Fitch Stress Test Sees No Turkish Bank Failure Even if Iran Conflict Drives Lira to USD/75

Companies Mentioned

Why It Matters

The findings reassure investors that Turkey’s banking system remains resilient under extreme exchange‑rate stress, limiting systemic risk and supporting credit availability. However, the isolated breach at Halkbank signals a potential focal point for policy intervention if the crisis deepens.

Key Takeaways

- •Only Halkbank breaches legal CET1 ratio in severe scenario

- •Average CET1 buffers: 7.2% private, 5.5% state-owned banks

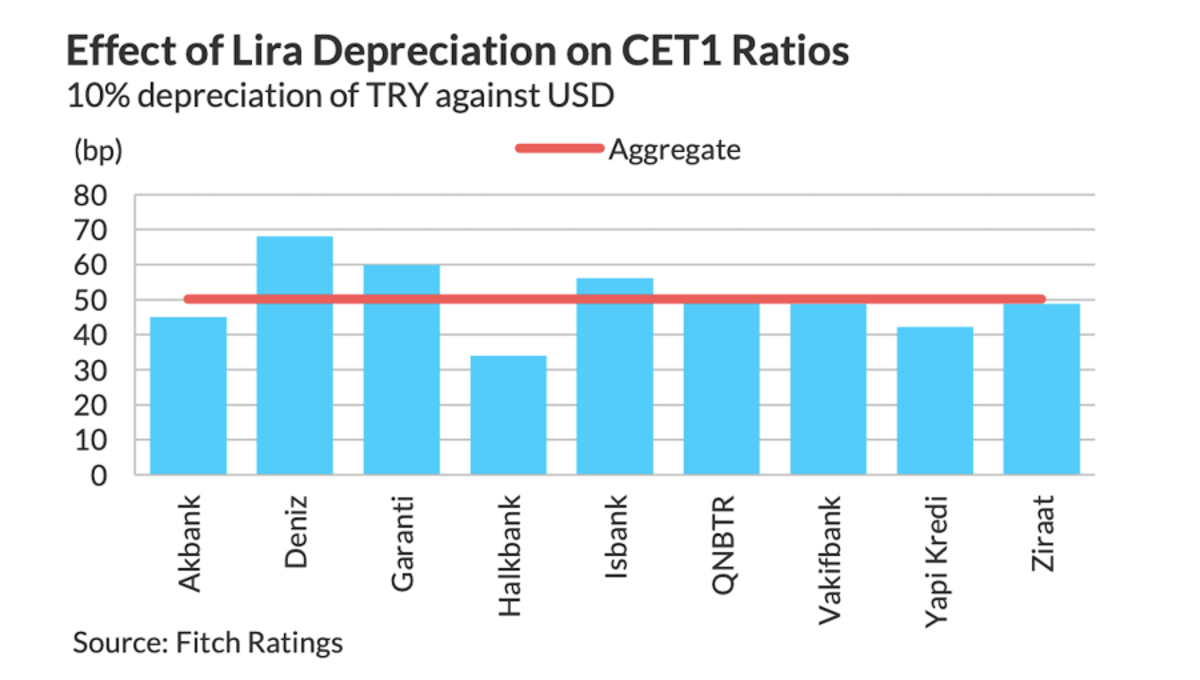

- •10% lira depreciation cuts aggregate CET1 by ~50 basis points

- •Fitch assumes no extra shareholder or regulatory support through 2026

Pulse Analysis

Turkey’s banking sector faces heightened scrutiny as the Iran‑Russia conflict threatens to push the lira toward 75 per dollar. Fitch Ratings’ latest stress test, commissioned to answer investor concerns, models three exchange‑rate paths and corresponding non‑performing loan (NPL) spikes. The base case assumes a USD/TRY of 49.5, while the severe scenario tests a 75 level and a 7.5% NPL ratio by 2026. Even under these duress conditions, the aggregate capital adequacy of the nine major banks remains above the Basel III minimum, underscoring the sector’s built‑in resilience.

The test reveals a clear split between state‑owned and private institutions. Private banks, led by QNB Turkey with a 9.1% CET1 buffer, hold an average cushion of 7.2% of gross loans, compared with 5.5% for state banks. Halkbank emerges as the outlier, its CET1 ratio projected to dip 108 basis points below the 4.5% legal floor in the severe scenario. A 10% depreciation of the lira would shave roughly 50 basis points off the sector’s combined CET1, while a one‑percentage‑point rise in NPLs would erode another 46 basis points, highlighting the sensitivity of capital ratios to both currency and credit quality shocks.

For investors and policymakers, the results carry mixed signals. The overall robustness suggests that systemic contagion is unlikely, reducing the urgency for emergency liquidity injections. Yet the isolated vulnerability of Halkbank could prompt targeted regulatory forbearance or shareholder recapitalisation if market stress intensifies. Moreover, the removal of two forbearance measures earlier this year already trimmed capital ratios by 170–200 basis points, indicating that policy levers remain available. As Turkey navigates external geopolitical risks and domestic inflation pressures, monitoring lira movements and NPL trends will be critical for assessing future credit risk and the need for policy support.

Fitch stress test sees no Turkish bank failure even if Iran conflict drives lira to USD/75

Comments

Want to join the conversation?

Loading comments...