLMs as another tool to tack onto a workflow, but that framing isn't quite right. In this clip, Naeem Abraham (Senior Director of Product Strategy at C&R) presents a ... better perspective. Generative AI doesn't behave like a...

By Alex Johnson

Social•Jan 19, 2026

Remote Work May Demote Auto Loans in Repayment Hierarchy

Dave Wasik and I revisit a Great Recession line about auto loans and consumers' repayment hierarchies: “you can sleep in your car, but you can’t drive your house to work.” Then we ask the 2026 question: with work-from-home and Uber/Lyft now...

By Alex Johnson

Social•Jan 17, 2026

Split Banking Lobby to Counter Anti‑Yield Crypto Divide

It would be smart strategy to try to split the banking lobby, since community banks are the face the anti-yield argument. Indeed, the banks have been doing the same: driving a wedge between Coinbase and the rest of crypto. Not sure what...

By Alex Johnson

Social•Jan 17, 2026

Coinbase Stands Firm on Its Non‑Negotiable Principle

Great points in this thread. There’s a reason why Coinbase has made this the hill it’s willing to die on.

By Alex Johnson

Social•Jan 16, 2026

Sportsbooks Predict Customer Value Faster Than Banks

All of this is nuts, but these two facts are especially mindblowing: - One gambling consultant tells The Economist that “By the time a customer places his first bet, [sportsbooks] are 80-90% certain they know the lifetime value of the account.” -...

By Alex Johnson

Social•Jan 16, 2026

Wells Fargo Execs Mock Bilt’s Profitable Model

“If Bilt can do it and be profitable” The executive at Wells Fargo are laughing their asses off right now.

By Alex Johnson