Power Module Packaging Evolution Amid Material Innovation, Supply Chain Shifts

Companies Mentioned

Why It Matters

The evolution of power‑module packaging directly impacts the efficiency, reliability, and cost of EVs, renewable‑energy converters, and industrial drives, making it a critical lever for the broader electrification agenda. Companies that secure resilient, locally‑sourced packaging supply chains will gain a competitive edge as demand accelerates.

Key Takeaways

- •Global power module market projected $20 bn by 2031, 10% CAGR.

- •Packaging materials now one‑third of module cost, shifting to 30% by 2031.

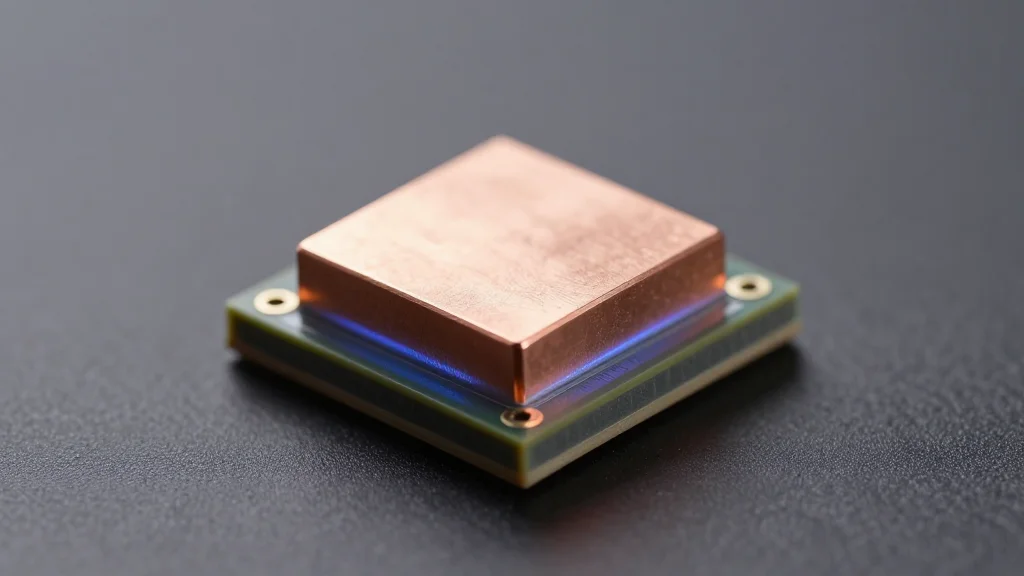

- •Copper interconnections and silicon‑nitride substrates dominate next‑gen packaging.

- •Asian region supplies 70%+ of packaging components, driving supply‑chain concentration.

- •Companies adopt “China+1” diversification to mitigate geopolitical and logistics risks.

Pulse Analysis

Electrification across transportation, renewable energy, and industrial automation is reshaping the power electronics landscape, with power modules emerging as the linchpin of high‑efficiency converters. The market’s projected $20 billion size by 2031 reflects a compound annual growth rate of roughly 10%, underscoring the urgency for manufacturers to enhance thermal performance and reliability. Packaging, which currently represents about 33% of a module’s bill of materials, is evolving from traditional aluminum interconnects to copper‑based solutions and from Al₂O₃‑DBC substrates to silicon‑nitride, delivering superior heat dissipation and mechanical robustness.

Material innovation is also redefining cost dynamics. While the share of packaging in total module cost is expected to dip modestly to 30% as silicon‑carbide devices command a larger portion of value, raw material demand for copper, silver, and silicon‑nitride is surging. Silver‑copper sintering for die‑attach and high‑filler encapsulants are gaining traction despite price pressures, prompting vendors to optimize usage and explore alternatives. These advances enable higher power densities and longer lifespans, essential for fast‑charging EV infrastructure and grid‑scale renewable converters.

The supply chain underpinning these materials remains heavily concentrated in Asia, where a dense ecosystem of mineral extraction, refining, and specialized component fabrication offers logistical efficiencies. Geopolitical tensions and long‑shelf‑life polymer constraints, however, are driving OEMs toward regionalization strategies such as “China+1,” expanding production to Malaysia, Vietnam, and other low‑cost hubs. This diversification not only mitigates risk but also positions firms to respond swiftly to local market demand, giving them a decisive advantage in the fiercely competitive power module arena.

Power Module Packaging Evolution Amid Material Innovation, Supply Chain Shifts

Comments

Want to join the conversation?

Loading comments...