Not Dead: Provider-Sponsored Plans Reassessing

Companies Mentioned

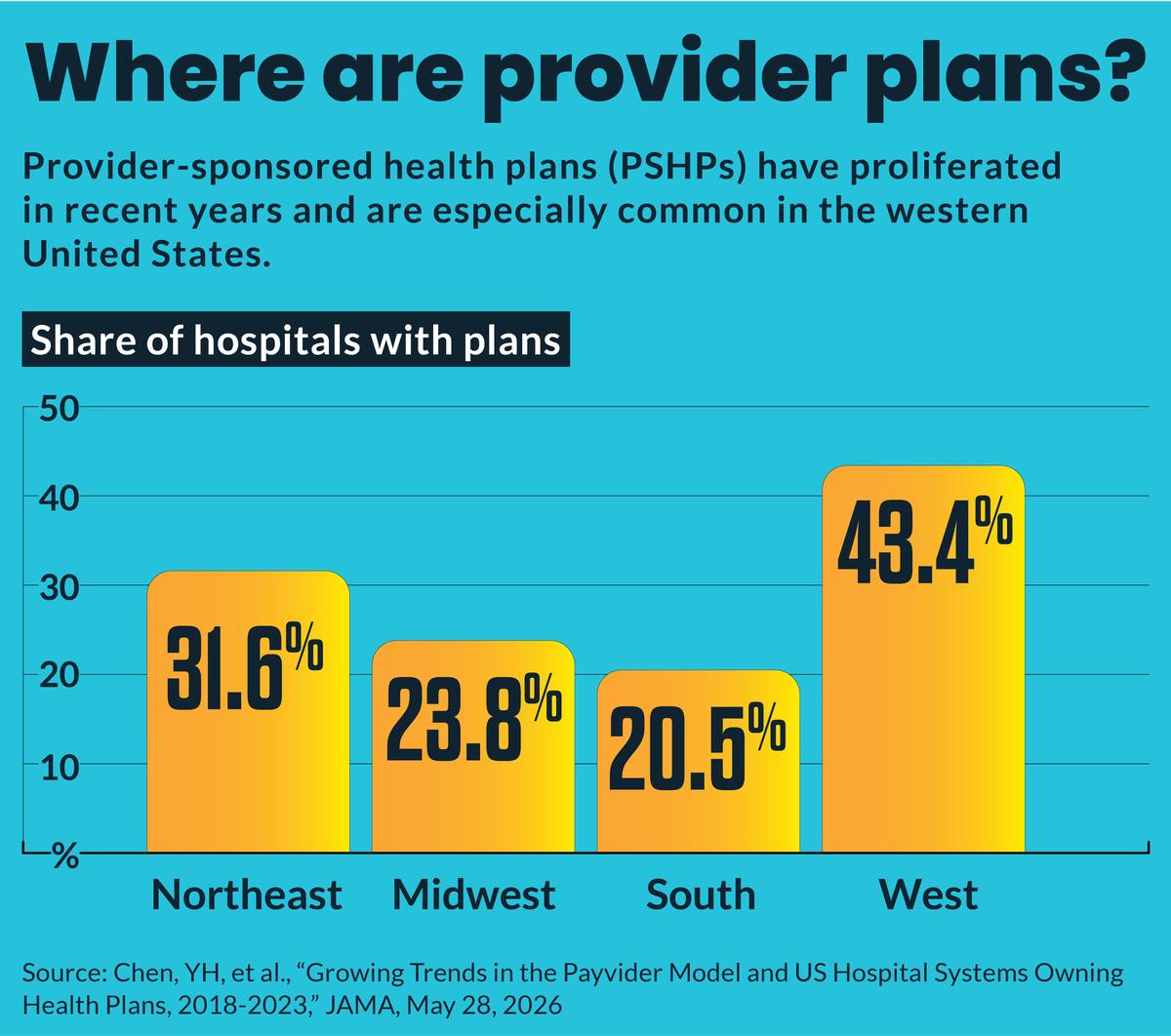

Why It Matters

The shift determines whether hospitals can leverage payer ownership as a profit center or face margin erosion, influencing overall health‑system financial stability and competitive positioning.

Key Takeaways

- •PSHP ownership rose from 18% to 27% of hospitals (2018‑2023)

- •Academic medical centers account for >35% of new provider‑sponsored plans

- •Recent exits include Presbyterian MA, Providence Medicaid, PacificSource ACA plans

- •Subscale PSHPs face lower EBITDA margins than systems without payer arms

- •Viable paths focus on partnerships, joint ventures, or targeted commercial products

Pulse Analysis

The past half‑decade has seen provider‑sponsored health plans (PSHPs) transition from niche experiments to a notable segment of the U.S. hospital landscape. A JAMA study shows ownership climbing from 692 hospitals (18.3%) in 2018 to 834 (27.2%) in 2023, driven largely by academic medical centers, where more than a third now run their own plans. Proponents argue that integrating payer functions can smooth cash flow by capturing revenue before services are rendered, offering a hedge against the fee‑for‑service squeeze.

Yet the rapid expansion collides with a tightening insurance market. Over the last year, several regional PSHPs announced pullbacks: Presbyterian Healthcare Services exited most Medicare Advantage (MA) products, Providence is winding down most of its plans by 2027, and PacificSource dropped ACA offerings in Montana. Analysts such as Alvarez & Marsal note that many of these plans are under‑capitalized and lack the scale to compete with established insurers, a gap reflected in below‑average operating EBITDA margins for systems that retain sizable payer arms.

Faced with mounting pressure, health systems are forced to choose between investment, partnership, consolidation, or exit. The Alvarez & Marsal report outlines five strategic levers, emphasizing joint ventures, delegated administration, or narrow self‑insured employee programs as the most realistic routes to achieve scale without shouldering full payer risk. Consolidation can unlock economies of scale, while outright exits preserve cash reserves. For providers, the decision now hinges on short‑term financial viability rather than long‑term vision, reshaping how hospitals view payer ownership as either a strategic anchor or a liability.

Not dead: Provider-sponsored plans reassessing

Comments

Want to join the conversation?

Loading comments...