JunkBondInvestor

Creator

0 followers

Credit analyst focused on high yield bonds, leveraged loans, and distressed/special situations with frequent deal/document analysis.

Recent Posts

Social•Feb 20, 2026

Most Weekly BDC Discounts Are Mispriced—Learn Why

Everyone has a BDC take this week. Most of them are wrong. If you don't understand how they trade, what drives the discount, or why NAV isn't what you think it is, start here. https://www.junkbondinvestor.com/p/the-bdc-primer-part-1

By JunkBondInvestor

Social•Feb 18, 2026

Demand Surge Compresses Bond Spreads Despite Record Issuance

Record bond issuance. Record trading volumes. Tighter spreads. More supply should widen spreads. Instead buyers are so hungry that more issuance actually improves liquidity and compresses risk premiums. This works until it doesn’t.

By JunkBondInvestor

Social•Feb 18, 2026

CLOs Bet on Yield While AI Threatens Software Holdings

This is the CLO market right now: Sellers: AI will destroy these businesses Buyers: Thanks for the yield Software is the largest sector in CLO portfolios globally. 10-15% concentration. Nearly half mature in the next 3 years. Someone here is wrong.

By JunkBondInvestor

Social•Feb 17, 2026

AMC Refires $2.5B to Trim Maturity Wall

AMC moving to clean up its maturity wall. $2.5B package taking out 2027 notes (12.75%) and 2029 TL If it prices well, decently lower interest burden. $AMC

By JunkBondInvestor

Social•Feb 16, 2026

Private Credit Bets on Software Amid AI Uncertainty

Five private credit firms just provided $1.4B for a software buyout of OneStream valued at $6.4B. Same week everyone’s asking whether AI will make these companies obsolete. The market is telling you software is at risk. The lenders are telling you...

By JunkBondInvestor

Social•Feb 16, 2026

Alphabet and Meta CDS Explode From Zero to Top Traders

A year ago, CDS on Alphabet and Meta didn't exist. Now they're among the most actively traded single-name contracts in the US market Nobody creates a default insurance market for fun... $GOOG $META

By JunkBondInvestor

Social•Feb 16, 2026

AI Disruption Drives Widening Credit Spreads Ahead of Earnings

AI disruption is hitting IG credit spreads, not just stock prices. Concentrix: BBB-rated, 455,000 call center employees. Paid 130bps concession to refinance. Stock down 24% last week. Spreads doubled in February. Credit markets pricing obsolescence before it shows up in earnings.

By JunkBondInvestor

Social•Feb 13, 2026

BDC Quarterly Letters: Refusing Write‑Downs, Defying Pressure

Every BDC quarterly letter should just say “we are choosing not to mark this down and you can’t make us.”

By JunkBondInvestor

Social•Feb 13, 2026

Most Private Credit PIK Is Bad Yet Labeled Performing

58% of PIK in private credit is "bad PIK" per Lincoln. Borrower stops paying cash. Lender accepts more debt instead. Everyone marks it at par. This is called "performing."

By JunkBondInvestor

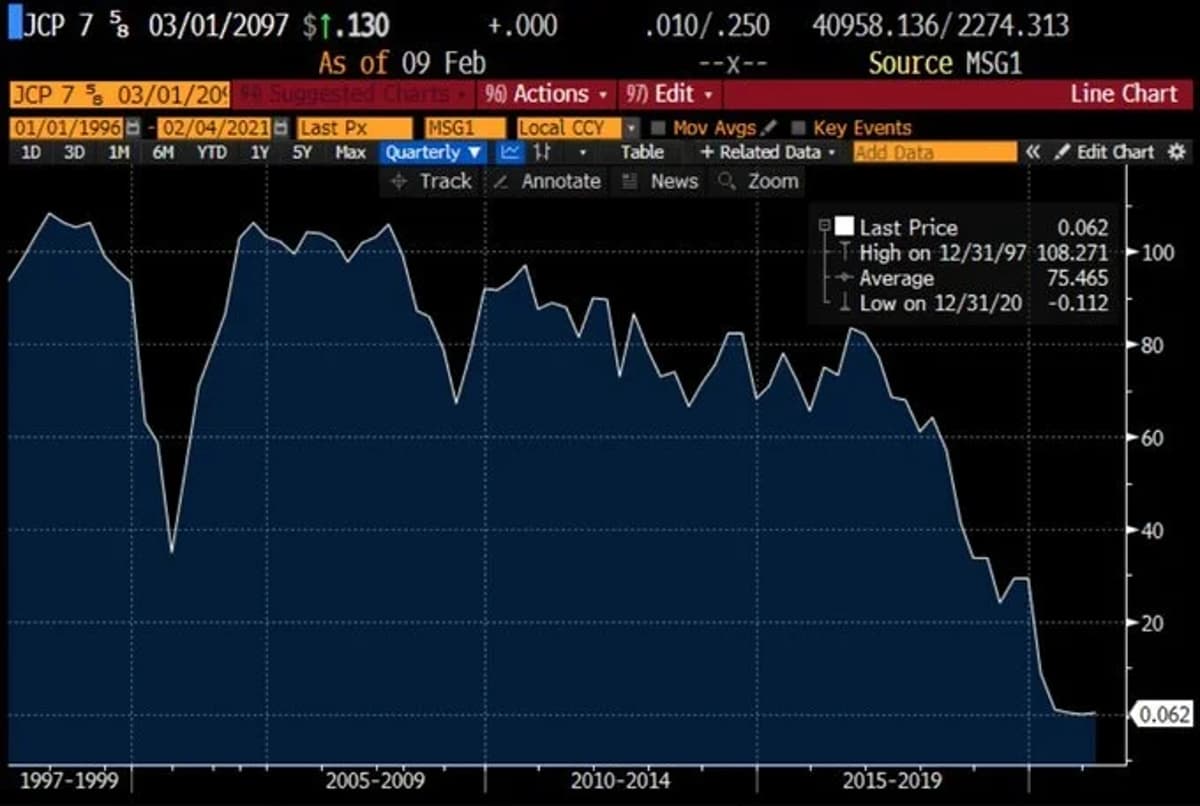

Social•Feb 10, 2026

Google’s 100‑Year AI Bond: Ambitious or Foolhardy?

Google issuing a 100-year bond to fund AI capex. Remember JC Penney’s 100-year bond? Issued in 1997. Bankrupt in 2020. At least they got their basis back in coupons.

By JunkBondInvestor