Florida Needs More, Much More Wind Mitigation. Experts at OIR Summit Give Ideas

Companies Mentioned

Why It Matters

Without broader incentives, Florida’s exposure to costly hurricanes will keep rising, pressuring insurers and taxpayers. Implementing the proposed reforms could lower premiums, reduce catastrophe losses, and create a new market for resilience‑focused construction and insurance services.

Key Takeaways

- •Florida's wind‑mitigation grants exceeded $300 million but target too few homes.

- •Upgrading to “code‑plus” adds $20‑30 k, while grant caps at $10 k.

- •Experts propose a uniform storm‑resistance grading system for homes.

- •Pilot programs could let lenders amortize mitigation costs and insurers fund upgrades.

- •Federal tax‑credit and surplus‑reserve reforms could lower homeowner premiums.

Pulse Analysis

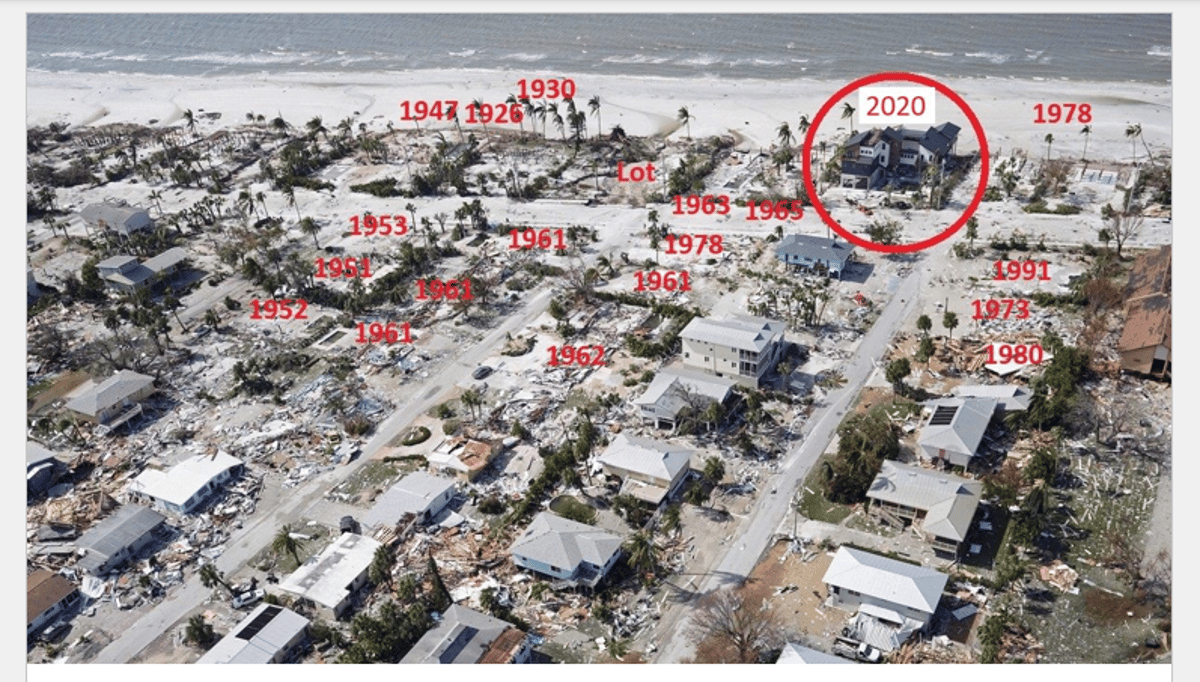

Florida remains the nation’s most hurricane‑prone state, and its $300 million wind‑mitigation grant program reflects a growing recognition of the need for resilient housing. Yet the program’s design—limited to $10,000 matching grants—covers only a fraction of the $20,000‑$30,000 extra outlay required for true "code‑plus" construction. As a result, many homeowners and builders view upgrades as a hard sell, while insurers continue to shoulder the bulk of catastrophe losses. The gap underscores a market failure where short‑term cost concerns eclipse long‑term risk reduction.

At the recent OIR summit, academics and actuaries outlined a multi‑pronged strategy to close that gap. Central to the plan is a uniform storm‑resistance grading system that would rate homes on comprehensive resilience measures, not just roof upgrades. Such a grade could become a marketing tool, influence mortgage terms, and feed data to catastrophe models. Coupled with pilot financing programs, lenders could amortize mitigation expenses over the life of a loan, while insurers might fund upgrades directly in exchange for lower future claims. Public‑private partnerships, tax‑credit accounts akin to health‑savings plans, and reforms allowing insurers to invest surplus reserves tax‑free for catastrophe coverage were also highlighted as levers to shift the economics in favor of hardening homes.

If adopted, these reforms could reshape Florida’s insurance landscape. Lower premiums and reduced claim volatility would improve insurer solvency, potentially easing the pressure on the state‑run Citizens Property Insurance Corp. Homeowners would gain tangible financial incentives, making the upfront $20,000‑$30,000 investment more palatable. Moreover, a robust grading database could spawn new business models, such as resilience‑focused construction firms that bundle insurance. In sum, aligning incentives across the housing, finance, and insurance sectors promises not only to protect property but also to generate a sustainable, profit‑driven market for hurricane resilience.

Florida Needs More, Much More Wind Mitigation. Experts at OIR Summit Give Ideas

Comments

Want to join the conversation?

Loading comments...