Sergey CYW

Creator

0 followers

Analyst covering Big Data companies and AI infrastructure (e.g., Snowflake, Confluent, MongoDB) with valuation and growth analysis.

Recent Posts

Social•Feb 19, 2026

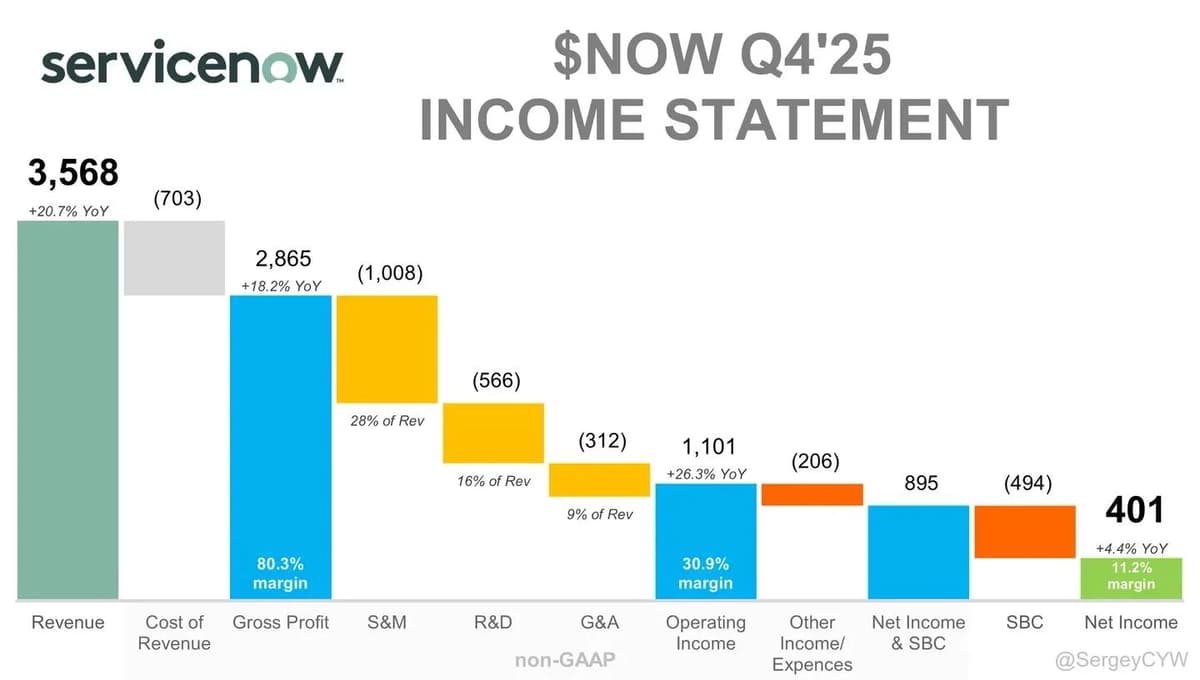

AI Could Boost ServiceNow, Not Just Threaten It

Is $NOW really at risk of AI disruption? $NOW is down ~52% from ATH. The bear case is simple: ~97% of revenue is seat-based. If AI reduces headcount, seat growth slows. But the real question is whether AI replaces ServiceNow… or makes it more central. Management is targeting $1B in AI-related ACV by 2026. That’s roughly 6–7% of projected ~$15.5B FY26 revenue. Not massive on its own, but meaningful this early in the adoption curve. Investing

