Can Middle East Oil Producers Meaningfully Bypass the Strait?

Why It Matters

The limited but viable bypass capacity reshapes global oil logistics, influencing price volatility and geopolitical leverage for both producers and consumers. Understanding these constraints helps investors gauge supply‑risk premiums and policy makers assess regional stability.

Key Takeaways

- •Saudi East‑West pipeline exports up to 5 m bpd via Red Sea port Yanbu

- •UAE Habshan‑Fujairah line adds ~1.5 m bpd, still within Iranian strike range

- •Iraq’s Kirkuk‑Ceyhan pipeline runs below its 1.6 m bpd design

- •All alternative routes face attack risk, political disruption, higher costs

- •Red Sea traffic stays suppressed due to Bab al‑Mandeb security concerns

Pulse Analysis

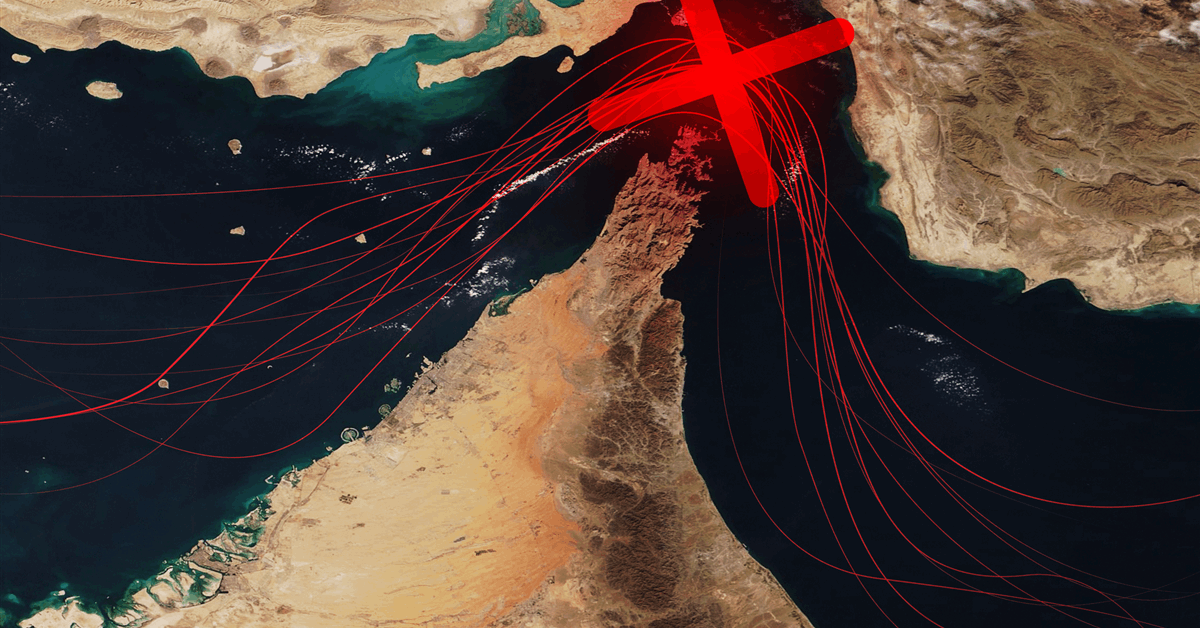

The East‑West Petroline across Saudi Arabia offers the most substantial alternative to the Hormuz chokepoint, moving up to seven million barrels per day and delivering roughly five million barrels to the Red Sea port of Yanbu. While the buried pipeline reduces direct sabotage, its pumping stations, terminals and the port itself remain exposed, as demonstrated by the recent strike that knocked out 700,000 barrels per day. This capacity, however, falls short of Saudi’s total export needs, forcing producers to rely on higher‑cost routes and price premiums.

The United Arab Emirates’ Habshan‑Fujairah pipeline and Iraq’s Kirkuk‑Ceyhan line provide additional, albeit smaller, volumes. The UAE line can transport about 1.5 million barrels daily to Fujairah, but the port lies within range of Iranian weapons, making it a recurrent target. Iraq’s pipeline operates below its 1.6 million‑bpd design, limiting its contribution to regional supply. Together, these routes can offset roughly half of Hormuz traffic, but their vulnerability to geopolitical shocks and the need for elevated freight rates diminish their strategic reliability.

Security concerns in the Red Sea, especially around the Bab al‑Mandeb Strait, further constrain the shift away from Hormuz. While Russia and China have continued transits, many commercial shippers avoid the corridor due to lingering Houthi threats and the risk of renewed attacks. Consequently, oil markets continue to price in a supply‑risk premium, and policymakers must weigh the trade‑off between diversifying export pathways and exposing critical infrastructure to new security challenges.

Can Middle East Oil Producers Meaningfully Bypass the Strait?

Comments

Want to join the conversation?

Loading comments...