Rising Health Costs Outpace Social Security for Retirees

Why It Matters

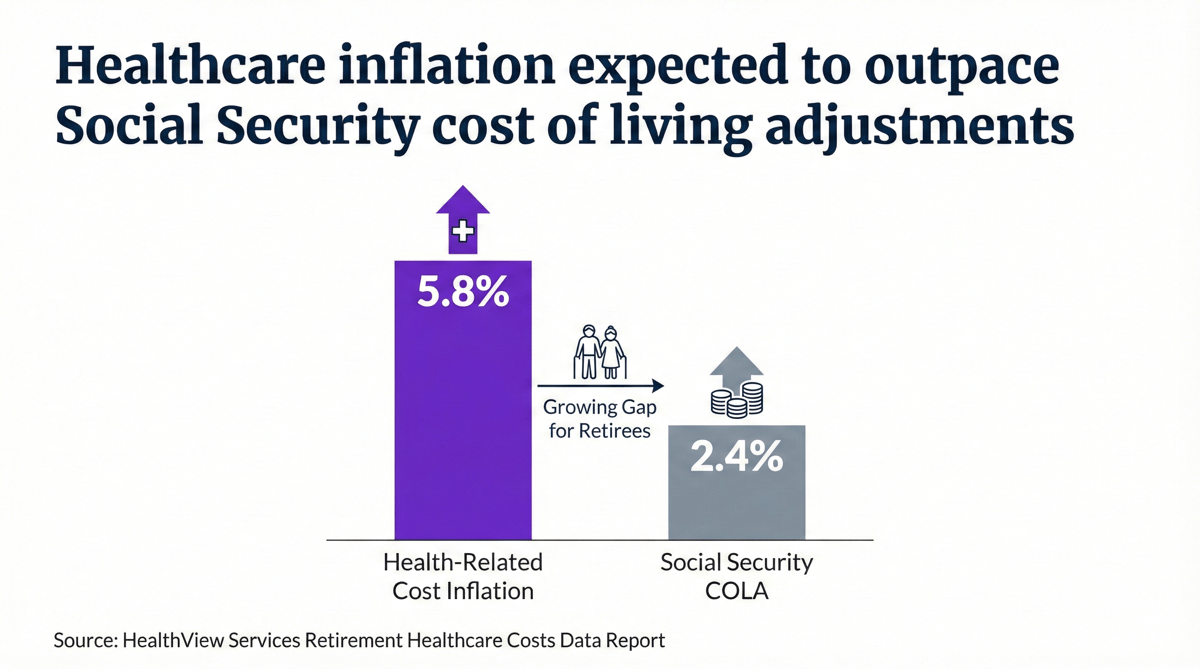

The disparity between health‑care cost growth and Social Security benefits erodes retirees’ purchasing power and pressures public and employer‑based health programs. Addressing this gap is critical for the financial security of an aging workforce.

Key Takeaways

- •Health cost inflation 5.8% outpaces 2.4% COLA.

- •Medicare Part B/Advantage premiums rose 9.7% in 2026.

- •Part D drug premiums up 50% since 2022.

- •Lifetime Medicare costs vary by state, up to $1.05M.

- •HSAs and benefit calculators can mitigate budgeting gaps.

Pulse Analysis

The accelerating pace of health‑care inflation is reshaping retirement economics. While Social Security’s automatic cost‑of‑living adjustments have steadied at roughly 2.4% per year, the HealthView Services report flags a 5.8% annual rise in medical expenses. This divergence means that each dollar of Social Security income now covers a smaller slice of a retiree’s health budget, amplifying financial vulnerability for seniors who rely heavily on fixed income streams.

Medicare’s own pricing dynamics compound the challenge. In 2026, premiums for Part B and Medicare Advantage climbed 9.7%, reflecting broader market pressures from hospitals operating near break‑even and pharmaceutical price hikes. Part D drug costs have surged 50% since the Inflation Reduction Act’s 2022 provisions, leaving high‑spending retirees especially exposed. Moreover, state‑level cost differentials are stark—annual lifetime medical expenses can range from $878,000 in Washington to over $1 million in Missouri—underscoring the geographic dimension of the problem and its ripple effects on small‑business benefit plans.

Financial planners and HR leaders are urged to counteract these trends with proactive tools. Maximizing Health Savings Account contributions allows retirees to grow tax‑advantaged funds that can offset out‑of‑pocket spending, while Social Security optimization calculators help individuals time benefit claims for maximum lifetime value. By integrating these resources into employee benefits education, companies can improve retirement readiness and alleviate the looming strain on both private and public health‑care safety nets.

Rising health costs outpace Social Security for retirees

Comments

Want to join the conversation?

Loading comments...