How Rising Home Insurance Costs Are Linked to Credit Scores

•March 9, 2026

0

Why It Matters

The credit‑based pricing model deepens affordability challenges for low‑income homeowners and amplifies financial vulnerability after disasters, prompting regulatory scrutiny and calls for fairer underwriting practices.

Key Takeaways

- •Fair credit homeowners pay up to 2.3× higher premiums.

- •29% of consumers have fair or poor credit scores.

- •Credit bans can lower low‑score premiums by ~$175 annually.

- •NBER finds low‑score owners pay $550 more in 2024.

- •Disparities amplify financial strain after natural disasters.

Pulse Analysis

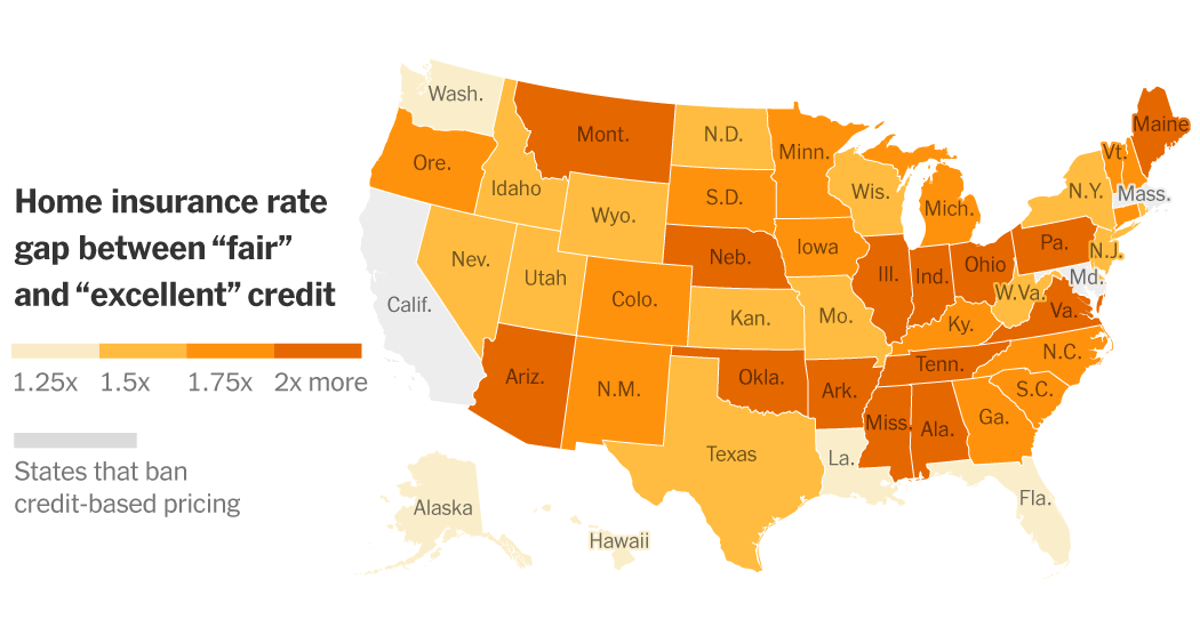

Rising home insurance costs have traditionally been blamed on climate change, rebuilding expenses, and inflation, but a less obvious driver is emerging: credit scores. Insurers employ an "insurance score" derived from a homeowner's credit history, and recent analyses show that a fair credit rating can double or even triple premiums compared with excellent scores. States such as Tennessee, Alabama, and Ohio exhibit the steepest gaps, where fair‑score policyholders face a 2.3‑fold increase. This pricing structure means that, for many, a poor credit profile is as costly as living in a high‑risk disaster zone.

The equity implications are profound. Approximately 29 percent of U.S. consumers fall into the fair‑or‑poor credit bracket, often overlapping with low‑income and minority households. When a natural disaster strikes, affected homeowners frequently turn to credit cards and loans for repairs, further eroding their scores and triggering a feedback loop of higher insurance costs. Early natural experiments, such as Washington State’s temporary credit‑ban, demonstrated that removing credit factors can shave about $175 off annual premiums for low‑score owners while modestly raising rates for high‑score customers, suggesting policy levers can mitigate the disparity.

Industry defenders argue that credit scores predict claim frequency, citing NBER findings that low‑score households file more claims due to limited cash reserves. Critics counter that insurance is a mandated product, and pricing based on credit effectively penalizes the financially vulnerable, reinforcing socioeconomic inequities. As more states contemplate bans or caps on credit‑based underwriting, insurers may need to pivot toward alternative risk indicators—like property characteristics and loss history—to balance actuarial soundness with consumer fairness. The ongoing debate underscores a broader shift toward transparent, equitable pricing in the home insurance market.

How Rising Home Insurance Costs Are Linked to Credit Scores

0

Comments

Want to join the conversation?

Loading comments...