Video•Jan 25, 2026

The Problem with Equal Weight Index Funds

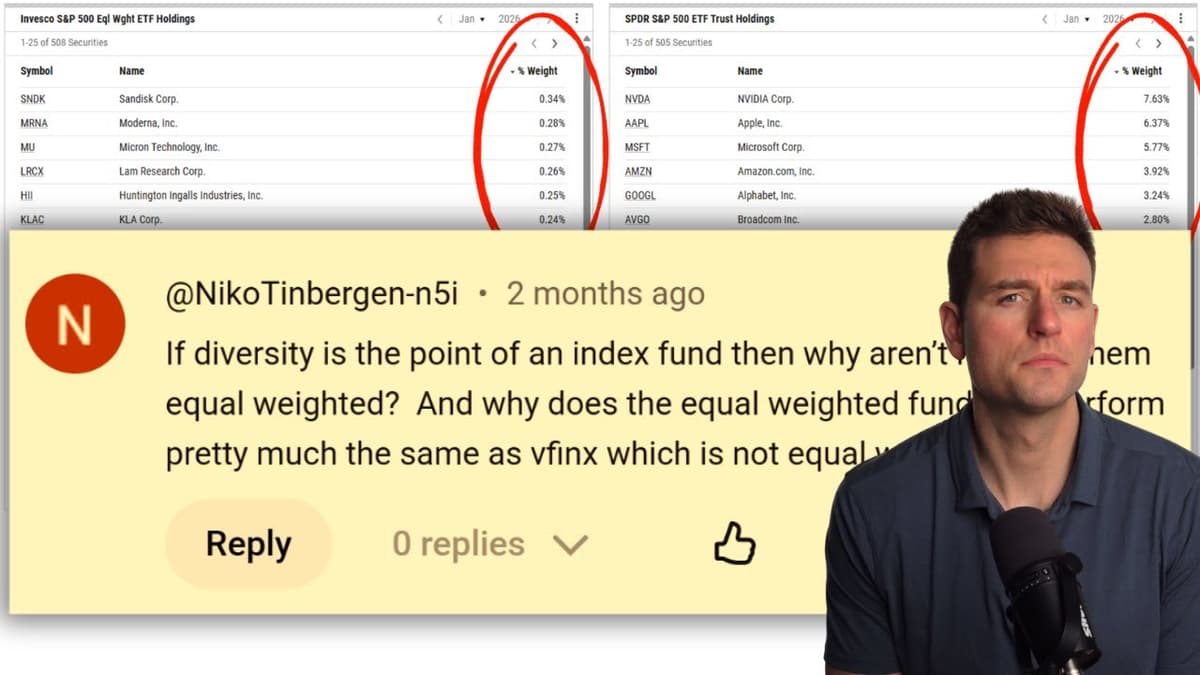

The video examines why equal‑weight index funds, despite their popularity, are not a superior alternative to market‑cap weighted funds. Ben Felix explains that equal weighting eliminates the heavy concentration in mega‑caps like Apple, but it does so by forcing large rebalancing trades, creating higher turnover, added transaction costs, and a systematic short‑momentum bias.

Key data points include the Invesco S&P 500 Equal Weight ETF’s modest outperformance since 2003, a turnover rate more than ten times that of a traditional cap‑weighted S&P 500 ETF, and a 15‑year standard deviation noticeably higher than its cap‑weighted counterpart. Factor regressions show the equal‑weight fund loading positively on size and value while loading negatively on momentum, indicating that its returns stem largely from exposure to smaller, cheaper stocks rather than any intrinsic advantage of equal weighting.

Felix contrasts this with Dimensional’s US Core Equity fund, which achieves comparable small‑cap and value tilts with a net expense ratio of 0.15% versus 0.20% for the equal‑weight ETF, and does so with far lower turnover and without a negative momentum exposure. The fund’s sector caps and selective trading rules illustrate how intentional factor tilts can replicate the benefits of equal weighting while avoiding its inefficiencies.

For investors, the takeaway is clear: if the goal is to reduce concentration and gain exposure to lower‑priced, smaller‑cap stocks, a smartly designed factor‑tilted fund can deliver the same risk‑adjusted returns with less volatility, lower costs, and fewer unintended bets. Equal weighting is not a magic solution; it merely packages known factor exposures in a less efficient vehicle.