By Sergey CYW

Social•Feb 17, 2026

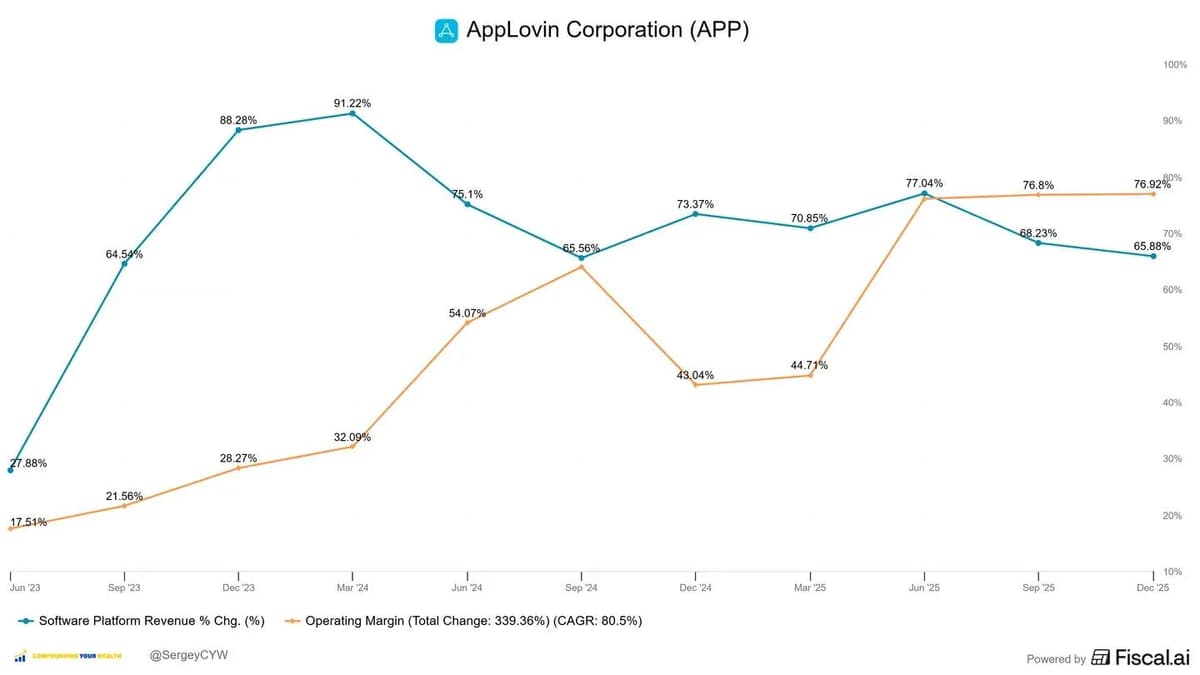

AppLovin's 66% Growth, 77% Margin, Stock Still Falls

$APP Growing 66% With 77% Operating Margin — Yet Stock Is Down 42% YTD AppLovin delivered numbers most software companies can’t even model. Revenue up +66% YoY. Operating margin at 77%. And yet the stock is still down 42% YTD. Valuation argument? Forward P/S around 16x. Forward...

By Sergey CYW

Social•Feb 13, 2026

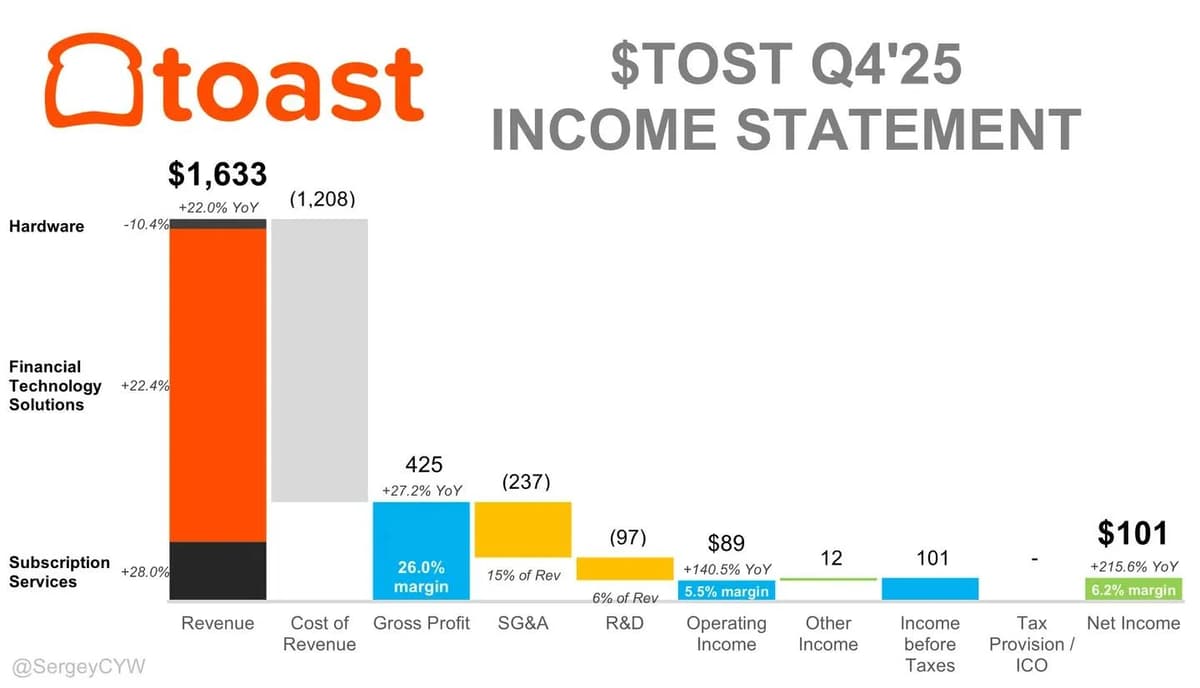

TOST Q4 Margins Surge, Profit Spikes over 200%

$TOST Q4: Operating income +140% YoY, net income +216% YoY. Margins expanding across the board. Revenue came in at $1.63B, up 22% YoY. Growth moderated vs +25% last quarter, but profitability stepped up meaningfully. Gross profit grew 27% YoY with gross margin...

By Sergey CYW