6 Brutal Money Stats of the Average American (2026)

The video breaks down the stark financial reality facing the average American in 2026, covering income, expenses, debt, net worth and retirement savings. It shows that a median full‑time worker earns about $52,000 a year before taxes, translating to roughly $3,000 after‑tax monthly, while the average household spends $6,545 each month on housing, transportation and food alone. Key data points include a median credit‑card balance of $9,000 carrying roughly 24% interest, a median net worth of $192,700 that collapses to under $60,000 once home equity is stripped out, and a median retirement nest egg of $65,000—equating to just $293 a month under the 4% withdrawal rule plus Social Security. The presenter highlights that 25% of Americans have zero retirement savings and that most stop working at 61, well before full Social Security benefits begin. Notable remarks stress the futility of investing while carrying high‑interest debt, urging viewers to prioritize debt repayment over market returns. The host also points out that home equity inflates net‑worth figures but offers little liquidity, and uses personal anecdotes about grandparents retiring abroad to illustrate the inadequacy of current retirement income. The implications are clear: without higher earnings, disciplined saving (10‑15% of after‑tax income), and early debt elimination, most Americans will face financial strain in retirement. The video calls for proactive financial education, higher savings rates, and leveraging assets that preserve purchasing power amid inflation.

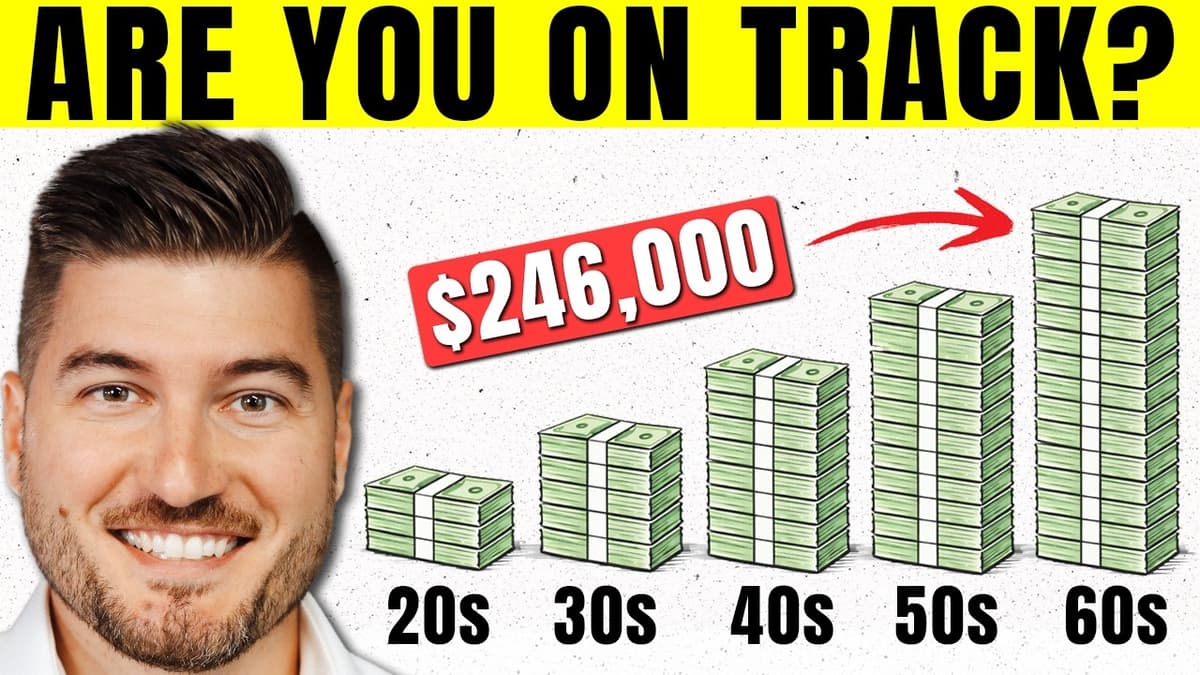

The Exact Amount You Should Have Saved At Every Age

The video outlines age‑specific savings targets, contrasting median household net‑worth figures with aggressive benchmarks that tie saved assets to multiples of annual salary. It emphasizes that by the late 20s you should be forming disciplined habits, contributing at least 10‑15%...

The Exact Order To Invest Your Money (Most People Get This Wrong)

The video explains that the sequence in which you allocate money—starting with safety nets and debt—determines long‑term wealth far more than chasing hot stocks. It recommends first a $1,000 emergency stash, then a full 3‑6‑month liquid reserve, followed by eliminating any...

How Much Car Can You Actually Afford? (By Salary)

The video breaks down how much car you can truly afford by tying vehicle costs to four income brackets—$50,000, $75,000, $100,000 and $150,000. It starts with the stark fact that the average new‑car payment in the United States is $767...

Why One Big Purchase Is Never Enough

The video explains why a single big purchase often leads to a cascade of additional spending, coining the “Dero effect” after an 18th‑century philosopher who upgraded his life piece by piece until broke. It outlines how the anchor item creates a...

Your Car Payment Is Stealing Your Retirement (The Math They Don't Show You)

The video argues that the most common financial decision in America—financing a new car—acts as a hidden retirement drain. By focusing on monthly payments rather than total cost, consumers overlook steep depreciation, financing charges, taxes, insurance, fuel and maintenance, turning...