Video•Apr 24, 2026

Bayesian Linear Regression and Maximum a Posteriori (MAP) Estimate

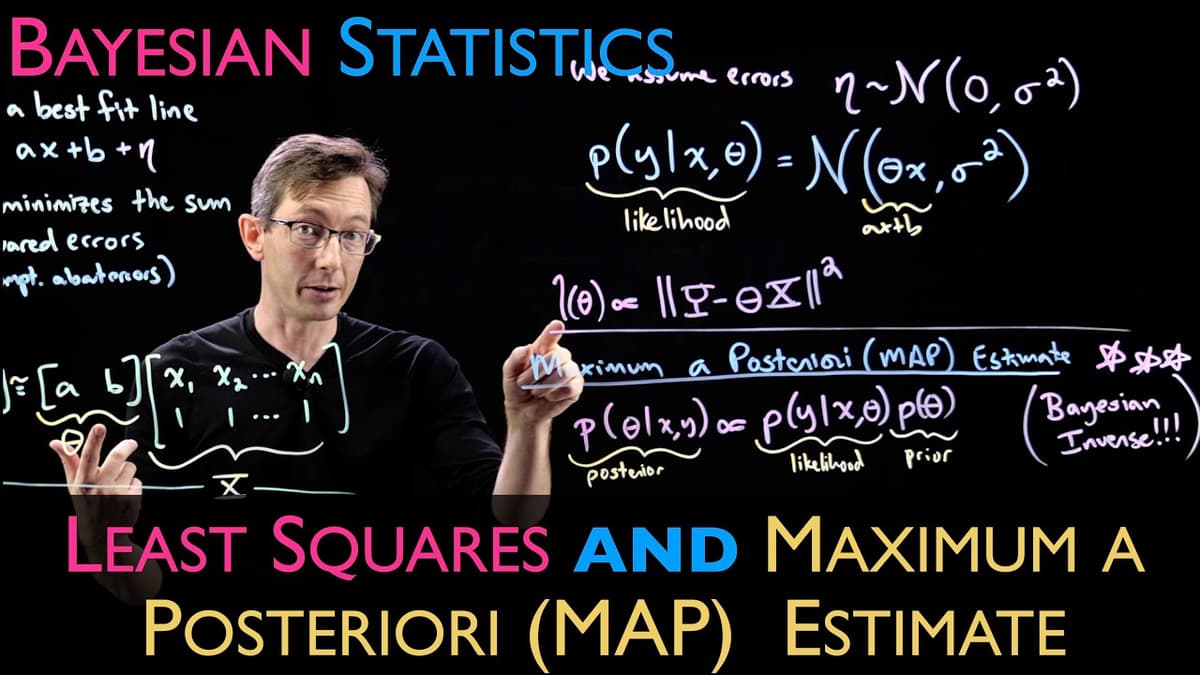

The video introduces Bayesian linear regression, a framework that models regression coefficients as random variables rather than fixed numbers, allowing analysts to incorporate prior knowledge and quantify uncertainty. It explains how the prior distribution, likelihood from observed data, and Bayes’ theorem combine to produce a posterior distribution over the coefficients.

Key insights include the use of conjugate priors—such as Gaussian priors for linear models—to obtain analytical posterior formulas, and the derivation of the Maximum a Posteriori (MAP) estimate as the mode of this posterior. The MAP solution mirrors regularized least‑squares, with the prior acting as a penalty term that shrinks coefficients toward prior expectations.

The presenter cites a concrete example: predicting house prices where a Gaussian prior centered on historically typical coefficients yields a posterior that balances new market data with long‑term trends. A quoted line emphasizes, “The MAP estimate gives you the best single‑point prediction while still respecting the uncertainty encoded in the posterior.”

For practitioners, the approach offers a principled way to regularize models, improve out‑of‑sample performance, and generate credible intervals for forecasts—critical for risk‑aware decision‑making in finance, marketing, and operations.