Rewriting the RFS Playbook: Final 2026-2027 RVOs for Biomass-Based Diesel

Key Takeaways

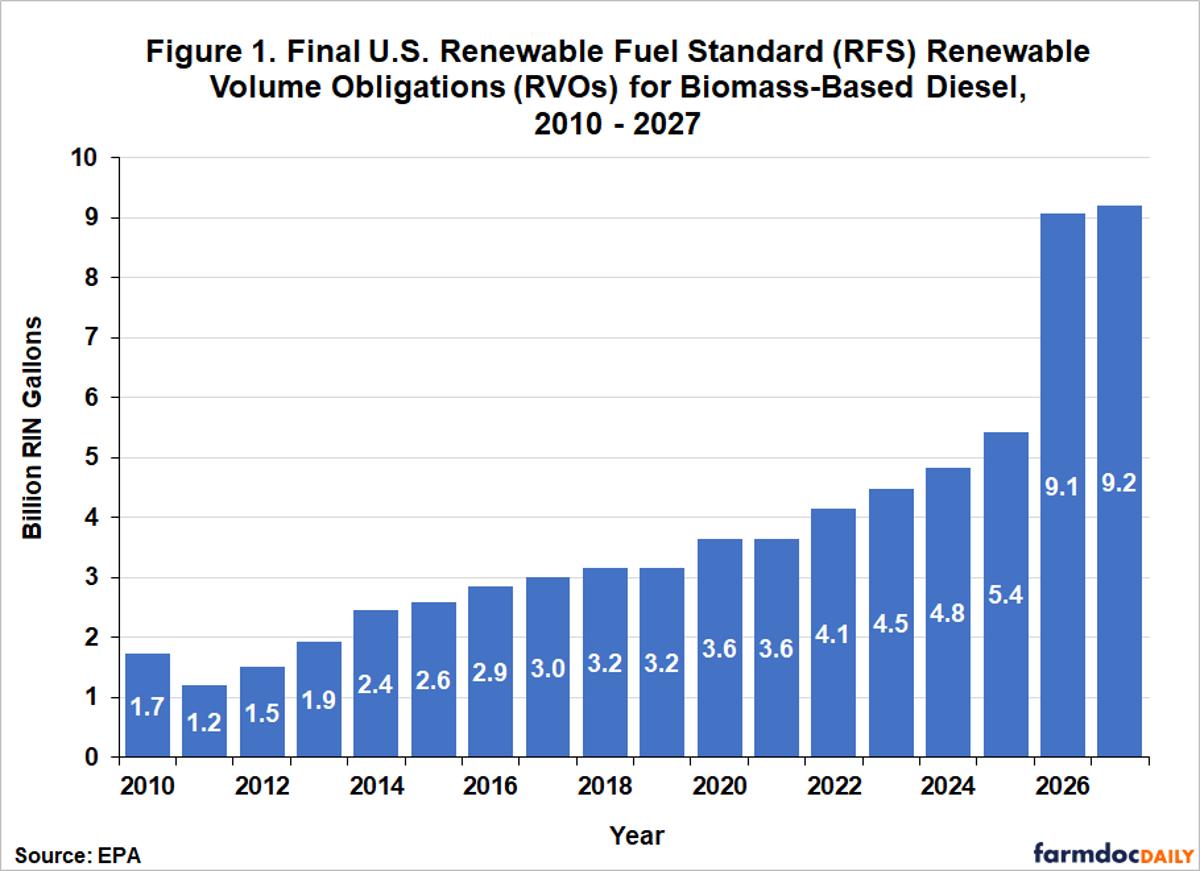

- •EPA mandates 9.07 bn RIN gallons biomass diesel in 2026

- •2027 requirement rises to 9.20 bn RIN gallons, 70% above 2025

- •70% of 2023‑2025 small refinery exemptions reallocated to RVOs

- •Half‑RIN import penalty postponed until 2028, easing compliance

- •Equivalence value for renewable diesel lowered to 1.5 RIN gallons in 2027

Pulse Analysis

The EPA’s final Set 2 rule marks a watershed moment for the U.S. renewable fuel landscape. By assigning 9.07 billion RIN gallons to biomass‑based diesel in 2026 and 9.20 billion in 2027, the agency has effectively tripled the annual demand compared with 2025 levels. This aggressive stance reflects a policy shift toward deeper decarbonization of the diesel pool, and it forces producers to accelerate capacity expansions, secure additional feedstock, and navigate tighter compliance margins. The reallocation of 70% of small refinery exemptions further tightens the supply‑demand balance, pushing obligated parties to source more renewable diesel or biodiesel to meet the heightened standards.

From a market‑structure perspective, the rule’s adjustments to equivalence values and the postponement of the half‑RIN import penalty create a nuanced compliance environment. Renewable diesel’s equivalence factor drops to 1.5 RIN gallons starting in 2027, aligning it with biodiesel and potentially dampening the premium previously enjoyed by renewable diesel producers. Meanwhile, the delayed half‑RIN penalty—originally slated for 2025—offers a temporary compliance cushion, allowing firms to phase in additional production without immediate financial penalties. Investors and traders should monitor how these regulatory tweaks influence RIN price volatility and the arbitrage opportunities between domestic production and imported feedstocks.

Looking ahead, the scale of the new obligations will reverberate through feedstock supply chains, especially for corn oil, soybean oil, and waste‑derived fats. Anticipated capacity builds at refineries and dedicated biofuel plants will likely spur capital spending, while logistics networks will need to adapt to higher volumes of renewable diesel and biodiesel. Stakeholders should also watch for potential policy refinements, such as EPA’s possible petition to raise renewable diesel’s equivalence value back to 1.6, which could reshape the competitive dynamics within the biomass‑based diesel segment. In sum, the final RVOs set a clear, high‑stakes trajectory for the industry, demanding strategic investments and agile compliance strategies.

Rewriting the RFS Playbook: Final 2026-2027 RVOs for Biomass-Based Diesel

Comments

Want to join the conversation?