Diesel Backup Gensets Are Big Winners From the Data Centre Boom. Our Cities Would Be Better Off with Batteries

Why It Matters

The diesel‑gen set boom adds billions to data‑centre CAPEX, strains grid capacity, and raises emissions, while the emerging battery‑gen hybrid model could reshape cost structures and market participation if regulators adapt.

Key Takeaways

- •Tier IV data centres require 96‑hour diesel backup per megawatt

- •Diesel genset CAPEX ≈ $1.6 B USD per GW built

- •Generator prices rose ~45% since 2021, lead times now 2‑3 years

- •Batteries cover most outages but cannot economically meet 96‑hour tail risk

- •New IESS rules enable storage‑gen hybrid participation in Australian markets

Pulse Analysis

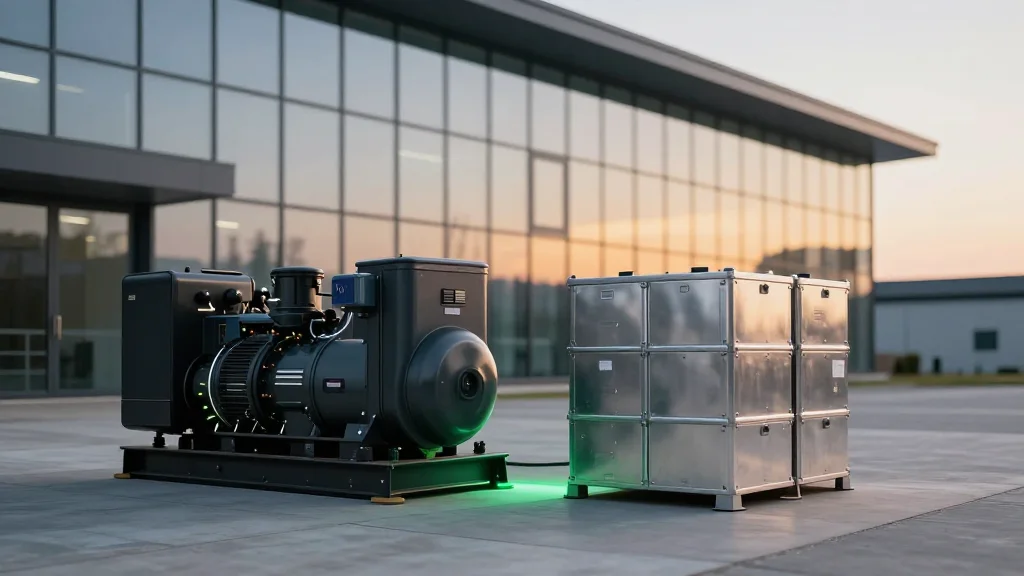

The data‑centre boom is redefining power reliability standards. Tier IV facilities, which command 99.995% uptime, must install diesel generators capable of sustaining operations for four days without grid power. In Australia, this translates to roughly 5 GW of diesel capacity under construction, representing about $8 billion USD in capital outlay and $250 million USD in recurring operating expenses. The sheer scale of diesel storage—tens of millions of litres—poses logistical challenges and heightened environmental scrutiny, especially as the sector accounts for up to 20% of national electricity consumption.

Economically, diesel generators have become a commodity under pressure. Capital costs have climbed 45% since 2021, driven by rising copper, specialty steel, and OEM pricing power, while lead times have stretched to 24‑30 months for 2‑3 MW units. OPEX remains significant, with fuel, testing, and service contracts averaging $5.25 million USD per 100 MW site annually. Batteries offer a lower‑cost alternative for typical outages of 4‑8 hours and can generate revenue through frequency control ancillary services (FCAS) and the Renewable Energy Target (RERT) market. However, their economics break down for the rare but severe 96‑hour tail events, keeping diesel as the default safety net.

Regulatory shifts could tip the balance. The Integrating Energy Storage Systems (IESS) rule, effective June 2024, creates an Integrated Resource Provider category that permits hybrid diesel‑battery assets to compete in energy and ancillary service markets. Coupled with potential AEMC reforms to allow backup generators in virtual power plant schemes, data‑centre operators may soon monetize standby capacity, reducing reliance on pure diesel. Investors and grid planners should watch for consolidation around centralized backup hubs—such as a Tomago‑style facility—and for policy incentives that could accelerate the transition toward cleaner, more flexible resilience solutions.

Diesel backup gensets are big winners from the data centre boom. Our cities would be better off with batteries

Comments

Want to join the conversation?

Loading comments...