Weird Health Insurance Concepts | Out-Of-Pocket

Key Takeaways

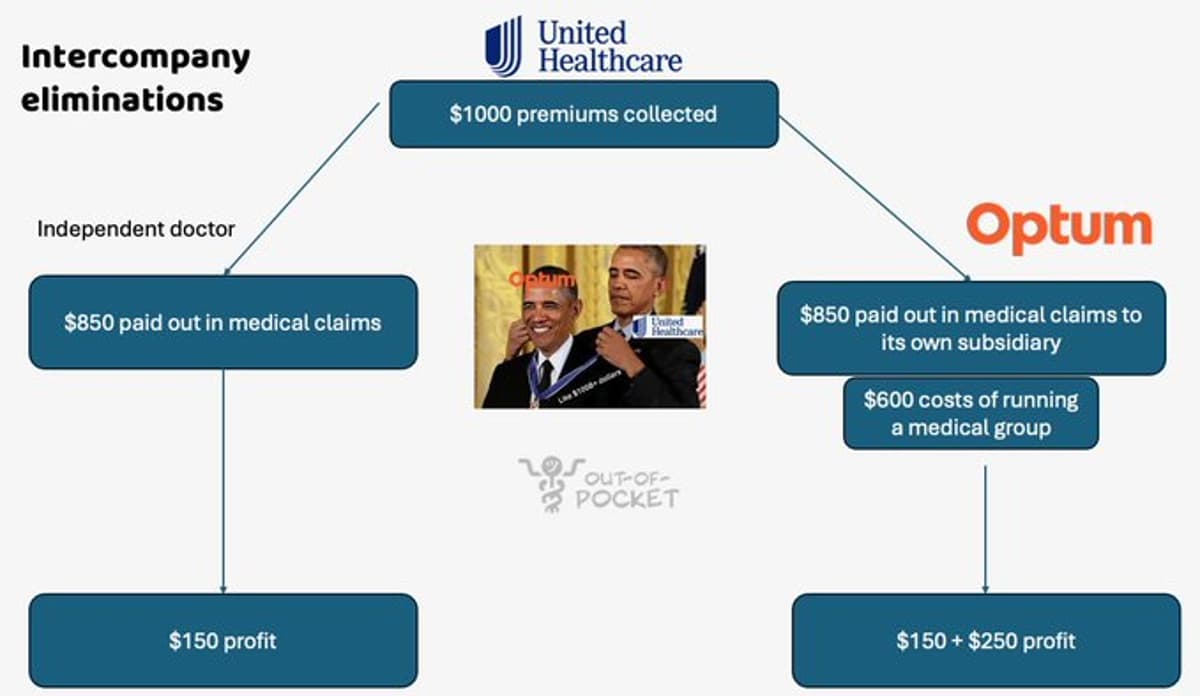

- •Intercompany eliminations let insurers count subsidiary payments toward loss ratios

- •Copay accumulators block manufacturer coupons from meeting deductibles

- •Copay maximizers inflate patient copays to increase pharma assistance

- •Reference-based pricing ties reimbursement to Medicare rates, limiting costs

- •RBP can generate surprise bills when providers reject payer rates

Pulse Analysis

Intercompany eliminations have become a cornerstone of vertical integration in the U.S. health‑insurance market. By treating payments to owned physician groups, PBMs, or specialty pharmacies as internal cost offsets, insurers can meet the 85 % medical loss‑ratio threshold while retaining a larger share of premium revenue. This accounting maneuver not only improves reported profitability but also creates incentives to steer patients toward in‑network, captive providers, potentially squeezing independent clinics out of the market.

Pharmaceutical manufacturers have responded to rising out‑of‑pocket burdens with copay assistance programs, prompting insurers to deploy two counter‑strategies. Copay accumulators exclude manufacturer coupons from deductible calculations, forcing patients to shoulder the full deductible before assistance applies. Conversely, copay maximizers artificially raise the patient’s share, prompting the manufacturer’s program to cover a larger amount. Both tactics reshape the cost‑sharing landscape, shifting financial pressure between insurers, drug makers, and consumers while complicating claims processing.

Reference‑based pricing (RBP) offers a different approach by anchoring reimbursements to a known benchmark—typically a percentage of the Medicare rate. Employers using self‑insured plans appreciate the predictability and potential savings, as RBP eliminates the need for complex provider negotiations. However, the model can generate surprise balance‑bills when providers reject the payer‑set rate, leading to disputes and administrative overhead. As more employers experiment with RBP, regulators and insurers must balance cost containment with patient protection to avoid unintended financial shocks.

Weird health insurance concepts | Out-Of-Pocket

Comments

Want to join the conversation?