Recent Posts

Social•Feb 18, 2026

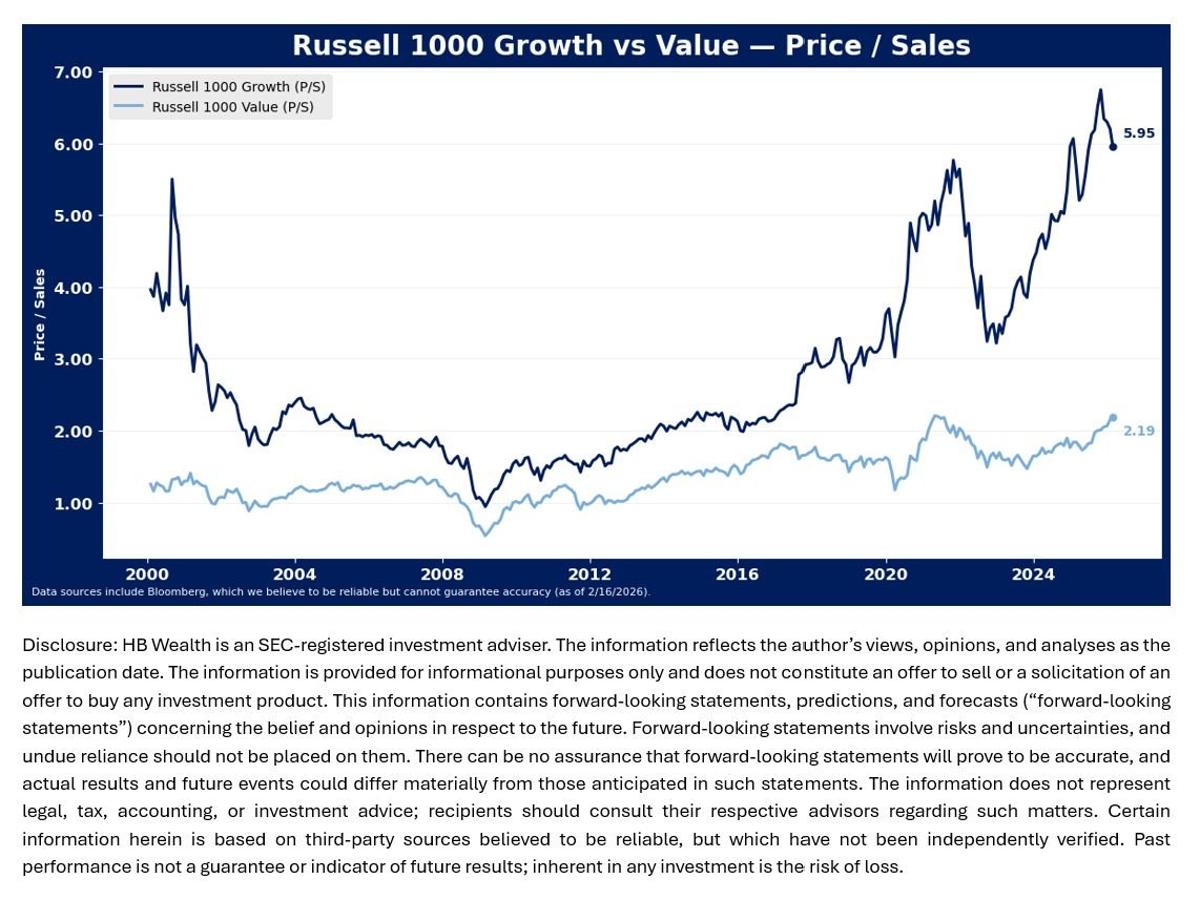

US Large‑Cap Valuations Still Overpriced, Risks Loom

Recent rotation has helped resolve some of U.S. large cap stocks’ valuation excesses, but risks remain to the downside for U.S. multiples. Large cap growth’s sales multiple is still near its all-time high, at about 6X, and growth’s earnings multiple may still be at least 15% too rich to value. The eye-popping growth premium is not the only evident excess in stocks, however, for now large cap value stocks are also trading very near all-time high valuations. These very high expectations have started to weigh on U.S. large cap growth stocks and may remain a problem for U.S. large cap returns overall in the near term.

By Gina Martin Adams, CMT, CFA